Q4 2024 Earnings Call Transcript")

-to-IRA rollovers, Vanguard finds")

The following segment was excerpted from this fund letter.

Year to date, Siemens Energy is up ~124% and up ~140% from our average entry price. We view this return as likely driven by investors pricing the stock based on a more thoughtful and informed valuation following a nasty sell-off last year, driven by the firm’s troubled wind turbine business.

Siemens Energy has two operating segments: Gas and Power Services (comprised of the gas turbine and grid technology businesses) and Wind Turbines. Gas Turbines, Grid Technology, and Wind Turbines businesses each account for ~30% of total revenue, with the remaining 10% coming from the firm’s transformation of industry division, which provides various niche services related to addressing the energy needs of industrial businesses. Last year, the firm sold off ~72% from its peak of €24.4 per share to a low of €6.8 based on issues solely associated with the wind turbine segment.

The specific issues that prompted the slide were quality issues affecting only 4% of the firm-installed Wind Turbine fleet. The company took a €1.6bn charge in Q3 and lowered its profit contribution from the future execution of Siemens Gamesa’s order backlog. The firm also took a €600 million charge to address production costs and ramp up challenges in the firm’s offshore segment. The stock dropped roughly 37% on these issues, announced in June/July last year.

In October, the firm announced that it was struggling to secure financial guarantees to serve as insurance to customers in case of a default on the type of long-term projects that Siemens Energy takes part in. Financial guarantees were difficult to secure because of the challenges in the wind turbine business.

Without added guarantees, ENR could not successfully bid on new projects for its Grid Technology and Gas Turbines and Power Plants segments. The firm’s shares sold off a further 35% on that news despite the positive underlying implications of the need for additional financial guarantees.

At the low in October/November of last year, the firm’s market cap bottomed out at ~€5.5 billion, vs. our estimate of the value of the business less the wind turbine segment but including liabilities associated with the wind turbine business of ~€15.5 billion. We added to our position several times between June and November, doubling its size.

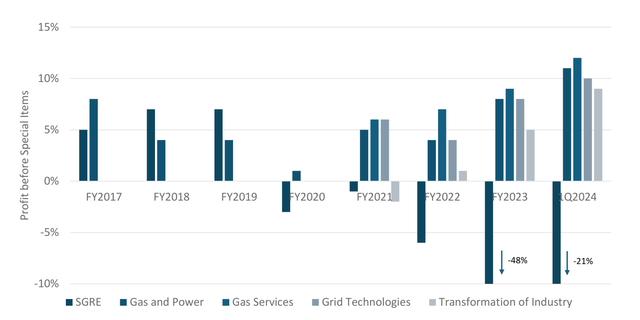

Our thesis on the stock remains the same as when we initiated our position in 2022. The company’s products and services cover the entire electricity value chain from conventional energy generation to renewables and grid infrastructure, and with several thematic tailwinds to the stock, including decarbonization, energy demand growth, and grid infrastructure investment, all that remains is for management to prove it can profitably operate the business. On that front, management has made considerable progress in all areas except wind, a fact overlooked last year in the sell-off (See Figure 10).

While the returns from Siemens Gamesa (SGRE) are a drag on the business and require significant attention, management’s focus on the other segments over the last few years has yielded meaningful returns. Management has improved margins within the non-renewable businesses and aggressively grown the order backlog, with order intake rising by more than 60% since FY2017. Overall, the story of the Gas and Power business unit (formed of Gas Services, Grid Technologies, and Transformation of Industry starting in 2021) has been one of rising orders, improving margins, and more robust cash generation.

Figure 10: Margins at Individual Reporting Segments at Siemens Energy

Source: Company Filings, Massif Capital

This year’s price rise is a recognition that Siemens Gamesa, although a clear overhang on the stock and the company’s performance, is just one piece of a larger pie. For the rest of this year, we expect the firm’s position as the world’s largest supplier of grid solutions1 and second largest producer of grid products2 to continue to support positive returns and look to 2025 and 2026 as years in which the rehabilitation of SGRE will start to positively affect the bottom line.

The grid business is experiencing significant growth, powered by increased demand for connecting renewables to grids in Asia, the US, and Europe and rising demand for grid services to deal with the electrical grid’s ever-greater complexity. Management expects to continue growing the grid business by low double digits, with double-digit margins for the near future.

The business’s barriers to entry are high, requiring significant technical and practical experience. For example, Siemens is one of only a handful of companies globally that produce large power transformers (LPTs) for the US Grid. Currently, only 20% of US large power transformer demand is met domestically (80% are imported, principally from Japanese and South Korean companies), with lead times of five years or more. Transformers are the critical equipment linking generation systems to distribution.

Recognizing the opportunity, gauging the political winds and the rise of national security-related protectionist concerns, Siemens is investing $150 million into its Charlotte, North Carolina facility to ramp up domestic production of LPTs. As far as we can tell, this is the only meaningful investment by market participants, even though the annual demand for LPTs has grown 22% since 2019 and is expected to grow a further 47% by 2030. For the US unit, Siemens needs to capture only 12% of the growth over the next six years to generate $150 million a year in revenue, equivalent to the 57 LPT’s management expects the plant to produce when in full operation. At that time, the US will still need to import 52% of the annual LPT demand (equivalent to 699 LPTs), suggesting ample room for growth after the first investment.

Although minor, the above example is an interesting case of the numerous niche opportunities that exist in the electrical system; on the other end of the spectrum, Siemens Energy, in consortium with Spanish firm Dragados Offshore, has signed an agreement with German-Dutch transmission operator TenneT to supply high-voltage direct current transmission technology for three grid connections that will ensure 6 gigawatts of offshore wind power can be transported back onshore. This contract has a value for Siemens and Dragadow of €7 Billion.

Meanwhile, other European Transmission System Operators are ramping up spending. National Grid expects to spend £42 billion over the next five years on transmission, grid infrastructure, and E.On expects to spend €26 billion on transmission infrastructure. A review of capex plans presented by European transmission system operators suggests that planned transmission infrastructure investments could double between 2026 and 2030 compared to today’s levels. This is why Siemens Energy needed further financial guarantee capacity.

|

Footnotes 1Grid Solutions: The design and management of High-Voltage Long-Distance power lines and associated software and technology, grid access services (connecting power plants or high-demand industrial facilities to electrical grids), grid stabilization services (increasing the reliability and stability of a complex grid with technology and software solutions), and Substations. 2Grid Products: Manufacturer and installation of transformers, switchgear, bushings, instrument transformers, and coils. Transformers transfer electricity from one circuit to another and can change the electricity voltage; switchgear protects electrical equipment from being overloaded, and the remaining products are used in substations, converter stations and throughout the transmission infrastructure. Opinions expressed herein by Massif Capital, LLC (Massif Capital) are not an investment recommendation and are not meant to be relied upon in investment decisions. Massif Capital’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is limited in scope, based on an incomplete set of information, and has limitations to its accuracy. Massif Capital recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies’ regulatory filings, public statements, and competitors. Consulting a qualified investment adviser may be prudent. The information upon which this material is based and was obtained from sources believed to be reliable but has not been independently verified. Therefore, Massif Capital cannot guarantee its accuracy. Any opinions or estimates constitute Massif Capital’s best judgment as of the date of publication and are subject to change without notice. Massif Capital explicitly disclaims any liability that may arise from the use of this material; reliance upon information in this publication is at the sole discretion of the reader. Furthermore, under no circumstances is this publication an offer to sell or a solicitation to buy securities or services discussed herein. Disclosure |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q4 2024 Earnings Call Transcript")

-to-IRA rollovers, Vanguard finds")