")

")

")

")

Investing Environment

Following broad market participation that drove US equities higher in late 2023 and early 2024, markets narrowed in Q2, with a handful of mega-cap technology names lifting the S&P 500® Index to all-time highs on the AI FOMO (artificial intelligence “fear of missing out”) trade. NVIDIA, Apple and Microsoft alone contributed 85% of the S&P 500®’s 4.28% Q2 return. However, due to the market’s narrow breadth in Q2, the index’s strong headline result was not representative of the average stock’s performance. Most US stocks were in fact negative returners, with the median S&P 500® Index stock down -3.20%. This type of result was in line with the Russell Midcap® Value Index’s -3.40% Q2 return. Most sectors within the Russell Midcap® Value Index were weak. The worst performing were consumer staples, health care and materials—each down about 8%. Exceptions were information technology, utilities and real estate. Given their higher leverage, utilities and real estate were beneficiaries of falling longer-term bond yields as US inflation continues to cool.

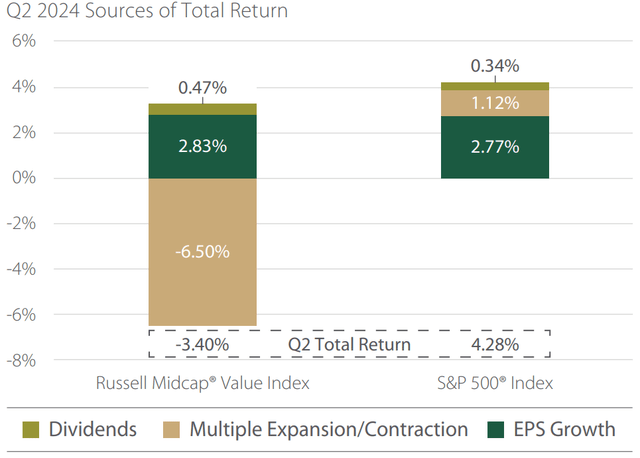

Given the meaningful outperformance by large-cap growth stocks, which drove the broad large-cap US indices higher, one might conclude that equity returns have simply followed earnings growth. However, as shown in Exhibit 1, Q2’s variance in returns between the S&P 500® and Russell Midcap® Value Indices was fully attributable to shifting valuations—multiple expansion of the former and multiple contraction of the latter. We will leave it to readers to draw your own conclusions about the market’s behavior. We will only point out that recent earnings growth for mid-cap value stocks has been just as strong as for their larger and growthier peers, and that mid-cap value stocks, which were already attractively valued relative to growth stocks based on history, have become even cheaper.

Exhibit 1: Size/Style Returns Explained by Multiple Expansion/Contraction…not Earnings Growth!

Source: Artisan Partners/FactSet/Russell/S&P. Multiple expansion/contraction represents price to earnings ratio. Past performance does not guarantee future results.

Performance Discussion

Compared to the Russell Midcap® Value Index, our portfolio performance was primarily held back by our health care and consumer discretionary holdings. Above-benchmark weightings in health care, consumer staples and consumer discretionary as well as a lighter weighting in utilities also contributed negatively to relative results. On the positive side, our financials, industrials and technology holdings outperformed.

In the health care and consumer discretionary sectors, Baxter International (BAX) and LKQ (LKQ) were key detractors. Baxter provides essential products in renal care, medication delivery, advanced surgery, clinical nutrition, pharma and acute therapies. Though quarterly results beat expectations and the company raised guidance, shares were down because some of the upside to results was in the renal care business, which is being sold to Carlyle Group (CG), whereas there was weakness in its healthcare services and technologies business—the legacy Hillrom business that it acquired in 2021. Baxter has sought to transform the company by selling several non-core operations, which will raise cash and simplify the business longer term as it focuses on profitable growth. Last year, it sold its BioPharma Solutions business at a significant premium, and this year it is exiting the kidney business. Given the company’s growth challenges over the past few years, patience among investors seems to be lacking. In our view, there is significant pessimism embedded in the stock price as it sells cheaply based on our sum-of-the-parts valuation analysis.

