Q4 2024 Earnings Call Transcript")

-to-IRA rollovers, Vanguard finds")

")

Gilead Sciences (NASDAQ:GILD) has dropped 15% YTD substantially underperforming the market. We last discussed the company two months, discussing how it was turning itself around. The company was impacted by tough trial results from Trodelvy, another disappointment given the more than $20 billion acquisition of Immunomedics. Despite that, the company has the ability to utilize its assets to generate strong returns while supporting a >4% yield.

Gilead Sciences 1Q 2024 Takeaways

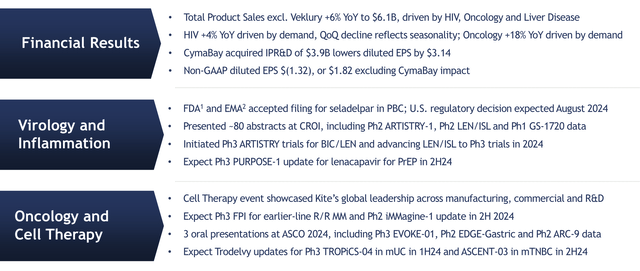

The company had a financially strong 1Q 2024, with some disappointing in trial results such as Trodelvy.

Gilead Sciences Investor Presentation

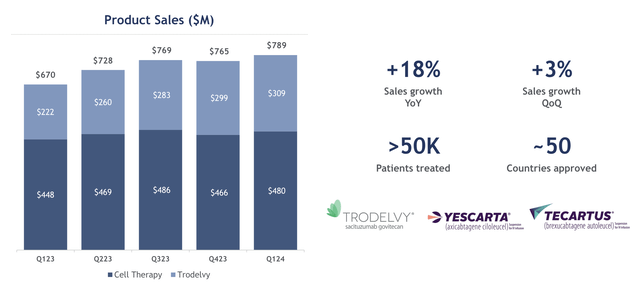

The company managed to grow non-Veklury product sales YoY. Especially strong performance was seen in the company’s Oncology business, but with years of expensive acquisitions here, the company needs to see continued growth. Yescarta is another almost $12 billion acquisition that is finally crossing $1 billion in annual sales 7 years later.

Still the company has an impressive R&D arm that we would like to see growth with. The company needs to build a balanced portfolio outside of HIV to drive long-term shareholder returns.

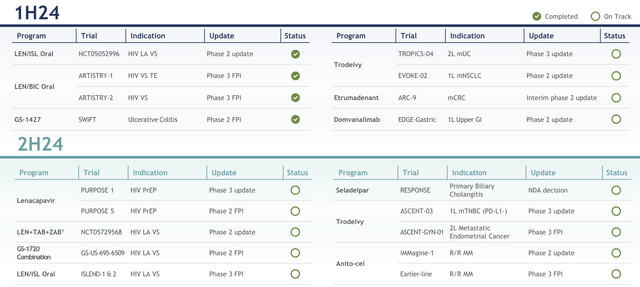

Gilead Sciences 2024 Milestones

The company has a number of exciting milestones in 2024.

Gilead Sciences Investor Presentation

Especially important are some tough results the company has had with Trodelvy that led to a 10% price drop early in the year. Given the more than $20 billion that the company paid for Trodelvy, the company needs to eventually see billions in annual sales from this drug to justify the investment. It’s crossed $1 billion but has a ways to go.

The company has continued to have strong returns from its results in its HIV business, especially.

Gilead Sciences Segment Performance

From a segment perspective, the company continues to be carried by having the strongest HIV business in the world.

Gilead Sciences Investor Presentation

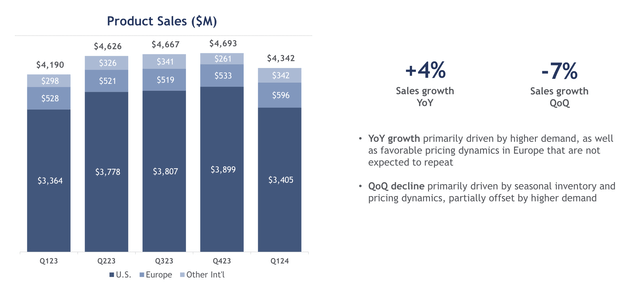

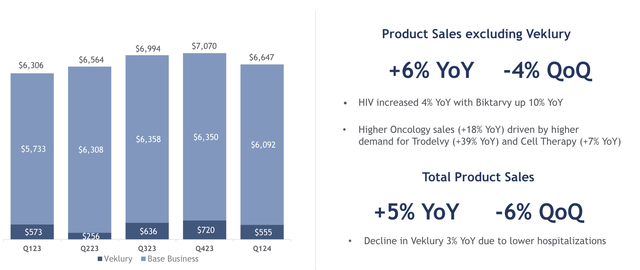

Most of this comes in the U.S., where the company has strong pricing power, but Europe and other international markets continue to provide billions in annual revenue. The company saw some QoQ weakness, not surprising given seasonal variance mostly in the United Sates, however, YoY sales growth has remained strong.

