-to-IRA rollovers, Vanguard finds")

")

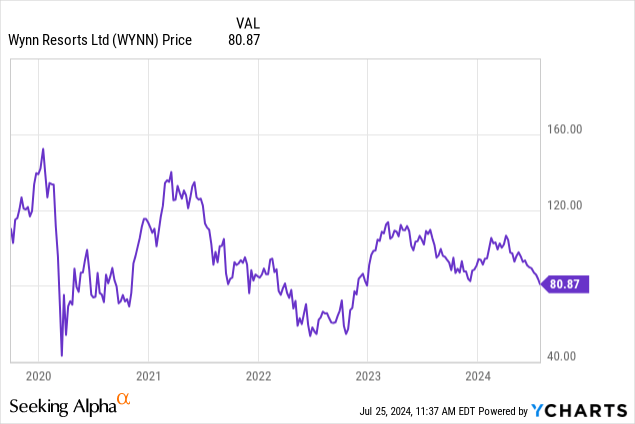

Wynn Resorts (NASDAQ:WYNN) is right now at pandemic prices, even though we are now far away from 2021. I think the market is heavily overlooking the solidity and growth opportunities of the business for the years to come, hence my buy rating for WYNN.

Wynn is a full recovery investment case and possibly more.

Briefly, Wynn Resorts is a casino company. This means they develop and operate casinos not only, not even mainly, in the US but all over the world. As a part of its main casino activity, the company also receives supplemental revenue sources from hotel rooms, food and beverage, and the entertainment, retail, and other services segment.

Specifically about the sources of income shown in the Earnings report for Q4 2023, casino revenue distribution for FY2023 was 57%, hotel rooms 18%, food and beverage 15.6%, and the entertainment, retail, and other segment 9.2%.

Considering this, the vast majority of Wynn’s revenues come directly from its properties in the US, but also from Wynn Macau, where it does not have complete control, but it just has 72% equity.

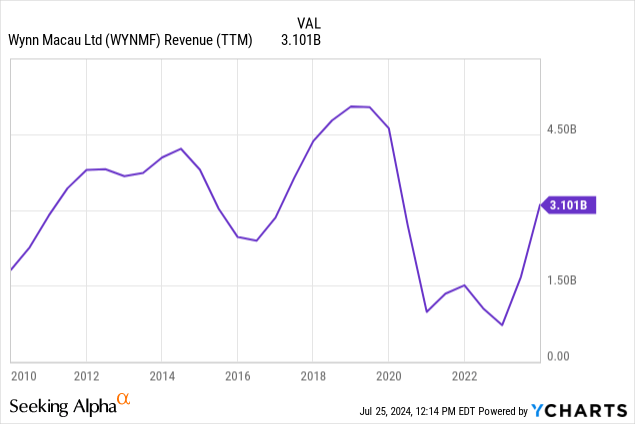

Wynn Macau, operations and ongoing recovery

In terms of operations, Wynn Macau comprises two huge operating resorts, Wynn Palace, located in the ultra-famous Cotai Strip (around 60% of revenues), and the homonymous Wynn Macau, placed in the inner harbor of the city (around 40% of revenues).

Unfortunately, Wynn Macau’s (OTCPK:WYNMF) revenues have not recovered from 2019 levels yet, falling short of just 70% of those by FY2023.

Following the most recent earnings release, revenues at Wynn Palace were $587 million in Q1 2024. That is 80% of revenues shown in 2019 and 88% of 2018. For the Wynn Macau property, both comparisons come at 78% and 67% of revenues for those years, respectively.

The company is showing a clear sign of recovery, and it will only improve as Outbound Travel to China recovers from the current 30% of 2019 level to an expected 80% by year’s end, as Trip.com (TCOM) management has expressed. Additionally, today, the occupancy rate has fully recovered to the usual 95% plus levels. REVPAR is also considerably higher for Wynn Palace, while it is close to the same for the Wynn Macau property.

Nonetheless, a counterargument against this recovery thesis could be made. It is true that a big part of the Macau casino gambling business comes from VIP clients. These clients are mainly coming from mainland China and not from outbound travel, but at the end of the day, foreigners will still bring more revenues to the mass casino segment, and the Chinese VIP client will likely continue to come back as the Chinese economy recovers slowly.

Wynn’s recovery in the US is more than complete

Wynn’s US operations have traditionally been present only in Las Vegas, but now Wynn can also rely on the Encore Boston Harbor property. For Q1 2019, revenues came in at just $401 million, down from $431.5 million in 2018 just in Vegas. Instead of those numbers barely surpassing the 400s, now Wynn reports for the last Q1 of 2024 $636.5 million in revenue just for Vegas and an additional $217.8 million coming from Boston. Together, both properties bring now more than 113% more income than in 2019. This speaks of the relatively good capital allocation made by the management some years ago. Las Vegas properties have also shown higher occupancy rates than in 2019.

This good success seen in Boston is likely to be replicated in the new development currently under construction in the United Arab Emirates, the Wynn Al-Marjan project. In my opinion, this project will bring around at least twice the revenues of the Boston property, since it will be around double the size.

Profitability is also doing well, and buybacks came back

From a profitability perspective, the company has presented a 1.59 adjusted EPS for Q1 2024. This is almost the same as it was in Q1 2019 at 1.6, but lower than the 2.3 reported in 2018. The 2018 numbers are interesting, in my opinion, to compare what the company could do not only with a fully recovered Macau but also with roaring gaming activity, even though that level cannot be kept throughout time because, at the end of the day, it is unsustainable for the clients.

