")

")

")

")

We have always been taught that the best time to invest is after a market crash when valuations are low.

Yet, when that crash actually occurs, very few investors actually have the courage to take action and will instead say things like:

“This time is different”

and

“We have not hit the bottom yet”

We have seen this repeat many times in history and yet, people never learn.

But the reality is that each crisis is different, but the end outcome is always the same: a recovery.

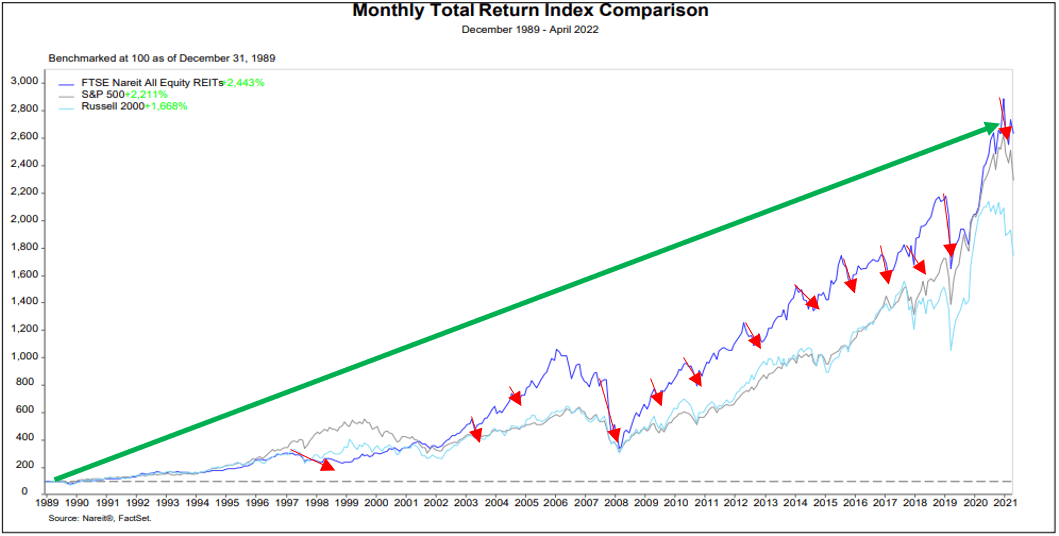

NAREIT

Moreover, it isn’t possible to time a bottom, so why even try?

Therefore, if you think rationally, you should invest when valuations are low and keep a long-term mindset. Yes, you probably won’t get in right at the bottom, but that does not matter.

This brings me to real estate investment trusts, or REITs (VNQ) in short.

I think that they are today offering a once-in-a-decade opportunity to win big in the coming years, and very few investors seem to be paying attention.