LKQ is the dominant player in salvage/aftermarket collision parts distribution in North America, with over 70% market share. In addition to continued cost inflation, lower-than-expected collision claims in North America due partly to a mild winter resulted in disappointing quarterly earnings. What was already a cheap stock when we initiated our position in January of this year has become even cheaper. At a 10X P/E, shares trade at a distinct discount to their historical 10-year average of 14X and are also cheaper relative to LKQ’s auto parts retailer peers, which arguably have similar long-term growth profiles. LKQ isn’t a fast-growing business, but it can grow 2% to 4%, and given its dominant market share and mid-teens return on tangible capital, we believe it should trade at a higher valuation. Over the last decade, LKQ has also become the largest mechanical parts distributor in Europe. As is the case in North America, independent European mechanics value LKQ’s reliable distribution and competitive pricing. The European business has improved operationally over the last five years as LKQ has focused on the integration of its various acquisitions to drive margin and free cash flow improvements. LKQ operates in end markets with limited cyclicality as 90% of revenues are tied to non-discretionary spending and reliably has strong free cash flow generation. The company also meets our requirement for a sound financial condition as its debt load is manageable at 2X EBITDA due to its attractive free cash flow. We added to our position on weakness.

Our overall biggest detractor was Globe Life (GL), a provider of life insurance, health insurance and investment products and services. Shares fell abruptly on a short seller’s report alleging widespread insurance fraud by Globe Life involving the writing of fictitious policies and artificially inflated financials. The one-day selloff wiped out over 50% of the company’s market value, but the stock has since recovered more than half of that loss. The company denied the allegations, retained outside counsel to conduct an independent investigation and is cooperating with the Department of Justice (DOJ). Per the recent 10-Q, management does not believe the DOJ investigation will result in a material liability. Our investment thesis on Globe Life over the years has been underpinned by its slow growth, conservative balance sheet and robust free cash flow returned to shareholders via buybacks and dividends. It is the tortoise to the market share. Events outside the short seller’s report have the team reviewing how much tech-infrastructure upgrades Globe Life may need to boost its internal processes and controls. While we question much of the short report’s accuracy, we nonetheless take the allegations and the market’s reaction seriously and are evaluating our investment case.

Turning to the positive side of the ledger, our top contributors were Analog Devices, NetApp (NTAP) and Arch Capital Group (ACGL). Analog Devices (ADI) is the second-largest analog semiconductor chipmaker in the world behind Texas Instruments (TXN). Investors are excited about the prospects of a cyclical recovery in semiconductors as ADI’s bookings have turned higher on improving demand and tight inventories. Initially purchased in 2006, ADI is one of our longest held stocks as the company has proven to be an excellent compounder of value due to its leadership position in a secular growth industry, strong balance sheet and cash-generating properties. ADI operates in attractive segments that offer high gross and operating margins and have sticky customers. Producing chips into applications that often have decades of longevity (autos, industrial, communications) and that are a small fraction of the overall cost within the value chain makes this business attractive and hard to displace once designed into the product/application.

NetApp is an enterprise data storage and solutions company with a specialization in all-flash (i.e., solid-state) storage. Sales of the company’s higher margin flash products (+17% y/y) boosted margins and helped offset rising NAND component costs. Notably, the mix shift to flash is driving structurally higher gross margins. The boom in AI infrastructure investment, though still a small portion of its sales, increases the potential long-term growth opportunity for the company’s storage solutions, and this element has likely contributed to the stock’s strong gains. While NetApp retains a healthy balance sheet and earns strong free cash flow margins, we used the stock’s strength to reduce exposure.

Arch, a global reinsurer, has experienced strong growth over the past year as reinsurance markets have been in an upswing in terms of pricing and premium growth, while rising interest rates boosted net interest income. Additionally, margins benefited from lower acquisition costs, better expense management and reduced catastrophe losses. In its mortgage insurance business, high interest rates are a headwind to top-line growth but a tailwind for margins. Arch is an industry leader capably managed by a long-tenured team that has achieved an enviable underwriting record while at the same time seeking opportunistic growth. It has shown discipline in pulling back from writing business when pricing is soft, patiently waiting for turns in the cycle to put its strong capital position to work.