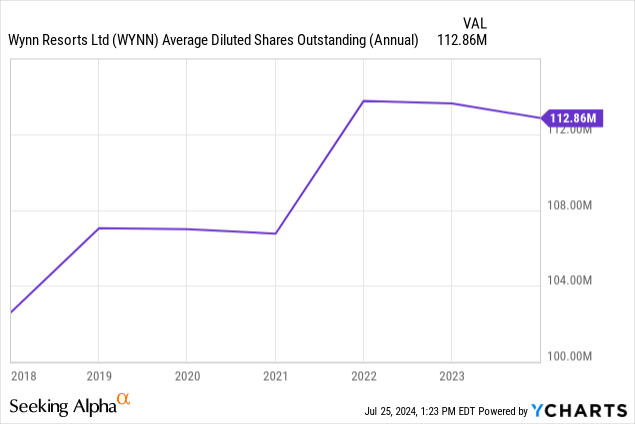

The share count otherwise has increased significantly from 2019, but fortunately, out of heavy financial distress, the company has managed to stabilize it and even done some buybacks. Honestly, I do not agree with having done those buybacks instead of paying down some debt.

Some fundamentals have worsened compared to 2019

Unfortunately, the recovery path for Wynn stock is not completely clear. For example, the company’s balance sheet is in a worse situation now than in 2019. Long-term debt is now over $2 billion higher than then, and the current debt will need to be rolled over since it is almost 3 times the adjusted earnings for the 2023FY.

The bad debt situation also does not help if we compare our current higher interest rates with those in 2019. In 2024, our interest rates are 300 basis points higher than in 2019. This situation directly impacts the returns the companies have but has a stronger impact on real estate companies because of the higher levels of debt that these companies usually carry, and Wynn is not an exception.

Another additional impact coming from interest rates on Wynn is that valuations will need to be lower for the company, as capital discounts on financial projections need to be higher due to the presence of current high interest rates that pay a decent 5% amount for just having the cash parked at the central bank.

These, combined with the company’s inability to grow more than the expected UAE project because of the nature of a Real Estate business and slightly bad news coming from a recent 5% decline in Macau gaming revenues, weigh on the stock.

Valuation

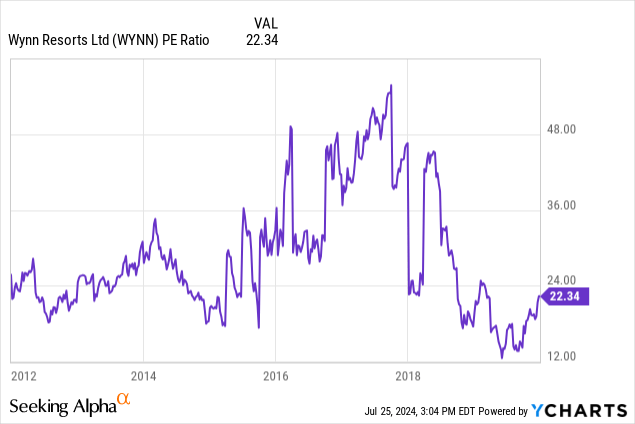

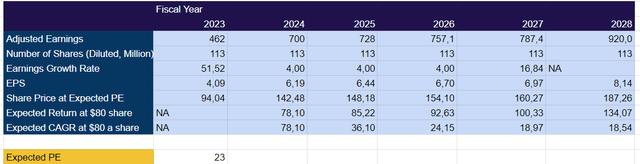

The current P/E ratio is around 22 times earnings, which is on par with the historical record. I consider the stock to reach $700 million in adjusted earnings by the end of this year if the recovery does happen smoothly. Additionally, I am not counting on Wynn doing buybacks as I think that is bad capital allocation due to the high debt levels, nor am I counting dividends in the returns of this model.

For the next few years, I am expecting a low growth in EPS of just 4% but a fully functional Al-Marjan property working by 2028. In this model, assuming a P/E of 23, the stock might be able to provide quite a strong 18% CAGR over the next five years.

Image created by the author based on WYNN SEC filings and projections (Author)

Some relevant risks associated with Wynn stock

Because WYNN is heavily exposed to Macau, a territory controlled by the Chinese government, the biggest risk is geopolitical tensions. Any important conflict between China and the West, for example, with Taiwan, might cause a stock market collapse, especially in stocks as heavily exposed as Wynn.

Another important risk to these stocks is those related to travel disruptions. Another global health public issue, some form of terrorist attack like the ones in 2001 might cause uncertainty for travelers and a material diminishing of revenues.

Additionally, of course, macroeconomic uncertainty can cause the stock to perform badly for years to come. For example, an increase in interest rates might be able to disrupt valuations, causing the projected 23 P/E ratio never to come back again, there, a pricing readjustment might be needed.

It is important to remember that as a Chinese-exposed investment, Wynn has had to deal with the Chinese authorities, and eventually, the company might be subject to a sudden crackdown like what happened with the technology companies from 2021 to 2023. Bear in mind this is not an easy buy-and-go-to-sleep investment.

Conclusion

Wynn Resorts is a solid company with solid arguments to outperform the markets from here. Unfortunately, the company also carries some important risks that make this investment less compelling.

I think the company has a place in a well-diversified portfolio that does not already have too much Chinese exposure. Even though the potential gains might be important, so are also the risks. Therefore, I grade the stock as a bare buy.

Read the full article here

-to-IRA rollovers, Vanguard finds")