: Medical Properties Trust Stock (NYSE:MPW)")

")

(NASDAQ:CGBD)")

")

Investment Overview

Twist Bioscience (NASDAQ:TWST) will announce its Fiscal Q3 2024 earnings next Friday, 2nd August – analysts’ consensus is for revenues of $77.37m, and earnings per share (“EPS”) of $(0.77).

This matches top-line guidance provided by the company itself – for $77m of revenues (and $77m – $80m in Q4), and, given EPS in Q2 was $(0.79), and gross margin is expected to climb from 41% in Q2, to 41-42% in Q3, I’d also expect Twist to meet or even slightly exceed analysts expectations on EPS also.

This is my first time covering Twist Bioscience for Seeking Alpha, which is partly due to the fact that Twist came onto my radar in early 2021, when the company was being celebrated as one of Cathie Wood’s ARK Innovation ETF (ARKK) most successful holdings, its share price having risen from its 2018 IPO price of $14, to a high of >$150 – representing a gain of very close to 1,000%.

In its Q1 2024 quarterly report, Twist discusses its business as follows:

an innovative synthetic biology and genomics company that has developed a scalable DNA synthesis platform to industrialize the engineering of biology. The core of our platform is a proprietary technology that pioneers a new method of manufacturing synthetic DNA by “writing” DNA on a silicon chip.

We have miniaturized traditional chemical DNA synthesis reactions to write over one million short pieces of DNA on each silicon chip, approximately the size of a large mobile phone.

We are leveraging our unique technology to manufacture a broad range of synthetic DNA based products, including synthetic genes, tools for next-generation sample preparation, and antibody libraries for drug discovery and development.

In 2021, a number of recently IPO’d companies focused on the life sciences industry, but pioneering new types of products and tools to assist in diagnostics, antibody discovery, DNA / mRNA writing tools, etc., commanded multibillion dollar valuations, only for their share prices to decline dramatically during 2022 and 2023, amid a post-COVID backlash against the biotech industry.

The likes of AbCellera (ABCL), Exscientia (EXAI), OminAb (OABI), and Telesis Bio (TBIO), have seen their share prices decline by 95%, 81%, 52%, and 99% either on a 3-year basis, or since going public, and as an investor in Telesis – formerly known as Codex DNA – myself, based on its partnership with Pfizer (PFE), I have not exactly been keen to gain more exposure to this space!

Nevertheless, after sinking to lows of <$15 per share in mid-2023 – its declines dovetailing with those of the ARK Innovation ETF, Twist’s share price has embarked on a strong bull run. Shares trade at a value of $59 at the time of writing, up >130% on a 12-month basis, and 80% on a 6-month basis.

Now that the share price trades a long way off its premium price of $190 – discounted by ~70% – and is rising, not falling, is it worth considering and investment in the not inconsiderable promise of Twist’s technology? In this post, I’ll try to answer that question.

Twist in 2024 – Growing Revenues, Chasing Profits

First of all, let’s consider what type of products Twist is selling – according to the company’s 2023 annual report/10-K submission:

We have combined our silicon-based DNA writing technology with proprietary software, scalable commercial infrastructure and an e-commerce platform to create an integrated technology platform that enables us to achieve high levels of quality, precision, automation, and manufacturing throughput at a significantly lower cost than our competitors.

We have applied our unique technology to manufacture a broad range of synthetic DNA-based products, including synthetic genes, tools for next generation sequencing, or NGS, sample preparation, and antibody libraries for drug discovery and development, all designed to enable our customers to conduct research more efficiently and effectively.

Leveraging our same platform, we have expanded our footprint beyond DNA synthesis to manufacture synthetic RNA as well as antibody proteins to disrupt and innovate within larger market opportunities, in addition to discovery partnerships for biologic drugs and developing completely new applications for synthetic DNA, such as digital data storage.

We currently generate revenue through our synthetic biology and NGS tools product lines as well as biopharma services for antibody discovery, optimization and development.

Typically, this type of market opportunity is challenging for two primary reasons (I’d speculate). Firstly, industry incumbents such as Thermo Fisher (TMO), Charles River Laboratories (CRL), and in the gene sequencing field, Illumina (ILMN), are tough to shift, with revenues, R&D budgets, infrastructure and customer bases an order of magnitude larger than its smaller, challenger competitors.