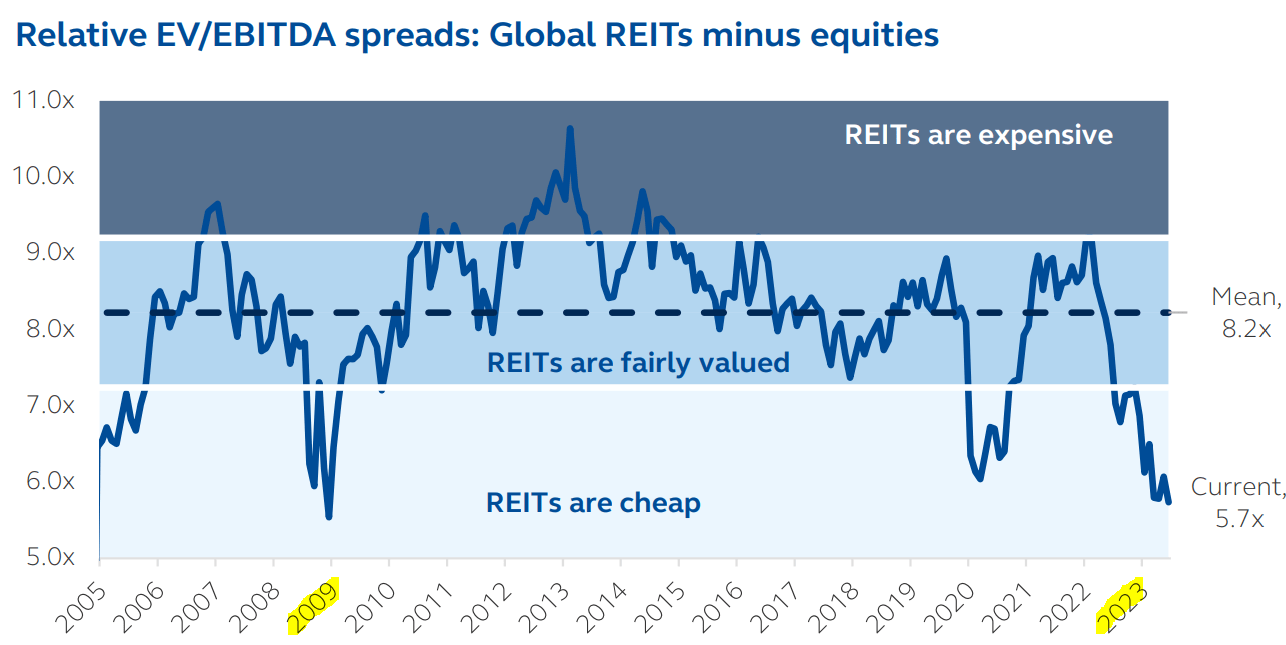

I know that the phrase “once-in-a-decade opportunity” phrase is overused, but here’s the thing: REITs have crashed, and their valuations are quite literally at their lowest in 16 years:

Principal Asset Management

Best of all, I think that the reason why they are discounted is temporary.

The surge in interest rates caused a lot of income-oriented investors to sell REITs to buy bonds and treasuries, and this explains why REITs crashed.

But interest rates are now expected to be cut in the near term, and I expect many of the same investors to rush back into REITs as they realize that the income that they expected to earn from treasuries wasn’t sustainable after all.

The debt market is now pricing a ~100 basis point cut within a year from now, and many Central Banks in Europe and Canada have already begun to cut rates:

Corporate Finance Institute

This should be a very powerful catalyst for REITs.

They crashed due to rising rates, and therefore, they should also recover as rates are cut.

And it gets even better…

Right as interest rates are cut, rent growth is also expected to accelerate in most property sectors because most new construction projects have been put on halt.

Therefore, all the recent negative headlines could soon turn into an avalanche of good news as the focus shifts from “rising interest rates” to “declining interest rates and undersupply-fueled rent growth”

Some REITs could surge by 50%+ as their valuations recover closer to their historic norms and while you wait, you also earn steady dividend income.

Here are three REITs that are offering a historic opportunity:

BSR REIT is our largest apartment REIT investment. It stands out in its peer group due to 5 key reasons:

- Nearly all of its properties are in rapidly growing Texan markets that are expected to attract significant population and job growth over the coming decade.

- It focuses primarily on Class B affordable properties with an average rent of just $1,500, which makes it more resilient to recessions and new supply.

- The rent-to-income ratios in its markets are also much lower than in coastal markets at just 20% vs. 35%, providing significant rent growth potential as these Texan markets grow in popularity.

- The management is the biggest shareholder of the company, so they are truly looking for shareholders. Today, they are aggressively buying back shares while they are heavily discounted.

- Despite enjoying some of the best growth prospects, its shares are some of the most heavily discounted in its peer group, trading at a 35% discount to their net asset value, and 12x cash flow. Just to return to their net asset value, the share price would need to appreciate by 50%, and BSR actually traded at a 10% premium to its net asset value in early 2022.

BSR REIT

BSR REIT

We just recently had the chance to interview the company’s management, and here are some of the main highlights.

When asked about their current valuation, here is what they said:

Right now, at $11.50, I think you’re buying BSR at $135,000 a unit. I haven’t seen $135,000 a unit for what we own in my career ever. Meanwhile, eight of the top ten fastest-growing counties in the United States are located in Texas. DFW and Houston lead the nation in numeric population growth.

The cost to build new apartment communities is today closer to double that, so you are getting a steep discount relative to replacement cost for high-quality assets in growing markets.

