")

(NYSE:BABA)")

")

Investment Thesis

D.R. Horton, Inc. (NYSE:DHI) remains well-positioned to post good revenue growth in the coming quarters, driven by its strategy to address affordability challenges, which includes reducing home prices and sizes and providing attractive incentives to attract potential homebuyers. Additionally, the company saw improved customer traffic and demand as mortgage rates eased, especially in the latter half of the last quarter and into July, which should further accelerate as the Federal Reserve starts cutting rates. The company is also focused on increasing its community count, which should contribute to its revenue growth in the coming quarters and 2025. Besides organic growth, inorganic growth opportunities from M&A should also help the company drive revenue growth.

On the margin front, the potential reversal in the interest rate cycle should allow the company to reduce incentives, which should help margins in the medium term. Further, the company’s focus on improving build cycle time should result in increased productivity and operational efficiency, which bodes well for margin growth. I believe the stock can give mid-teen returns over the next 4–5 quarters as the interest rate cycle reverses. Hence, I have a buy rating on DHI stock.

Revenue Analysis and Outlook

Despite high mortgage interest rates and uncertain economic conditions, DHI has been benefiting from good housing demand supported by favorable demographics, and a limited supply of new and existing homes at affordable prices.

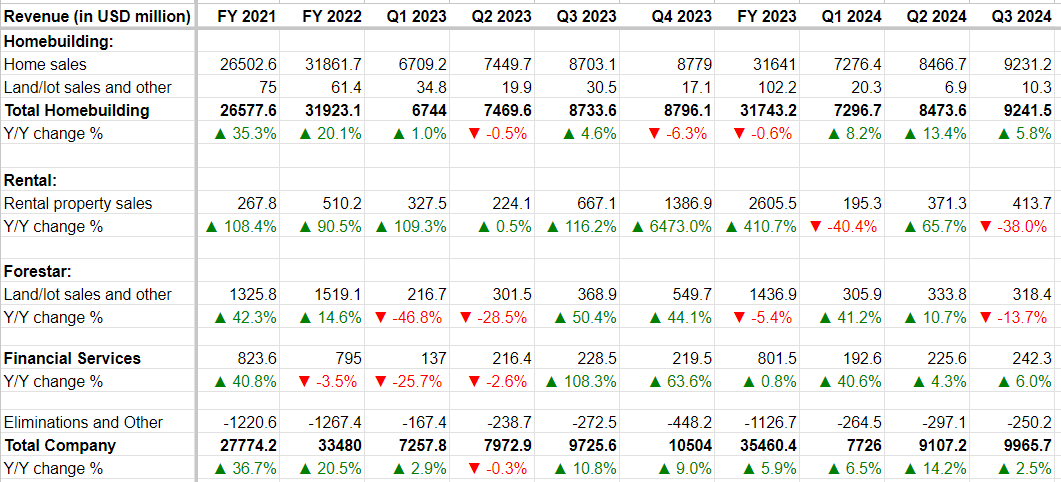

In the third quarter of 2024, the company’s total revenue increased by 2.5% Y/Y to $9.965 billion, primarily driven by a 5.8% Y/Y increase in homebuilding revenues. The Y/Y increase in homebuilding revenues was attributed to a 5.1% Y/Y increase in home closings to 24,155 units, and a 0.9% Y/Y increase in the average sales price of homes closed to $382,200.

DHI’s Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, I am optimistic about DHI’s revenue growth prospects. The last few quarters have been tough given the high interest rates. However, the company’s focus on affordable price points where the supply remained tight, as well as its strategy to address affordability challenges by reducing home prices and sizes, coupled with offering attractive incentives such as mortgage buydowns, has proven effective and DHI was able to grow revenues despite the macro headwinds. I expect the company’s leadership position, good execution, and focus on addressing affordability issues facing home buyers should help it post good growth moving forward as well.

Further, the recent data points around inflation have been positive, and mortgage rates have started coming down in anticipation of interest rate cuts. This should also help the company’s sales. During the Q3 FY24 earnings call, management noted that customer traffic and demand improved significantly as mortgage rates eased with the notable momentum towards the end of the quarter which continued in July. I expect this momentum to further accelerate as the Federal Reserve starts cutting interest rates.

The company’s efforts to increase its community count should also contribute to revenue growth in the coming quarters and next year. The company’s average selling communities increased ~12% Y/Y in the third quarter. Management anticipates mid-single-digit to high-single-digit growth in communities over the next few quarters, which should drive volume growth.

Additionally, the company is looking for small strategic tuck-in acquisitions to expand its footprint in new and emerging geographies and enhance its lot position in existing markets, which should also support its growth. Overall, I remain optimistic about the company’s growth prospects.