Secondly, budgetary constraints of potential customers such as academic research centres, hospitals, small biotech companies and private research labs make them reluctant buyers of more niche products supplied by smaller companies.

Nevertheless, Twist reported a relatively encouraging set of fiscal Q2 2024 earnings in May this year. The company drove record revenues of $75.3m, up 25% year-on-year, orders were up 45% year-on-year, to $93.2m, and management hiked its 2024 revenue guidance, to $300 – $304m, and its gross margin guidance, to 41.5 – 42%.

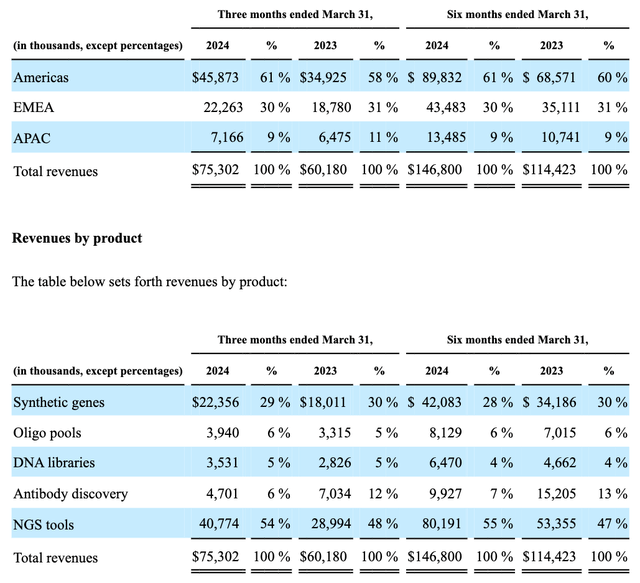

Twist – revenue overview (10Q submission)

As we can see above, Twist earns the majority of its revenues in the US, but has a large and growing source of revenues in Europe and APAc also, and while its revenues are dominated by sales of synthetic genes and next-generation sequencing tools, there is a good mix of other products and services also, with every segment growing, and the two largest growing by 29%, and 54% year-on-year, respectively.

On the negative side of the ledger, Twist is not yet profitable, recording a net loss of $(45.5m), or $(0.79) per share, which is at least an improvement on the prior year – net loss of $(59.2m), or $(1.04) per share. Management’s forecast is for a full-year loss of $(183m) – $(188m) before taxes.

The company reported cash and equivalents of $243m, and total current assets of $372m, with only $142m of total liabilities, so there is some pressure on the company to drive towards profitability, ideally in 2025, before the funding runway becomes too close to being exhausted. The company’s accumulated deficit stands at $1.12bn, so shareholders likely want to avoid being diluted any further (although I have a suspicion this is what may happen).

Looking Ahead – Steady Revenue, Margin Growth The Target

From an investor’s perspective, it ought to be good news that Twist appears to be strongly focused on increasing both its revenue and its gross margin, which is the path to profitability.

On the Fiscal Q2 2024 earnings call with analysts, Chief Financial Officer (“CFO”) Adam Laponis noted that gross margin had increased from 31%, to 41%, in just four quarters, and the company’s longer-term plan is to drive it above 50%, as Twist CEO Emily LeProust explained on the same call:

As we look over the next 18 months, in addition to driving revenue goals which is the primary driver of margin, we intend to continue to focus on margin improvement initiatives including product investments, operational excellence in sourcing and process optimization.

In addition, we’re in the process of negotiating contracts with suppliers and in some cases, with customers willing to provide volume commitments of fixed premium pricing in Express Gene.

We believe these initiatives, as well as further volume leverage of our fixed costs enable our ability to improve our margins by several points, and we see our path to gross margin north of 50% by the end of fiscal 2025.

Management seems to be aware that as the business scales up, it needs to show profitability, or the funding runway will be exhausted. The company has recently added a second manufacturing site, and, according to its Q2 2024 earnings presentation, has an edge over the competition in “speed, price and scale”.