Portfolio Activity

We made one new purchase in Q2, adding Genpact (G), a business process outsourcing (BPO) company. BPO companies are third-party providers of outsourced business services. Common areas that companies outsource are HR, finance/accounting and customer care. Other areas seeing strong trends toward outsourcing are supply chain, process automation and procurement. BPO companies need to build sufficient scale to compete, which leads them to specialize in specific service areas. Genpact has built domain expertise in a few select verticals where it can be No. 1 or No. 2, focusing on financial services, consumer, health care and high-tech manufacturing industries. Companies seek to partner with Genpact to improve productivity, increase competitiveness and drive better business outcomes. Genpact has over 129,000 employees in 35+ countries to enable its offerings. At its all-time highs in early 2022, Genpact shares were selling in the low $50s at around 22X FY1 earnings. Today, they sell in the low $30s at a 10X multiple. Though the business has performed well—continuing to generate free cash flow and grow earnings—the market has become concerned about Genpact’s future. Outsourcing is a tough industry. It’s labor-intensive, which can mean less pricing power, high rates of attrition and risks of labor arbitrage shifts, plus there is the need for continual technology investment. AI is also a risk. However, technological-driven automation isn’t new to this industry. Technology is continually replacing low-value work. However, Genpact is a not a commoditized body shop. The company has domain expertise, its contracts are long-term in nature, it provides services that are essential, and the tailwind of specialization via outsourcing appears to have a long runway. The business generates a lot of free cash flow, much of which is being returned to shareholders via dividends and share buybacks. At 10X enterprise value to EBITA for a business that should continue to grow, we believe odds are tilted in our favor.

We also added to our existing position in Vail Resorts (MTN), a premium skiing, lodging and resort company, that has fallen by nearly 25% over the past year. Mother nature didn’t cooperate this past winter, as there was below-average snowfall early in the ski season and highly variable temperatures. That contributed to reduced visitation, which had second-order effects on retail, rental and lodging activity. On the positive side, growth in advanced pass sales drove low-single-digit growth in lift revenues, while labor costs were well controlled. Vail is one of a couple dominant players in an industry that benefits from high barriers to entry due to the fixed supply of suitable mountains. Of course, this is a highly seasonal business, dependent on appetite for ski vacations and the right weather conditions, but the company has made strides to improve the business model by increasing the percentage of its business from the advance commitment pass product, which transforms the business from one of uncertainty and weather dependency to one of greater visibility and predictability. This provides stability and the ability to spend on capex during the off season to improve the guest experience, as well as pursue additional footprint expansion.

We sold one stock in Q2: Jones Lang LaSalle (JLL), a commercial real estate brokerage and property services provider. Leasing and capital markets activity has significantly improved since our initial purchase in 2020 when pandemic-driven uncertainty loomed over the office real estate market, and JLL’s stock has responded positively. So, we chose to recycle capital into more attractive opportunities.

Perspective

“It’s a market of stocks, not a stock market.”

We are not sure where this saying originated, but its implication is particularly salient in 2024. Market concentration (% weight of top 10 stocks in the S&P 500® Index) is at all-time highs, and correlations of stocks to the broader market (the degree to which returns of individual stocks reflect the index return) have fallen to all-time lows. The S&P 500® Index, which has become increasingly concentrated among a few mega-cap stocks, no longer represents the diverse opportunity set that exists within the US equity market.

We are ultimately stock pickers, but when we look at the valuation gaps that exist between mid caps and large caps and value versus growth, these relative spreads have reextended to highly attractive levels. Compared to P/Es of 22.4X and 27.8X (FY1 earnings) for the S&P 500® and Russell Midcap® Growth Indices, the Russell Midcap® Value Index sells for just 16.1X. Not since the dot-com bubble have these valuations spreads been this attractive. Our portfolio is even cheaper at 14.3X. Most importantly, we do not believe we are having to sacrifice quality in the current environment to find attractive values. Consistent with our approach of seeking to create a portfolio that is better, safer and cheaper than our benchmark, our portfolio has a greater median ROE (17.2% versus 10.5%) and median higher fixed charge coverage (5.8X versus 4.0X) than the Russell Midcap® Value Index. While we can’t predict the next recession, the outcomes of upcoming elections or the direction of the market, we feel good about the characteristics of the portfolio we have built.

Read the full article here

")

")

")

")

")