Q4 2024 Earnings Call Transcript")

")

Headwater Exploration (OTCPK:CDDRF) shows no signs of slowing down anytime soon. If anything, the cash is piling up yet again for this debt free upstream producer. That could produce a burst of more activity down the road. Oil prices appear to be a little bit more accommodating for heavy oil producers, and this heavy oil producer has some unusually profitable wells.

As the last article pointed out, higher prices often lead to more activity because paybacks are very short in the current environment. Management has announced a slew of discovery wells. Therefore, adding yet another rig is not yet out of the question. There has been a start of secondary recovery in some areas that can slow growth because secondary recovery efforts often lag up to a year. But right now, everything points to a bright future.

Earnings

This company posted one of the biggest positive earnings comparisons you will see in the industry. That is true especially considering this is a growth situation (not a recovery or turnaround where big positive comparisons are common).

(Note: Headwater Exploration is a Canadian producer that reports in Canadian dollars unless otherwise stated.)

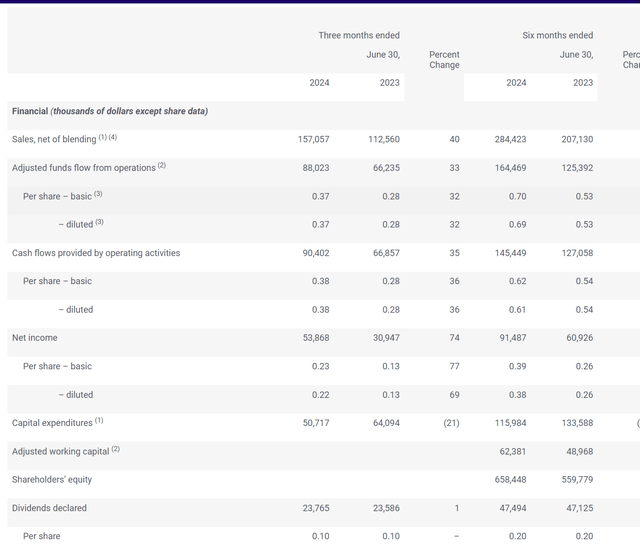

Headwater Exploration Second Quarter Earnings And Financial Highlights (Headwater Exploration Second Quarter 2024, Earnings Press Release)

Earnings roared ahead about 77% on a per-share basis. Adjusted funds flow roared a little less at 32% growth per share. But both of those growth figures are very robust.

As a result of this, adjusted working capital leapt up to C$62 million. Since production also grew, there is a very good chance that adjusted funds flow will exceed C$1 per share in the current fiscal year. Management could beat their own exit production rate goal as well.

The current cash and accounts receivable balance approaches C$200 million. Therefore, it is just a matter of time before management feels that there is enough cushion to raise the activity rate.

This is easily one of the more profitable companies I follow of any size, and it has one of the best balance sheets in the upstream world with no debt and lots of cash for its size. That kind of conservativism takes a lot of risk out of the upstream investment idea because debt free companies rarely get into serious trouble.

Likewise, there are other industries where you would pay far more for the kind of growth shown here. Therefore, there is likely to be a lot more upside in the future than downside.

Official Guidance

The official guidance is on the conservative side. Still it’s hard to find companies in this industry that can profitably grow organically while paying a dividend.

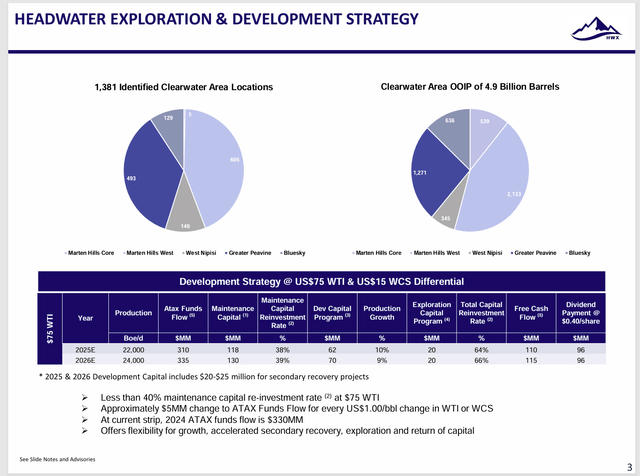

Headwater Exploration Production Growth Guidance (Headwater Exploration Corporate Presentation Second Quarter August 2024)

Note the conservative assumption about less than 40% of cash flow is needed to reinvest to maintain production. One of the things that enables the situation is that the secondary recovery often slows decline rates to far below the typical new wells first year experience for either conventional or unconventional. The result is that this company will have a blended decline rate made up of some secondary recovery and some usual decline rates.

That is going to prove to be a competitive advantage in the future because decline rates and growth rates often determine the maintenance capital needed to maintain production in the next fiscal year.

Since Mr. Market loves a growth story and very much hates the opposite, this management likely weighs the consequences of faster growth on the maintenance capital requirement for the following fiscal year. That determination likely leads to the amount of working capital needed before another rig is added.

