")

Investment Thesis: I rate America Movil as a buy.

In a previous article back in October, I made the argument that America Movil (NYSE:AMX) has good prospects for upside going forward, on the basis of strong LTV trends as well as a reduction in long-term debt.

Since my last article, the stock is up by just over 8%:

TradingView.com

The purpose of this article is to assess whether my bullish thesis for the stock still holds and whether the stock has the capacity to see further upside from here.

Performance

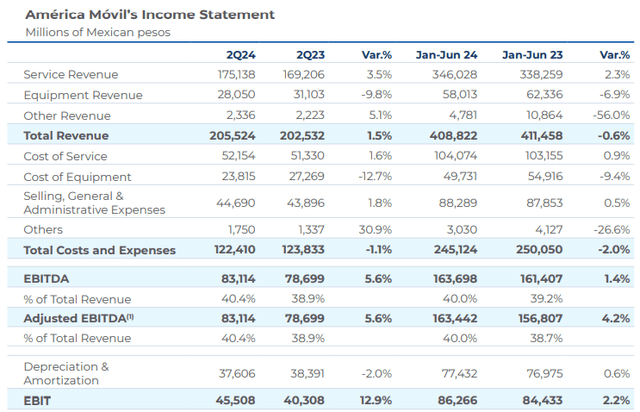

When looking at earnings results for Q2 2024 as released on July 16, we can see that total revenue was up by 1.5%, which was in large part due to growth in service revenue of 3.5%.

America Movil Q2 2024: Financial and Operating Report

While revenue growth has remained modest, it is encouraging that we are seeing growth once again. When I last covered America Movil, Q3 2023 results showed that service revenue was down by -4.3% as compared to the prior year’s quarter, while total revenue was down by -3.3% over the same period.

However, I had also made the qualification that this was primarily due to the appreciation of the Mexican peso against the U.S. dollar. On a constant currency basis, service revenue was actually up by 3.8% over the period. For the most recent quarter, service revenue saw growth of 4.7% at constant exchange rates. In this regard, the fact that service revenue has been growing in spite of currency headwinds is encouraging.

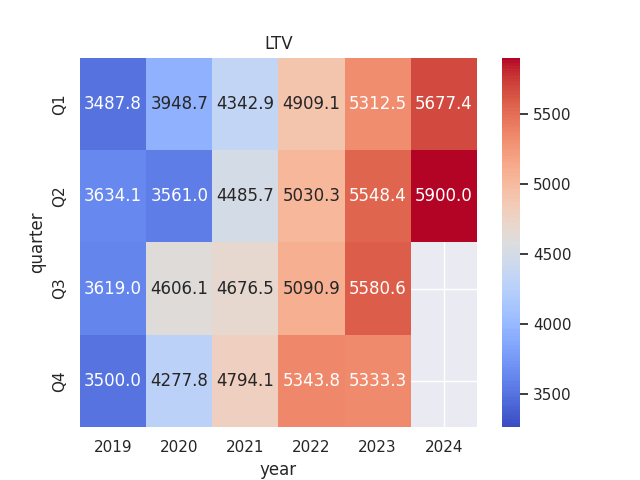

I had previously argued that given Mexico remains by far the largest market for the company by revenue – the fact that we have been seeing LTV (or customer lifetime value) increase across this market has been encouraging.

To calculate LTV, ARPU and churn rates for Mexico (across all wireless subscribers – postpaid and prepaid) were sourced and LTV was calculated by quarter as follows:

LTV = (ARPU / churn %) * 100

When looking at LTV for Q2 2024, we see that the same is up by over 6% on that of Q2 2023.

Heatmap generated by author using Python’s seaborn visualization library. LTV by quarter calculated by author – all figures in Mexican pesos.

This was due to both growth in ARPU (in Mexican pesos) from 172 in Q2 2023 to 177 in Q2 2024, along with a reduction in churn from 3.1% to 3% over the same period.

