")

")

")

Introduction

In April, I wrote an article on Remy Cointreau (OTCPK:REMYF) (OTCPK:REMYY) discussing the company’s prospects for this year. I thought FY 2025 (the current financial year as Cointreau’s financial year ends in March) should be much better for Cointreau after what I was expecting to be a poor FY 2024.

The company has now published its annual report for 2024, and as feared and expected, FY 2024 wasn’t great. But much to my surprise, the market didn’t appear to be prepared for what I thought was a widely expected weak performance in 2024 and Cointreau’s share price is currently trading approximately 24% lower than in April and is now trading about 67% below its December 2021 high. A head-scratcher, and I wanted to have another look to see if I either missed something or if I need to upgrade my thesis and conclusion for the French distillery. To get a better overview of the company’s history and activities, I’d recommend you to read my older articles here.

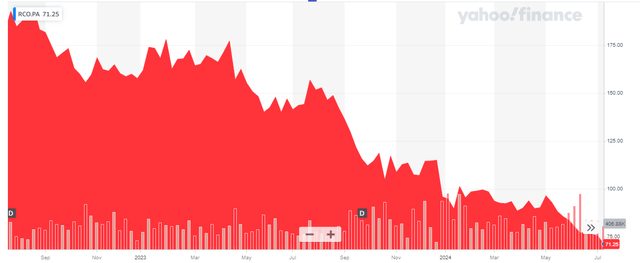

Yahoo Finance

Remy Cointreau has its primary listing in France where it’s trading with RCO as ticker symbol. The average daily volume is approximately 107,000 shares per day which makes the French listing the most liquid trading venue. The most recent share price was 71.25 EUR, and considering there are roughly 50.7M hares outstanding, the market capitalization is currently approximately 3.61B EUR.

The final results of FY 2024

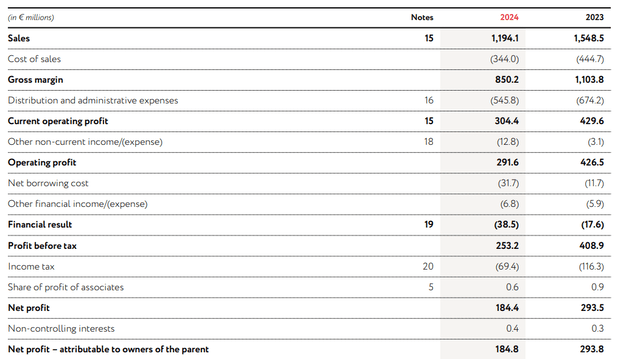

As expected, the result in FY 2024 wasn’t good. Revenue fell by in excess of 20% to just under 1.2B EUR and although the company was also able to reduce its COGS by almost 25%, this obviously wasn’t sufficient to keep the gross profit even remotely stable. As the income statement below shows, Remy Cointreau had to deal with a 253M EUR decrease in its gross profit, which is almost 23% compared to the preceding year.

RCO Investor Relations

Fortunately some of the other expenses decreased as well, but thee financial expenses increased on the back of higher interest rates, and this ultimately resulted in a 38% lower pre-tax income which fell to 253.2M EUR. After deducting the amount of taxes owed on that, the net profit was 184.4M EUR and 184.8M EUR was attributable to the common shareholders of Remy Cointreau. This represents an EPS of 3.64 EUR.

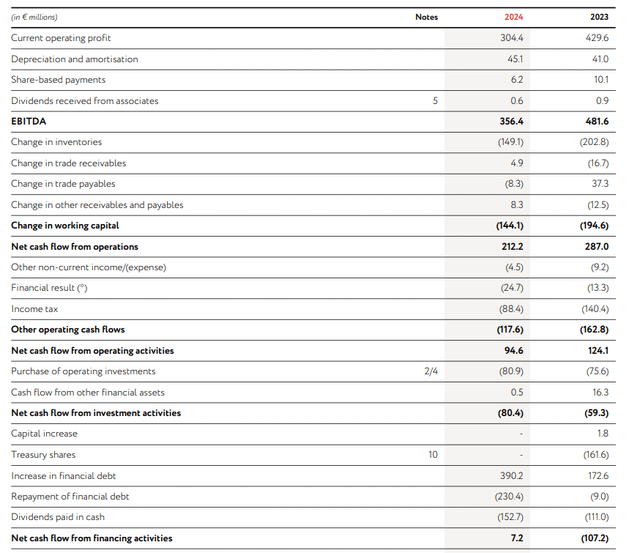

Cointreau continues to invest in growth (including additional capacity to let certain cognac age before marketing the product) but fortunately its operating cash flow is strong enough to cover those additional investments. As you can see below, the total operating cash flow was a 94.6M EUR but this included a 144M EUR change in the working capital position while it also included 88.4M EUR in cash taxes although only 69.4M EUR was owed based on the income statement. And to be complete, we should also deduct 8M EUR in lease payments.