We then asked whether they would consider selling the company to a bigger private equity company, and they answered that:

“We’re for sale every single day; you can buy one or all the shares on the stock exchange. If a buyer presents a value that provides exceptional total return potential for our investors, we will engage. Our management team owns 45% of the company, so we’re aligned with our investors on maximizing value.”

That’s exactly what I like to hear from a management team.

Blackstone (BX) just recently bought out two residential REITs that were priced at low valuations and were willing to pay a substantial premium. Moreover, KKR (KRR) just announced that it would acquire a $2 billion apartment community from Lennar (LEN) and it is paying $400k+ per unit.

The growth prospects are limited in the near term because a lot of supply is hitting the market, but over the long run, these assets will almost certainly grow their rents and value.

Paying 65 cents on the dollar is a rare deal and I won’t let it pass by.

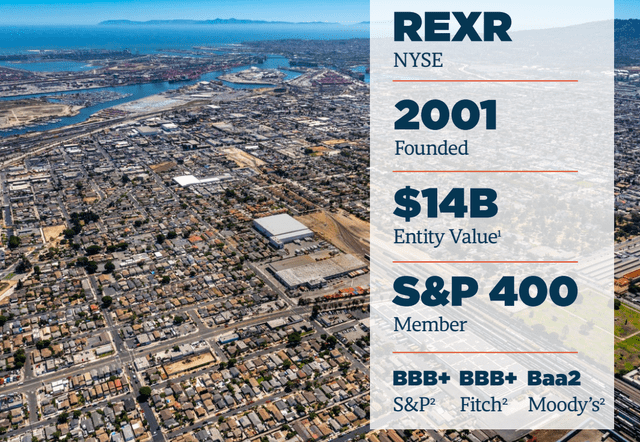

Rexford Realty Trust (REXR)

Tier-1 industrial REITs have recently become opportunistic.

- Their share prices have dropped significantly in recent years despite continuing to grow their cash flows at a rapid pace, and as a result, they are now priced at historically low valuations of around 19x FFO and a ~20% discount to their net asset values.

- They enjoy a huge mark-to-market in their portfolio as their rents have fallen deeply below market, which should allow them to hike rents by up to 50% as their leases gradually expire in the coming years.

- They also have a lot of development/redevelopment opportunities that should allow them to grow externally in addition to their rapid organic growth prospects.

First Industrial Realty Trust

And one of our favorites is Rexford Industrial Realty (REXR). It stands out in its peer group in that:

- It uses less leverage.

- It is bigger in size.

- It focuses on markets with lower risk of oversupply.

- It has less ground-up development risk.

- It has some of the most predictable growth prospects.

REXR is 100% focused on infill locations in SoCal, which is the strongest industrial market in the US. Below is a good example of what an infill location in SoCal looks like. It is almost impossible to bring new supply into these markets, but the demand for industrial real estate is ever-growing due to the growth of e-commerce, onshoring & nearshoring, broader GDP growth, and the strategic location on the West Coast for import/export businesses.

Rexford Realty Trust

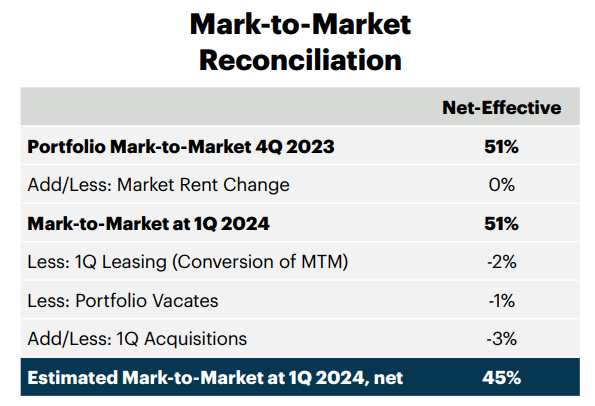

As a result, SoCal has the lowest vacancy rate in the nation at just 3% and the rent growth has been so strong that REXR now has a 45% mark-to-market across its portfolio:

Rexford Realty Trust

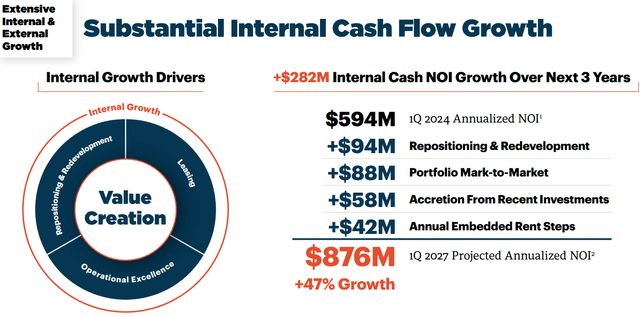

This mark-to-market, coupled with some additional investments, is expected to result in 47% growth within the next 3 years alone, and that won’t even exhaust their entire mark-to-market opportunity:

Rexford Realty Trust

Other industrial REITs have similar strong growth prospects, but those of REXR are arguably even more predictable because of the supply-constrained nature of SoCal.

Despite that, it is almost as cheap as its peers.

It is today priced at an estimated 19x FFO and a 20% discount to its net asset value.

18.5x FFO may not seem that low, but it is important to remember that this is based on today’s rents, which are deeply below market. If you now adjust its rents ~50% higher and add to that some external growth, you get a very low valuation multiple in just a few years from now unless its share price adjusts higher.

The same applies to the dividend. The current dividend yield is 3.5%, but it has been growing at 18% per year on average over the past 5 years, and at this rate, it will already reach 4% with the next hike.

That’s the fastest growth rate that I know in the REIT sector.

If you expect the dividend to grow at 12% per year going forward, your yield on cost will be ~6.5% in 5 years from now, and this growth rate is not unattainable for REXR given its massive mark-to-market opportunity.

SBA Communications (SBAC)

We believe that cell tower REITs have become deeply undervalued.

They are today trading at their lowest valuation multiples in over a decade, they are buying back shares, and even attracting the attention of activist investors.

We already hold a large position in Crown Castle (CCI) as part of our Retirement Portfolio, and we think that it is the best opportunity for investors who want to maximize income.

But recently, we also included SBA Communications (SBAC) in our Core Portfolio because we think that it is at least equally attractive for more risk-tolerant investors who are seeking to maximize total returns because:

- SBAC is a lot smaller in size.

- It retains more cash flow for growth.

- It invests in riskier foreign markets.

Here are its results so far:

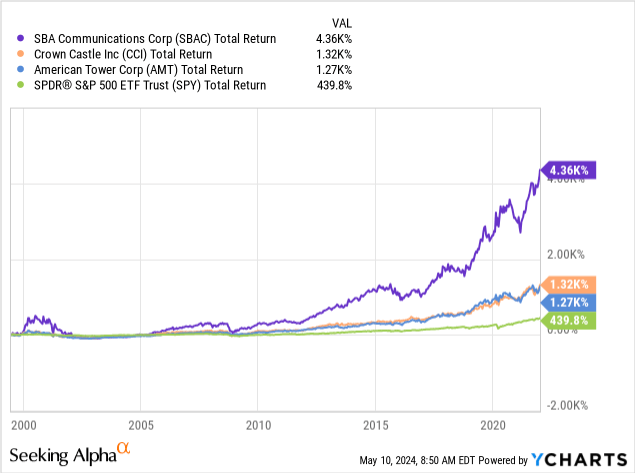

YCHARTS

All three cell tower REITs have massively outperformed the S&P500 (SPY) over the long run, but SBAC is still miles ahead of its peers. It has done an even better job at allocating capital into the most accretive investment opportunities, and managed to earn larger spreads over its cost of capital.

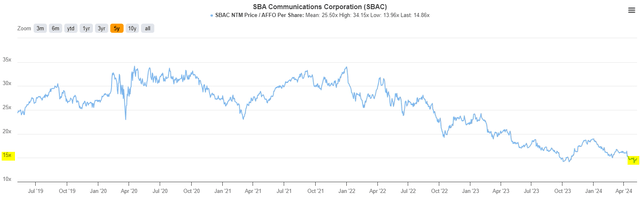

But today, it is the cheapest it has been in a very long time. Its share price has dropped by about 50% since the beginning of 2022 even as its AFFO per share grew from $10.74 at the end of 2021 to $13.21 expected this year.