Biktarvy, which has more than $11 billion in annual revenue, has a 49% market share with 3% share growth YoY, and continues to dominate the market. Descovy also has strong market share growth with >40% U.S. market share, and continues to remain a strong PrEP drug for protecting patients, earning almost $2 billion annually.

Gilead Sciences Investor Presentation

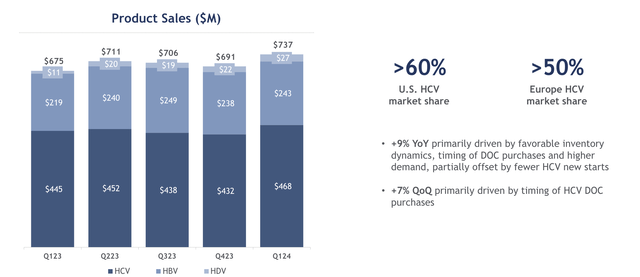

The company’s Hepatitis C business, once a cornerstone, has declined as the number of patients has, but still earns almost $2 billion annually. The company has a >50% market share here. Its Hepatitis B business is approaching $1 billion annually, but has proven a tough industry. Still these form nice sources of cash flow.

Gilead Sciences Investor Presentation

In cancer, where the company is hoping for long-term strength, annual product sales have crossed $3 billion. Backed by more than $40 billion in acquisitions, the company needs sales to be double that, to justify the investment over the long-term. Sales are growing by the double-digits here, backed by Trodelvy as the company’s cell therapy business remains weak.

Still a continued robust R&D portfolio will help growth and the company’s prior missteps here are priced into its stock in our view. Prior investors might be harmed, but those today are receiving the benefit of what is a strong portfolio, even if it was overpaid for.

Gilead Sciences Financial Performance

The company saw YoY growth even though it saw QoQ weakness.

Gilead Sciences Investor Presentation

That was partially impacted by a decline in Veklury, with most of the QoQ impact caused by HIV. The company saw more than $6.6 billion in quarterly revenue, which supports a strong guidance for 2024. The company expects quarterly revenue to remain roughly constant through the year with less improvement going into the back half of the year as 2023.

Gilead Sciences Investor Presentation

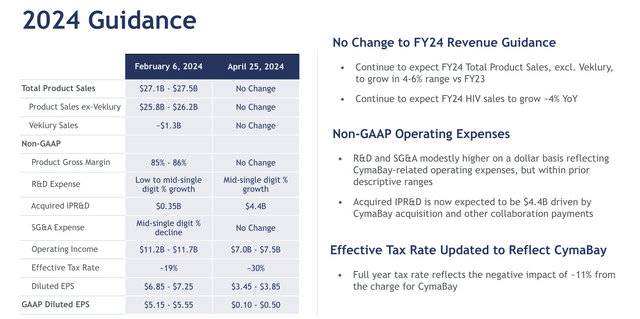

The company expects total product sales of $27.3 billion with weak Veklury sales of $1.3 billion and product sales of $26 billion. The company expects to have a strong gross margin, with IPR&D caused by its recent acquisition of CymaBay. The peak candidate here is Seladelpar, which is expected to cross $1 billion in peak sales but in a decade.

Our opinion on the company’s guidance is that the company maintains an incredibly strong portfolio. Veklury provided a nice boost in sales and shows the strength of the company’s anti-viral portfolio given how quickly it was able to respond. The company is maintaining its guidance, impressive to see given volatility in the industry.

We’re excited to see the company’s strong cash flow, but we want to see it slow down acquisitions until it can see revenue growth from its existing businesses.

Gilead Sciences Investor Presentation

The company has remained committed to shareholder returns. It has $25 billion in net debt which it’s kept roughly constant, and its 2.7% dividend increase keeps its yield at more than 4% at current prices. The company has also managed to decline its share count YoY and repurchased 5.2 million shares at just under $77 / share.

The company has roughly 1.2 billion shares outstanding, so it’s repurchasing at just under 2% a year, a level that it can comfortably afford.

Thesis Risk

The largest risk to our thesis isn’t just the standard risks of volatility facing Gilead Sciences. Ever since the company’s Hepatitis C strength, the company has made numerous acquisitions with lofty goals in Oncology etc. While it’s built some reasonable businesses through the sheer spending of $ billions, the return has been poor.

With continued mistakes, it needs to find a long-term path with its management.

Conclusion

Gilead Sciences has an impressive portfolio of assets. The company has had some missteps with tens of billions of dollars in acquisitions, but at this point it’s priced into the company’s share price. The company is building an oncology portfolio that’s earning billions in annual revenue, and it does have substantial growth potential from this revenue.

Going forward, we expect the company to continue generating its revenue growth. More importantly, unlike other biotech peers, it doesn’t have any major potential upcoming losses of revenue from its drugs. Its HIV business continues to remain strong and growing, and the company remains a leader in antiviral drugs as shown by its quick handling of COVID-19.

Going forward, we expect the company to drive strong shareholder returns, making it a valuable long-term investment.

Read the full article here

Q4 2024 Earnings Call Transcript")

-to-IRA rollovers, Vanguard finds")