The company’s newly launched product, Express Genes, has got off to a good start in 2024, but has not yet had a full quarter of sales to report, so Fiscal Q3 earnings, due to be reported on 2nd August (next Friday) will be instructive on that front – management has promised SynBio revenue of $31m, versus $29.8m in Q2, and NGS revenue of $41m, versus $40.8m in Q2 – as will Q4 earnings, with management pledging $77m – $80m of revenues

It is vital that Twist keeps building momentum and continues to satisfy its customers – of which there were >2,250 in Q2, up by ~150 year-on-year. In my view, Express Genes ability to deliver “fast turnaround times at scale” may be the right product, at the right time for this growing sector of the market.

Twist estimates its serviceable addressable market to be ~$6bn across synthetic bio and next-generation sequencing (“NGS”), with plenty of growth opportunities – oligo pools, IgG proteins – in play. It is certainly true that these markets are growing, albeit there are not too many bona fide end use cases for NGS products – newly IPO’d GRAIL (GRAL), the cancer testing provider, could open up the cancer testing field, however.

Concluding Thoughts – Why I’d Back Twist To Succeed In A Market Where Most Companies May Not

Personally, I have a gut feeling that Twist can succeed in this challenging market, where customers can be reluctant, use cases scarce, revenues hard to come by and costs high.

Importantly, Twist has shown it can grow revenues – they have risen from $54.4m in 2019, to potentially >$300m in 2024. The customer base is thankfully diverse, 19% academia, 1% agriculture, 56% healthcare, and 24% industrial / chemical / biotech, the company says.

Twist has a unique technology with a competitive advantage – its products may work faster, and have cheaper price points than its rivals, thanks to its silicon chip technology – and momentum can be sustained by new product launches, such as Express Genes, and DNA data storage – an untapped market.

Shares have enjoyed a mighty bull run, to early 2021, and endured a torrid bear run, but having hit rock bottom, the recent upside trend has been uninterrupted for the best part of 6 months.

Twist has a valuable tailwind behind it – momentum – and it seems to have earned the trust of not only >2,500 customers and counting, but also Mr Market – an intangible advantage versus competitors, the majority of which are still suffering from sell-offs and downgrades.

There are risks to consider before making any investment into Twist, however. I suspect management may look to raise further funding – which in some ways is understandable, as a cash injection gives the company the means to grow faster than the market – but raising funds devalues the share price and the accumulated deficit has risen >$1bn. At what point do shareholders begin to wonder if the company will ever deliver an ROI, and begin to pull money out?

Additionally, Twist’s products could be blown out of the water by new technology, either developed, or acquired, by its larger competitors, putting pressure on revenues, and also on margins (the company may need to spend more heavily on SG&A in such an instance).

Finally, given Twist’s current market cap is $3.44bn, and its revenues forecast for 2024 is for ~$300m, the forward price to sales ratio is >10x, without any profits to look forward to. Essentially, if you are buying Twist stock, you are buying on the expectation of rapid revenue growth, but does Twist have a strong enough product portfolio to satisfy Wall Street’s expectations?

When I look down the list of analyst coverage of Twist for Seeking Alpha, in the past 15 months, there have been no “buy” calls, no “sell” calls, and ten “hold” calls – out of ten.

Not only for this reason, I am going to stick my neck out and give Twist stock a “Buy” recommendation ahead of Fiscal Q3 earnings due next week.

In my view, COVID, and the intense scrutiny on vaccine and antibody drug development, and the numerous success stories e.g. Eli Lilly’s bamlanivimab, which helped AbCellera launch its IPO, while in fact it was unrealistic to think a new bamlanivimab could be easily discovered – created unreasonable expectations around this segment of the drug development space and created a bubble.

That bubble was well and truly burst in 2022 and 2023, and it is also the case that Pharma companies like to complete R&D in house, so are not necessarily on the lookout for companies to work alongside. This all makes for a tricky market, in my view.

I like Twist’s product mix, however, and I view the company as capable of expanding its product offering based on its unique and differentiated technology, and crucially, I believe the company and management have support on Wall Street, which has found a sensible valuation to work with, after several years of boom and bust, and is now watching the growth story unfold, and the company progress towards profitability.

More good news next Friday ought to send the share price a little higher, and make a slightly bloated valuation look more reasonable.

Read the full article here

: Medical Properties Trust Stock (NYSE:MPW)")

")

(NASDAQ:CGBD)")