")

Introduction & Investment Thesis

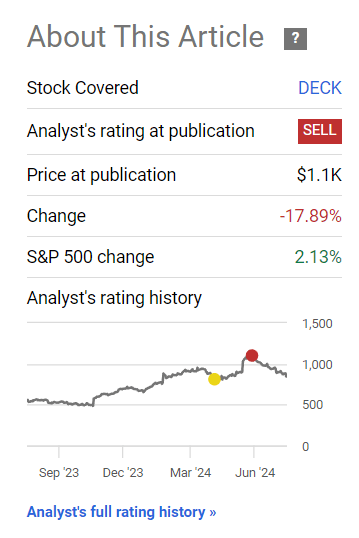

I last covered Deckers Outdoor Corporation (NYSE:DECK) on June 6th, where I believed that the stock was overvalued with excessive investor optimism baked into its valuation, making it prone to a sharp pullback, especially as revenue growth rates slow from their prior levels. I did emphasize, however, that the company had been operating resiliently, as it saw its HOKA and UGG brands continuing to outperform as it leveraged a robust product portfolio. It is also making compelling marketing efforts to acquire and retain customers both in its domestic and international markets. Since then, the stock has declined close to 18%, underperforming the S&P 500 (SP500) and Nasdaq 100 (NDX).

SA:Price change since last coverage

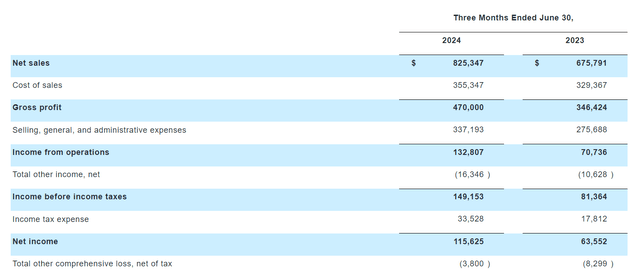

The company reported its Q1 FY25 earnings on July 25th, where it saw its revenue and operating profit grow 22% and 87% YoY, respectively, beating estimates. One of the main factors behind the outperformance was its HOKA brand, which grew 30% YoY, gaining shelf space and market share gains as it built customer loyalty through compelling product assortments and brand moments. At the same time, it also saw its margins expand as it benefited from full-price selling across its HOKA and UGG brands.

The stock rallied after earnings. However, it closed 6.3% higher at the market close on July 26th. I believe that the stock rallied primarily because of the revenue and earnings beat during the quarter, but it will likely be short-lived as the management has not raised its revenue and earnings guidance for the remainder of the year.

Although I believe that the company will continue to operate resiliently, it will face tougher competition moving forward at a time when Stefano Caroti, the present COO, will take the position of CEO moving forward. Assessing both the “good” and the “bad,” I don’t believe that the stock is offering an attractive entry point for long-term investors, with little to no upside at the moment. As a result, I will choose to remain on the sidelines and rate the stock a “hold” at its current levels.

The good: Strong growth in HOKA brand as it benefitted from full-price selling, Strong product innovation and brand affinity across HOKA and UGG, Expanding Profit Margins

Deckers Outdoor reported their Q1 FY25 earnings report. The revenue grew 22% YoY to $825M, beating estimates by 2.3% driven by robust full-price demand across its HOKA and UGG brands globally, contributing 93% of Total Revenue, while both DTC and wholesale channels grew more than 20% each.

Diving into brand performance, HOKA revenue grew 30% YoY and 2.2% sequentially to $545M, with DTC growing at a faster rate of 33% YoY compared to Wholesale Revenue, which grew at 28% YoY. The company continues to drive robust product assortments. These include top styles like Clifton and Bondi as well as emerging franchises such as Mach, where they launched Mach 6, which experienced a strong sell-through in its global marketplace, especially among its younger demographics. Plus, their franchises such as Transport and Kawana are also seeing explosive growth across channels, where consumers are increasingly adopting the light hiker and fitness shoe more for casual and versatile wear.

Meanwhile, the company continues to innovate on its advanced performance leading styles, such as Cielo X1 and Skyward X, with the recent launch of Skyflow at a much more commercial price point to elevate the HOKA brand’s everyday performance lineup. What I think is particularly noteworthy in the company’s HOKA brand is that it is continuing to add shelf space and gaining market share with full price sell-through, something its competitor Nike (NYSE:NKE) has been falling behind on, which is indicating growing customer loyalty from its successful acquisition and retention strategies across distribution channels in its domestic and international regions.

Moving on to UGG, this is the second-largest brand in terms of revenue contribution. It grew 14% YoY to $223M, driven by full-price selling, increased adoption of Golden Collection and continued growth in both DTC and wholesale channels. It had product innovation that is centered around increasing the number of wearing occasions and styling versatility to sustain demand over longer periods of time. Plus, the company has also been driving targeted collaborations to drive marketing activations, along with the upcoming launch of the Feels Like UGG campaign, which will take place through a combination of social media, in-store events, and community events.

Shifting gears to profitability, the company saw its gross margins improve 560 basis points YoY to 56.9% as it benefited from its product mix, with higher margin products within HOKA and UGG driving sales growth along with a higher full-price selling environment. Meanwhile, the company generated $132.8M in GAAP operating income, which grew 87% YoY with a margin of 16%, an improvement of 600 basis points from the previous year. However, SG&A expenses grew at a similar rate to overall revenue growth, making up 40.9% of Total Revenue, compared to 40.8% in the previous year, as the company drove investment in marketing initiatives to expand global HOKA awareness and recruit talent.

