")

Investment Thesis

It has been a tough year for Medical Properties Trust (NYSE:MPW), since the largest tenant, Steward Health, filed for Chapter 11 bankruptcy in May. We’ve particularly had a contrarian stance on the company, given as we pointed out the financial challenges multiple of their tenants have been facing.

Today, we believe to be entering into a situation where Medical Properties Trust is in the “end game” stage as it faces a multitude of problems. These problems range from declining underlying cash flow-based fundamentals, rising cap rates and much higher funding costs, as well as much recently uncovered information about their tenants, which is why we’re updating our rating on the company from ‘Sell’ to a ‘Strong Sell’. In this article, we elaborate on the reasoning behind our valuation and why we believe there are very few opportunities left in MPW’s common stock and why chasing the current yield of 12.74% appears disproportionate to us in terms of risk-return considerations.

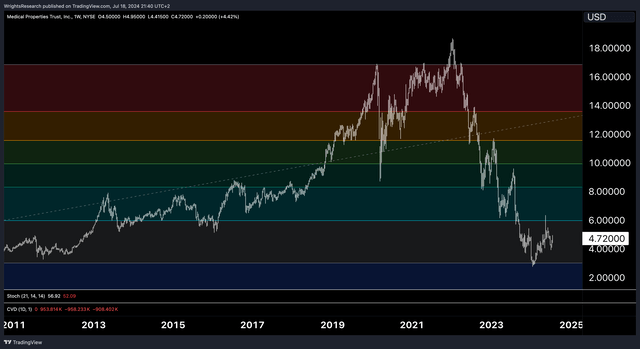

Tradingview, Wright’s Research

Where There’s Smoke, There’s Fire

In our previous findings, we’ve been very critical of some of Medical Properties Trust’s tenants, for example having pointed out Stewards Health’s financial standing which was seemingly deteriorating looking at reports from court filings. These doubts ultimately came to fruition when Steward Health filed for Chapter 11 bankruptcy in May of this year, as we anticipated.

As of last week, Steward Health has also been under criminal investigation from Federal authorities for “fraud and violations of the Foreign Corrupt Practices Act”. This news came after earlier this month, an investigation led by the Organized Crime and Corruption Reporting Project (OCCRP) revealed that Steward Health reportedly paid over $7M to intelligence firms to engage in surveillance and disinformation campaigns on critics of Steward, including journalists and analysts highlighting what we believe to be highly unethical and very questionable conduct. In Stewards latest bankruptcy proceedings files we can also see that among the latest transactions before bankruptcy (Docket 1400), over $1.5M was paid out to intelligence firm Audere International, whilst other bills for example to medical suppliers went unpaid.

And as the saying “where there’s smoke, there’s fire” goes, Steward wasn’t the only major tenant of Medical Properties Trust which we found to be arguably problematic, as we believe Prospect Medical also had certain financial woes and has seen a fraud investigation opened against them by the DOJ as well earlier this month. Pipeline Health also went through bankruptcy restructuring last year, with other tenants of Medical Properties trust also previously having shown financial challenges. We saw these problems preemptively though, having constructed unorthodox measures like Cash EBITDA which was steadily declining instead of the AFFO/NFFO which most investors were seemingly focused on and remained quite robust.

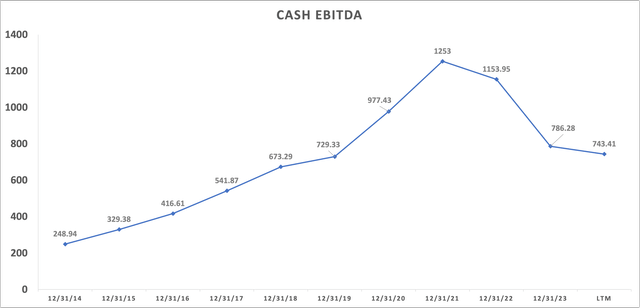

Author’s Visuals

Measures like Cash EBITDA did away with some of the complex financial engineering like investments and loans being extended to tenants which were arguably in poor financial health. Also taken into account were things like non-cash rent and what we believed to be aggressive financial accounting with straight line rent adjustments given our perception some contracts to tenants would not be feasible in the long run, and should be measured on a cashflow basis only. As you can see in the graph above, annual Cash EBITDA is defined as Cash From Operations (CFO) with interest expense and income tax expense added back.