RCO Investor Relations

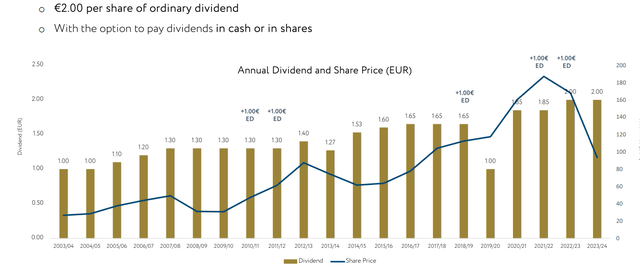

This means the adjusted operating cash flow was approximately 250M EUR. The total capex was 81M EUR, which means the underlying free cash flow was approximately 169M EUR which translates into a FCFPS of 3.33 EUR per share. Cointreau is proposing to pay a dividend of 2.00 EUR per share, and the stock will trade ex-dividend in the coming week. The French dividend withholding tax for non-residents is 12.8%. The dividend will be payable in cash or stock.

RCO Investor Relations

The stock is now trading at a free cash flow yield (including growth investments) of approximately 5%, which is reasonable. The earnings multiple of 18 is also relatively reasonable for a leader in the premium segment anticipating 72% gross margin by the end of this decade. And with a total net debt of 650M EUR, the debt ratio of just under 1.70 (despite the substantially lower EBITDA) isn’t bad either. The company is currently trading at an EV/EBITDA ratio of 12.

Will we indeed see growth this year?

While those metrics are okay in case 2024 was an exceptionally weak year, I obviously want to make sure Remy Cointreau at least has a chance to see its EBITDA (and free cash flow) increase again. Cointreau’s management was pretty vague when it presented its outlook for the current financial year, calling it a “year of transition” while FY 2026 should allow the company to pursue growth again.

Reading between the lines, this sounds like we shouldn’t expect much from Remy Cointreau this year. And indeed, the consensus estimates for this year are banking on a 350M EUR EBITDA, which should ultimately result in a 191M EUR net profit for an EPS of 3.63 EUR per share.

However, from FY 2026, the company should indeed be able to grow its revenue again by the high-single digit percentage that has been promised by its management. The consensus estimates for FY 2026 and FY 2027 respectively call for a 391M EUR EBITDA and a 430M EUR EBITDA respectively. In 2027, this should result in an EPS of 4.74 EUR per share which means the stock is currently trading at just 15 times its FY 2027 earnings.

Investment thesis

While a multiple of 15 times earnings in two years time still sounds high, keep in mind RCO is a world leader in its segment and the stock will likely never be cheap. I expect the net debt level to remain stable (the net free cash flow will be spent on growth and the dividend, I don’t expect any net cash to hit the balance sheet) which should indicate the EV/EBITDA ratio will fall to around 10 by FY 2027. Again, a multiple of 10 times EBITDA does not sound outrageous. In the past few years, Cointreau traded at around 20 times EBITDA, while comparable companies Brown-Forman and Diageo are trading at a forward EV/EBITDA of respectively 15 and 13, based on consensus estimates. Applying a forward EV/EBITDA of 14 on the EBITDA consensus of 430M EUR in FY 2027 would result in a fair value of 106 EUR. Discounting that back to today (two years) at an 8% discount rate would result in a current fair value of around 90 EUR per share. Straightening the issues with China on the anti-dumping accusation would be a major boost to Remy Cointreau as that negative overhang obviously also has an impact on its share price. I hope the cognac producers can find a solution soon as that would definitely remove another element that is holding the share price back.

And that’s why I will soon initiate a long position in Remy Cointreau. I had the stock high on my watchlist after my recent April article, but as the share price continued to decrease I remained on the sidelines. But I think we are now entering deep value territory here as the entire business, including the intangibles related to the leading brand names, is now valued at just over 4B EUR. And that actually could make Remy Cointreau an attractive candidate for another company to expand its brand portfolio at a relatively low cost, potentially unlocking synergy benefits in the process.

I will likely start buying stock on the open market while also writing put options (in a combination of in the money and out of the money put options).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")