Therefore, the year-over-year expansion in margin was fully led by the company’s success in driving growth through full-price selling across its brands, especially HOKA. It gained increasing customer loyalty and market share.

Q1 FY25 Press Release: Revenue and Profitability growth YoY.

The bad: Leadership change when earnings growth is peaking, Revenue guidance unchanged

In my first coverage of Deckers Outdoor, I discussed that Dave Powers had announced his retirement after serving as the CEO for the last 8 years, during which the stock had a phenomenal run. This was the last quarter under Dave’s leadership, with Stefano Caroti becoming the next CEO on August 1st. While Stefano has had extensive experience running Deckers Outdoor as Chief Commercial Officer until now, he is taking on the role at a time when revenue and earnings growth is expected to slow down from its previous levels. At the same time, leadership changes are often accompanied by uncertainties, especially when it comes to the respective styles and strategies to navigate a highly competitive and macro economically tough landscape.

SA: Earnings growth has likely peaked

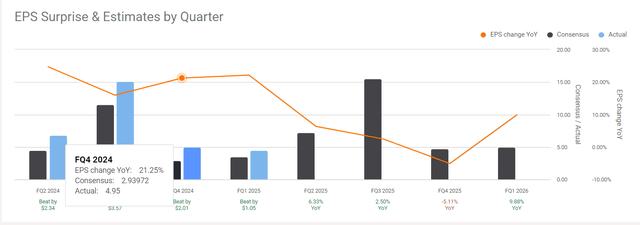

On the competitive front, Deckers Outdoor mainly competes with Nike, Skechers (NYSE:SKX) and Crocs (NASDAQ:CROX) and while Deckers is growing at a faster rate than Nike and Crocs, it is also trading at a higher premium. On the other hand, Skechers, which is growing at a similar rate to Deckers Outdoor, is trading at a cheaper forward price to earnings multiple of 16. This is compared to Deckers, which is trading at a 68% higher premium with a price to earnings ratio of 27. While Deckers Outdoor is steadily gaining customer loyalty from its product assortments, leading to higher market share, along with beating analyst earnings expectations for four quarters in a row, earnings growth has likely peaked. It faces tougher comps moving forward.

Meanwhile, the company also kept its expectation for revenue growth in FY25 unchanged from the previous quarter, where it expects revenue to grow 10% YoY to $4.7B. However, they increased their expectation for gross margins by 50 basis points to 54% given the strength of the first quarter results, while projections of operating margin are anchored at previous levels of 19.5%–20%. During the earnings call, the management outlined that their FY25 guidance assumes no meaningful deterioration in macroeconomic conditions from current levels. While I generally agree that the overall macroeconomic environment should improve with the Fed getting ready to start cutting interest rates, keeping revenue guidance unchanged for FY25 indicates management’s caution to manage analyst expectations under the new leadership.

Revisiting Valuation: The post-earnings rally will be short-lived, with no substantial upside.

Although the stock is up over 6% post-earnings call, I believe that the rally will be short-lived. While the company is still operating with resilience and strong growth in its HOKA brand, as it continues to gain market share both in its domestic and international markets through product innovation, compelling brand campaigns, and distribution expansion, the company will face tougher comps moving forward. Meanwhile, the management has not raised its guidance on the revenue or earnings front.

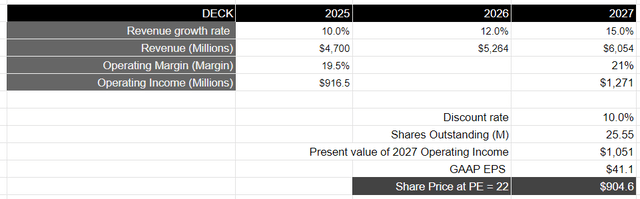

Therefore, my valuation assumptions remain more or less the same as before. I expect revenue growth to accelerate to the low and mid-teens in the coming years as it can gain higher market share through its product assortments for both HOKA and UGG, resulting in a revenue of $6B by FY27. From a profitability standpoint, assuming that operating margin expands by 50–100 basis points every year, as it improves its unit economics through a product mix of higher margin products along with inventory optimization, it should generate $1.27B in operating income by FY27. This will be equivalent to a present value of $1.05B when discounted at 10%.

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% over a 10-year period, with a price-to-earnings ratio of 15–18, I believe that Deckers Outdoor should trade at 1.25x the multiple. This is given the growth rate of its earnings during this period of time. This will translate to a P/E ratio of 22, or a price target of $904, which is where the stock is currently trading.

Author’s Valuation Model

My final verdict and conclusions

Since I last issued a “sell” rating on the stock based on my analysis that there was too much investor optimism baked into the company’s valuation, the stock has declined more than 17%, underperforming the indices. This is even after the stock rose significantly after its post-earnings rally, though it lost a lot of steam by market close.

Personally, I believe the rally will be short-lived, with the stock either range-bound or declining from its current levels in the coming months, as the management has kept its growth projections unchanged from the previous quarter. While I am optimistic about Deckers’ execution to gain market share in its HOKA and UGG brands as it gains brand affinity while driving financial discipline, it doesn’t offer an attractive long-term opportunity or entry point now. There is little to no upside, making Deckers Outdoor Corporation shares a “hold” at its current levels.

Read the full article here