As a result, it is now priced at just 15x AFFO, down from 35x at its peak, and 25-35x during most times in the past years. Even at the bottom of the pandemic crash, it still traded at 23x FFO, but today, you can buy it at 15x:

TIKR

I believe that SBAC was too expensive in 2020/2021 when interest rates were near zero, but it is today too cheap due to fears of higher interest rates.

The market went from one extreme to another, and it has opened a rare opportunity to buy this exceptional REIT at a historically low valuation.

For the first time in a long time, SBAC is now even buying back shares. In the last quarter alone, they bought back $200 million worth of shares at an average price of $213.85 per share.

They thought this was too good of an opportunity to let pass by. But today, it is even cheaper, trading at $196 per share, and therefore, we can expect these buybacks to continue.

Why did it get so cheap?

It is the same reason why CCI and AMT have dropped as well. It is a combination of fears of higher interest rates and the near-term headwind caused by T-Mobile’s acquisition of Sprint. It will lead to a slowdown in growth in 2024 and also in 2025, and this is a big problem in the eyes of most investors, since they only care about the short-term.

But if you can think long-term like a real landlord, this is a great opportunity because growth should accelerate in 2026. Here are the average analyst estimates for AFFO per share for the coming years:

| 2024 | 2025 | 2026 | 2027 | 2028 |

| 13.21 | 13.20 | 13.48 | 14.51 | 15.37 |

As you can see here, its AFFO per share is expected to rise by 16% by the end of 2028, and that’s despite experiencing very little growth until 2026. Its growth could also be more significant if interest rates return to lower levels.

SBAC runs on a bit more leverage than American Tower at 6.5x, but that’s still fairly conservative for a cell tower REIT of this quality. It is actually a historical low for SBAC and below its target of 7-7.5x.

So in short, I think that the market is overreacting here to near-term headwinds and forgetting about SBAC’s rapid long-term growth prospects.

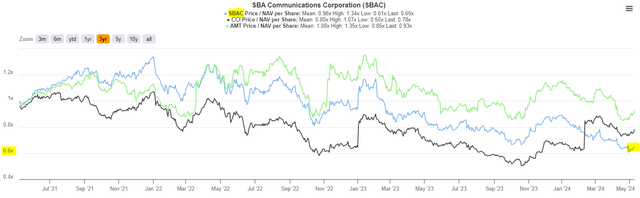

Its P/AFFO is the lowest since the great financial crisis, and its P/NAV is the lowest ever since there was a consensus NAV estimate from analysts. Currently, it is at 0.68x, materially lower than that of its peers Crown Castle and American Tower:

TIKR

Simply returning to its NAV and a more reasonable P/AFFO multiple would require 50% upside from here, and I believe that this will happen once SBAC’s growth accelerates past 2025 and/or when interest rates return to lower levels.

In the meantime, the dividend yield is very low, and this is likely why so many investors have lost patience. Even after its crash, its dividend yield is just 2%, but this is because its payout ratio is very low at just 30%.

Generally, 2% would be too low for a “high yield landlord”, but remember that what really matters is the average yield of our portfolio, and it is today at near 6%, despite the very low average payout ratio of most of our REITs.

Moreover, I view this low payout ratio as an advantage in this specific case since cell tower REITs have great investment opportunities, but their cost of capital is too high right now. Retaining the cash flow allows it to organically reinvest in buybacks, deleveraging, and other investment opportunities, and it is more tax-efficient for us than receiving a bigger dividend.

Finally, the dividend is growing very rapidly. It was just recently hiked by another 15%, and this continued rapid growth should serve as another catalyst for the stock.

Closing Note

REITs are still priced at a decade-low valuation, despite actually performing well:

- REITs use little leverage, with an average LTV of just 30%.

- REIT debt is mostly fixed-rate and maturities are long and well-staggered.

- REITs benefited from the inflation as it resulted in faster rent growth.

But the clock is now ticking for REIT investors.

The window of opportunity could be soon closing because REITs enjoy a very powerful catalyst in the near term.

Interest rates are expected to be cut, and rent growth is also likely to accelerate. The combination of these two factors should greatly improve their market sentiment and lead to an epic recovery.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")