Margin Analysis and Outlook

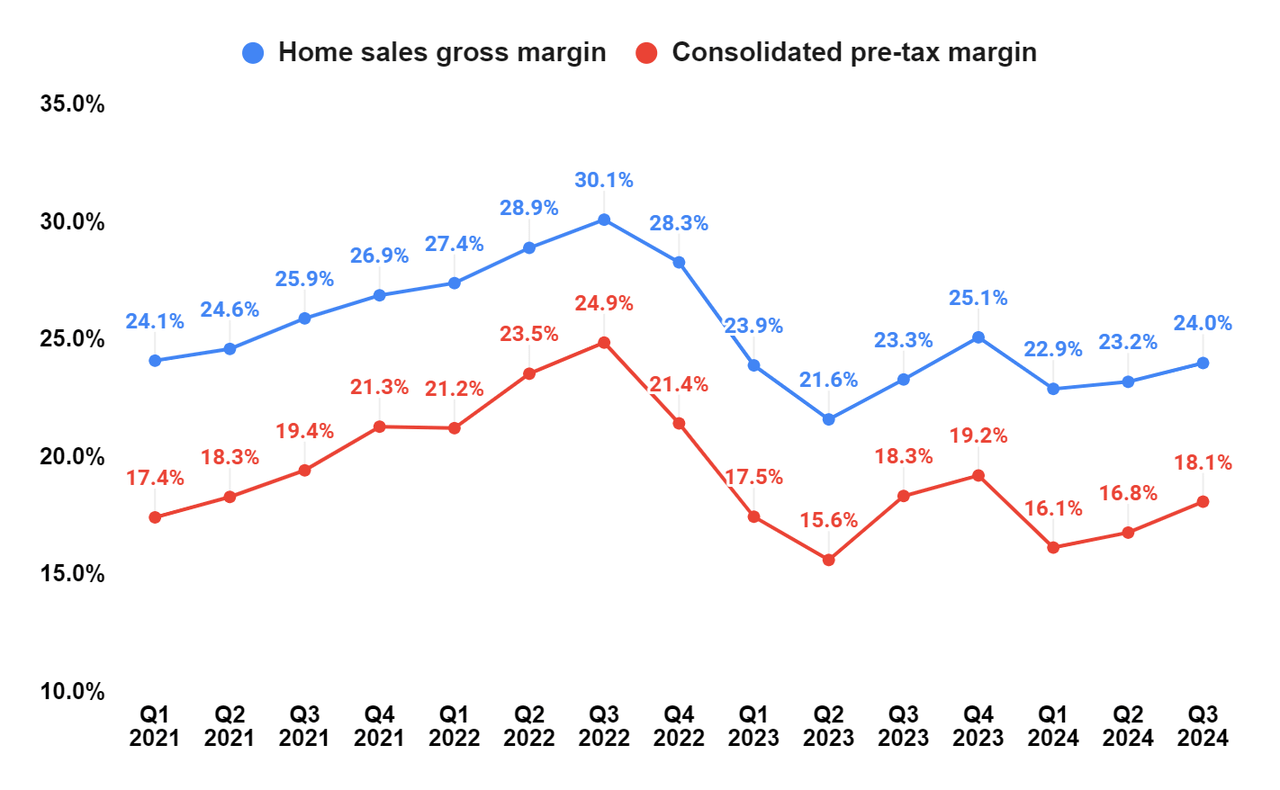

In Q3 2024, the company’s home sales gross margin expanded by 70 bps Y/Y to 24%, driven by a decline in stick and brick costs due to lower lumber prices, partially offset by higher lot costs. However, the consolidated pre-tax margin declined by 20 bps Y/Y to 18.1% as an increase in pre-tax margin in the homebuilding operations was more than offset by a decrease in pre-tax margin in rental operations. The lower rental operations pre-tax margin was due to a decline in home closings and a lower gross margin on home and unit closings.

DHI’s Home Sales Gross Margin and Consolidated Pre-Tax Margin (Company Data, GS Analytics Research)

The company’s medium-term margin outlook is positive. Over the last few quarters, the company had to incur costs related to mortgage rate buydowns, and other incentives in order to drive demand. However, with the interest rate cycle poised to reverse, I expect lower incentive costs moving forward. Further, labor and supply chain constraints continue to ease, and the company is improving build cycle time. So, I am expecting improved productivity and operational efficiency, which should help margins moving forward.

Valuation and Rating

D.R. Horton ended the last quarter with a tangible book value per share of $74.82. According to consensus expectations, the company is expected to report an EPS of $4.16 in Q4 FY24 and $15.83 in FY25. The company also has 30-cent per share quarterly dividends, or $1.50 per share in dividend payouts over the next five quarters.

So the company’s tangible book value per share should be around $93.31 (= $74.82 + $4.16 + $15.83 – $1.50) by the end of FY25 (ending September 2025). Over the last 10 years, the stock has traded at a P/TBV of ~2x. However, I expect it to trade at a slight premium around the FY25 end, given we will likely be in the initial stages of a housing recovery catalyzed by interest rate cycle reversal around that time. Applying a 2.2x P/TBV multiple to the FY25 end expected TBV per share of $93.31, we get a target price of $205.28 or ~16% upside from the current levels. So, I rate DHI stock a buy.

Risks

- I am expecting continued easing of mortgage rates and an interest rate cycle reversal in the coming quarters. However, if it doesn’t happen, it can negatively impact share prices.

- The housing market also depends on broader economic trends like GDP, consumer confidence, and unemployment levels. If there is a macro slowdown and these factors trend in an unfavorable direction, it may negatively impact the demand.

Read the full article here

")

(NYSE:BABA)")

")