From a balance sheet standpoint, we can see that the company’s long-term debt-to-total assets ratio is up slightly from that of December 2023.

| Dec 2023 | Jun 2024 | |

| Long-term debt | 339,713 | 403,527 |

| Total assets | 1,564,186 | 1,662,997 |

| Long-term debt-to-total assets ratio | 21.72% | 24.27% |

Source: Figures (in millions of Mexican pesos) sourced from America Movil Q2 2024 Financial and Operating Report. Long-term debt-to-total assets ratio calculated by author.

In addition, we see that the quick ratio (total current assets less inventories all over total current liabilities) is up slightly over the same period, but remains less than 1 – indicating that America Movil does not have sufficient liquid assets to meet its current liabilities.

| Dec 2023 | Jun 2024 | |

| Total current assets | 340,167 | 348,195 |

| Inventories | 19,272 | 23,247 |

| Total current liabilities | 515,246 | 491,366 |

| Quick ratio | 0.62 | 0.66 |

Source: Figures (in Mexican pesos) sourced from America Movil Q2 2024 Financial and Operating Reports. Quick ratio calculated by author.

I had previously argued that in spite of the company having a quick ratio below 1 – investors would be willing to tolerate this for as long as we saw continued reduction in long-term debt as well as continued growth in LTV.

While long-term debt itself is up by 18% since December 2023, we see that growth in the long-term debt-to-total assets ratio has been more modest. In this regard, the company has continued to show a stable balance sheet on the whole, and revenue and LTV growth for the most recent quarter has been encouraging.

Looking Forward and Risks

In terms of growth prospects for America Movil going forward, wireless subscriber growth across the Mexican and Brazilian markets has been encouraging – and a continuation of this growth is likely to allow the stock to rise further.

With America Movil currently holding 64 percent of the share of wireless subscribers in Mexico, the company is in a good position to maintain its competitive advantage across this market. Across Mexico, America Movil added 148,000 new broadband accesses in the most recent quarter across both prepaid and postpaid customers to reach a total of 84.2 million wireless subscribers, which includes 12.8 million 5G subscribers.

It is estimated that 5G subscribers in the Mexican market are expected to reach 87 million by 2030, as compared to 16.9 million in 2025. This marks a substantial opportunity for America Movil to continue expanding its reach and bolster wireless subscriber growth.

One potential risk that I see in this regard is that with competitor Movistar having recently reached an agreement with AT&T (T) to extend its use of the latter’s 5G service network – which has the potential to increase competition in this space and could affect America Movil’s capacity to bolster wireless subscribers. However, I take the view that the risk of this is minor given the company’s existing reach across this market.

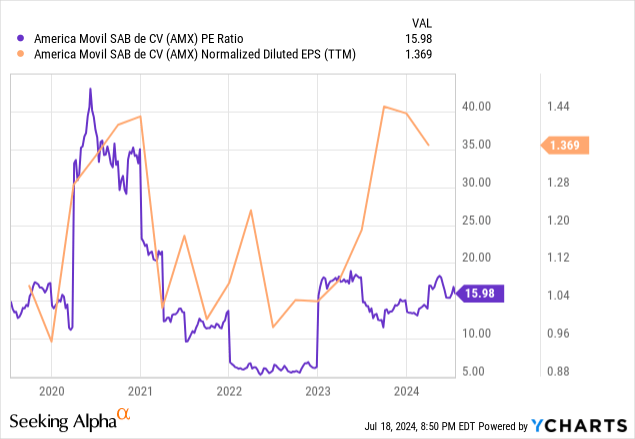

I had previously made the argument that on the basis of America Movil having previously traded at a similar level to that seen in 2019 but with earnings per share having trailed higher – the stock was potentially undervalued and could see an upside to the $22 mark.

ycharts.com

Since then, we have seen the P/E ratio remain steady over the past year – while earnings per share has seen a topping out of growth for now. In this regard, I take the view that the stock is trading at fair value at the current price of $17, but has the capacity to see further upside to the $22 mark if revenue growth continues to remain resilient.

Conclusion

To conclude, America Movil has seen resilient revenue performance, and LTV growth has continued to remain impressive. I take the view that the company has strong prospects to further grow its wireless subscriber base given the anticipated growth in 5G demand. For these reasons, I rate America Movil as a buy.

Read the full article here

")