")

Stock: Unpacking This Newly Listed Tech Co.")

Background

Ever since the public market debut of Meta’s (META) Facebook platform, investors have raced to discover the ‘next big thing.’ For a while, Snap Inc. (SNAP) seemed to hold promise as a rival platform that could deliver monster returns to investors. Twitter (now X, and privately held) engendered the same feelings. Ultimately, however, both of those platforms failed to generate the same degree of return consistently for shareholders. One late-comer to the social media public market is Reddit (NYSE:RDDT).

Since going public in March of this year, things have been fairly good for the stock and its shareholders.

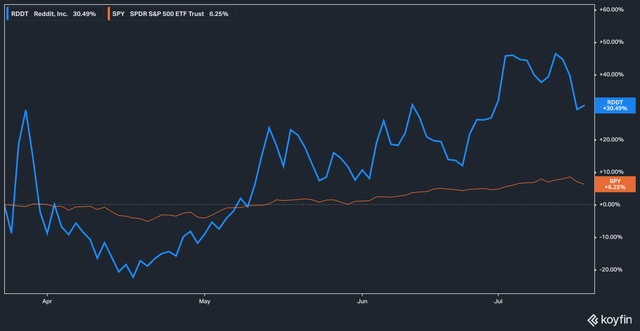

RDDT vs SPY total return (Koyfin)

Since its debut, Reddit has delivered a 30% return to shareholders, compared with the broader S&P 500’s (SPY) return of 6% for the same time frame. So, should investors expect big returns in the future from Reddit? Let’s dive in.

Old Problem, Novel Solution

One of our main focuses when researching a company is how a company, more or less indirectly, treats its shareholders – do common shareholders get at least a nominal vote in how things are done, or does the company issue excessive amounts of stock to the detriment of investors?

Like so many of its tech brethren, Reddit has multiple types of common stock – Class A, Class B, and Class C. Class A is a run-of-the-mill share, with one vote allocated. Class B shares are super shares, with 10 votes each. Class C shares have no voting rights. According to Reddit’s S1, this means that Class B shareholders control 97.1% of overall voting power.

For some companies, this structure has created a perception issue – Snap famously raised the ire of investors by allowing its founders near total control over common shareholders, for example. But Reddit appears to have taken a slightly different path, in the form of provisions that allow for the eventual conversion of Class B shares into Class A shares.

From the most recent 10-Q:

Shares of Class B common stock may be converted to Class A common stock at any time at the option of the stockholder. In addition, each share of Class B common stock will convert automatically into one share of Class A common stock (i) upon any transfer, except for certain permitted transfers set forth in the Restated Certificate, including transfers to family members, certain trusts for estate planning purposes, entities under common control with or controlled by such holder of our Class B common stock, and with respect to Advance Magazine Publishers Inc., any Advance Entity (as defined in the Restated Certificate), or (ii) upon the first date on which the aggregate number of outstanding shares of Class B common stock ceases to represent at least 7.5% of the aggregate number of then-outstanding shares of our Class A and Class B common stock.

All of that may sound like legal boilerplate mumbo jumbo, but it is important – under certain conditions – the transfer of shares by Class B shareholders could result in those shares being converted to Class A. While it sounds nice, we think the likelihood of it happening is relatively low.

The second method is a bit more plausible, at least in theory. Under the second method, should Class B shares represent less than 7.5% of the aggregate number of A and B shares outstanding, they will convert to A shares.

Buried deep on page 202 of the S1, the ‘Description of Capital Stock’ shows that the company is authorized 140 million shares of Class B capital stock and 2 billion shares of Class A capital stock. What this means to us, in effect, is that management will at least have to be mindful of the amount of Class A stock-based compensation or stock issuance it undertakes.

While nothing is ever foolproof, it is a novel way for a company to assuage shareholder concerns of mass dilution.

The Network Effect

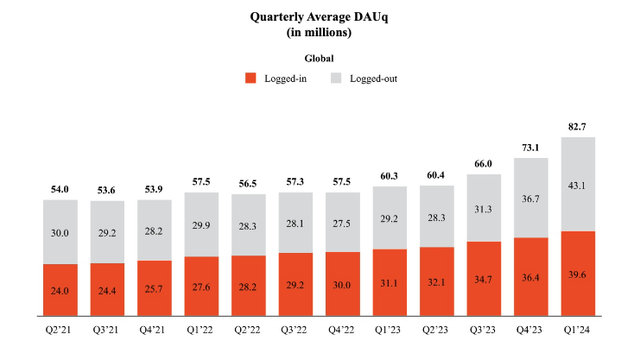

One of the biggest hurdles for any social media platform is attracting, retaining, and growing its user base. Reddit uses a relatively standard measure for the industry, which it calls Daily Active Uniques (DAUq), which is defined “as a user whom we can identify with a unique identifier who has visited… or opened a Reddit application at least once during a 24-hour period.”

On this all-important front, Reddit seems to be doing well:

Reddit DAUq (Quarterly Report)

For the three months ending March 31, 2024, “global DAUq grew 37% compared to the prior year period, driven by 45% growth in DAUq in the United States and 30% growth in DAUq in the rest of world” according to the latest 10-K.

Of course, growing users is only a portion of the equation – they don’t mean much if you can’t monetize them. On this front, Reddit seems to be doing well. In the latest conference call, COO Jen Wong noted that part of the increase in revenue growth (48% increase year over year to $243 million) was due to “[c]lick volume [doubling] and we improved click-through rates by over 40% year-over-year in the quarter.”

Risks & Valuation

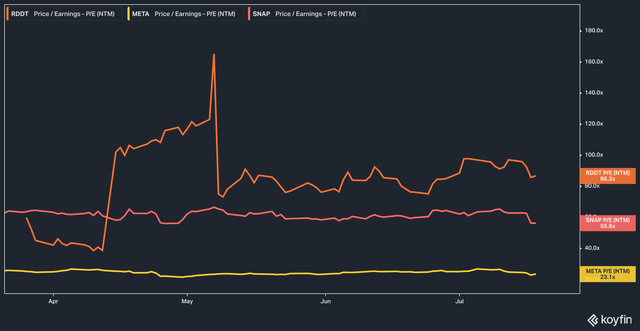

The principal risk we see at Reddit is its valuation. Today, the stock trades at a forward P/E of 86x, and a forward EV/EBITDA of 79x – figures which harken back to the heady days of ZIRP.

Reddit PE vs SNAP, META (Koyfin)

Indeed, even against its peers, Reddit is traded at a significantly inflated valuation. Snap currently trades at 55x forward earnings, while Meta – the industry juggernaut – trades for only 23x. Reddit is no flash in the pan, but we struggle to see how a valuation this far above the undisputed social media king, with all of its reach and monetized platforms, is sustainable.

Of course, investors also have to contend with the same risks inherent in any social media company. At this valuation, investors undoubtedly expect strong growth for many years to come. What if attitudes towards the platform – perhaps ignited by political pressure as Meta has periodically seen over the years – drive away users or stall growth? These are all significant factors that we believe investors should have in mind.

The Bottom Line

Reddit has a lot going for it: Management is handling the business well, a growing user base, and increased advertiser success. However, its dual-class structure, at the moment, precludes Class A shareholders from having any meaningful say in the governance of the company, and the lofty valuation alarms us, as any bump in the road could cause a reversion in valuation. For those reasons, we remain neutral on Reddit today.

Read the full article here

")

")