Discoveries

In the meantime, the discovery picture likewise appears to be very bright.

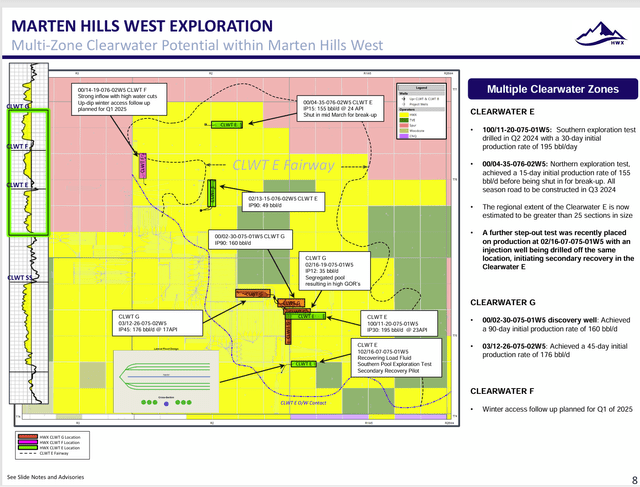

West Martin Hills

Keep in mind that most managements already know that the oil is likely there. Therefore, the chances of exploration success run very high.

Headwater Exploration Summary Of West Martin Hills Exploration Activity (Headwater Exploration Corporate Presentation Second Quarter August 2024)

Out of all the “exploration” wells drilled only one encountered such a high water cut that the company will move the location slightly to see if better results can be obtained. This is typical in the new age of “exploration”. The on-land results are typically decent.

Note that one of the discoveries is delivering 24 API oil. That is getting towards the medium oil grade rather than heavy oil. If enough of that oil is found, it can be sold for a likely better price than the heavy oil.

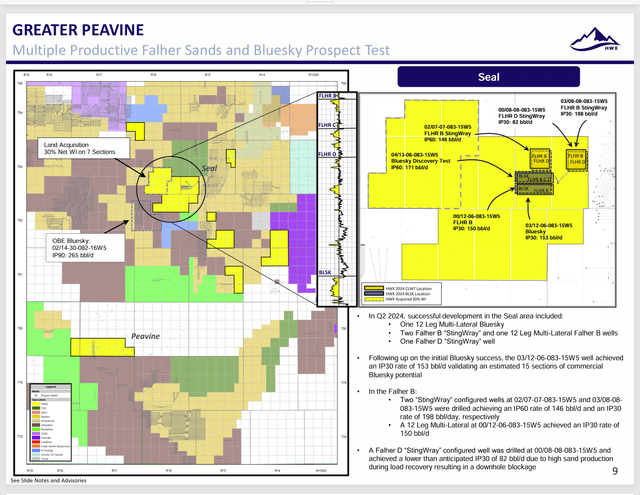

Greater Peavine

Here is yet another area where exploration wells are having a very high success rate.

Headwater Exploration Summary Of Greater Peavine Area Exploration Results (Headwater Exploration Corporate Presentation Second Quarter August 2024)

One of the other considerations is at least some of these exploration results mean there will be more Tier 1 acreage in the next reserve report. As long as this kind of success happens throughout the industry, there is no danger of the industry running out of Tier 1 acreage.

Also, the increase in probable reserves likely means that the company will be busy on this acreage for years to come.

Other Areas

The company has other areas that include acreage in Greater Nipisi, Handel, and Clay. All of these either have exploration well results or have plans for more exploration and possibly further activity.

Most of this points to the fact that the new technology has unleashed a lot of areas that were previously not competitive for industry dollars. So far, there have been no limits to the success of just about anyone in the industry. That means the boundaries of the play or plays using this technology have yet to be determined.

Summary

We are definitely in no danger of running out of oil. The challenge has always been to develop the oil at a reasonable price for general consumption. Right now, technology is moving at such a rapid pace, that many companies like Headwater Exploration can expand operations as they wish. There are always intervals to explore that we have not (likely because we could not) produced yet.

Clearly Headwater Exploration has found a very profitable niche that should lead to years of growth and far more valuable company. The latest Baytex Energy (BTE) (and others) presentation shows that these wells return 500% or more.

Some operators in the area, like Tamarack Valley (OTCPK:TNEYF) report three paybacks in the first year from these wells in the current environment. That makes the company strategy among the most profitable of any company I follow.

The company is a very strong buy that may appeal to a wide range of investors despite its small size. The big cash balance and debt free balance sheet make this a more conservative idea than the small size would normally indicate. Similarly, the relatively low price-earnings ratio likewise lowers the risk of long-term capital loss.

This is that rare company that can grow while paying a dividend. The yield is fairly decent though. Since this management has considerable experience building and selling companies, I would be tempted to hold these shares until they sell the company or until the growth story changes materially.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q4 2024 Earnings Call Transcript")

-to-IRA rollovers, Vanguard finds")