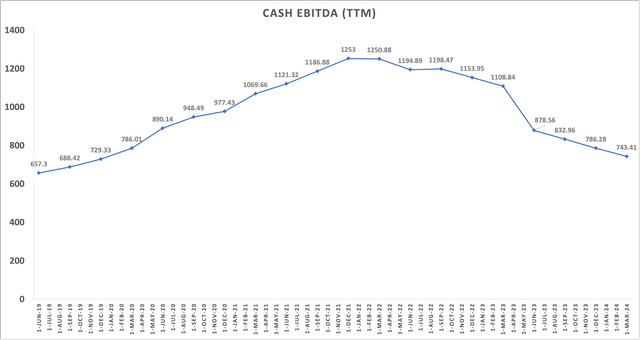

For example, over the last 12 months CFO totaled to $444.48M, with interest expense being $422.20M adding up to a total of $866.68M. Note that, instead of a tax expense over the last 12 months, Medical Properties Trust saw a tax benefit of $123.27M, which brings the total to $743.41M over the period. If we were to actually look at this metric on a rolling 12 month basis, you can see that from Q4 2021 this metric declined a staggering amount from $1253M to right now standing at merely $743.41M. This metric will become very important later in our valuation, where we also take into account MPW’s debt load and current cap rates for similar properties in the industry.

Author’s Visuals

Fair Value Accounting & Liquidation Value

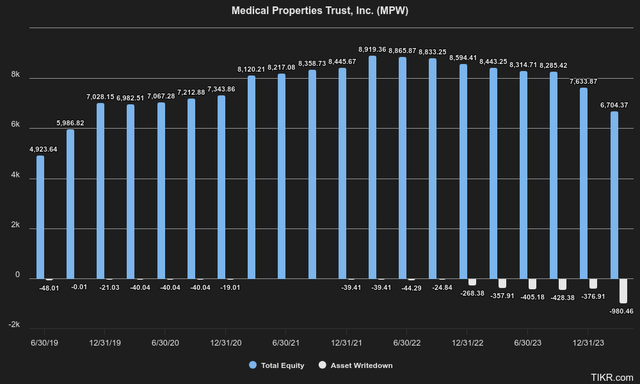

Additionally, we also want to raise the notion that there is a big discrepancy in what properties are worth according to fair value accounting compared to the liquidation value in reality, given we believe the two are often conflated by investors. In Medical Properties Trust’s case, the fact that the asset value is labeled as $11.40BN on the balance sheet, does not mean that the actual liquidation value resembles the same amount, given you only know what a property is worth once it hits the market and gets sold.

Thus, also the belief that because MPW’s equity is currently marked at $6.70BN on the balance sheet, that it also should trade at a $6.70BN market cap, we believe to be arguably a fallacy. This is especially the case when there are questions about the quality of MPW’s assets and changes in market conditions like rapidly rising cap rates. It also does not account for other adverse market conditions like the fire sale of assets, which we believe to be applicable to MPW. In previous articles we alluded to the fact that writedowns could be coming, which we right now are already starting to observe with over the last 12 months over $980M of asset writedowns already being done. Shareholder’s equity is being compressed, and we believe this trend to continue into the future as the company has to either raise capital at exorbitant rates or sell off assets off which we believe the liquidation value to be lower than it is currently marked at on the balance sheet.

TIKR Terminal

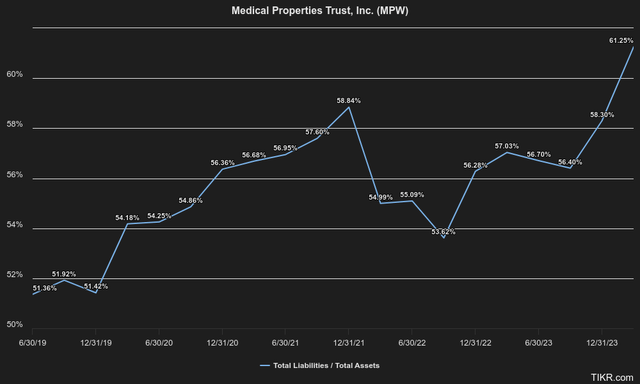

Another contentious topic that’s not often seen is the effects these writedowns have on MPW’s leverage ratios. As you can see on the chart below, the total leverage ratio or total liabilities over total assets has been steadily rising since 2022 and hit a record high of 61.25% as of the last earnings release. Likewise, we see this ratio also headed north if writedowns keep coming, and asset values keep contracting while MPW’s debt liabilities stay constant.

TIKR Terminal

This elevated leverage ratio may lead to a number of adverse outcomes, such as a lower credit rating and higher financing costs, given MPW could be seen as a much riskier borrower. Plus the most substantial risk of all, which is the potential inability to refinance current debt at all, and subsequently insolvency issues. In which case, you always have to remember that common shareholders are paid last, with bondholders being higher up in the capital stack in terms of priority.

All Eyes On Refinancing

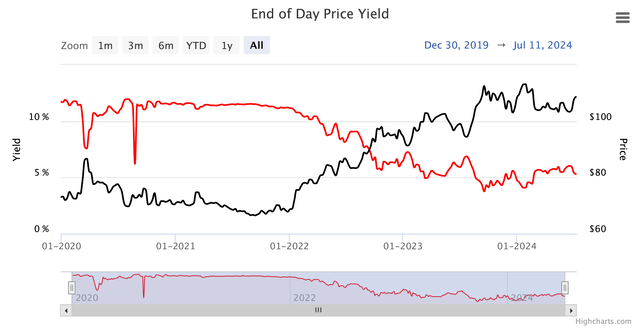

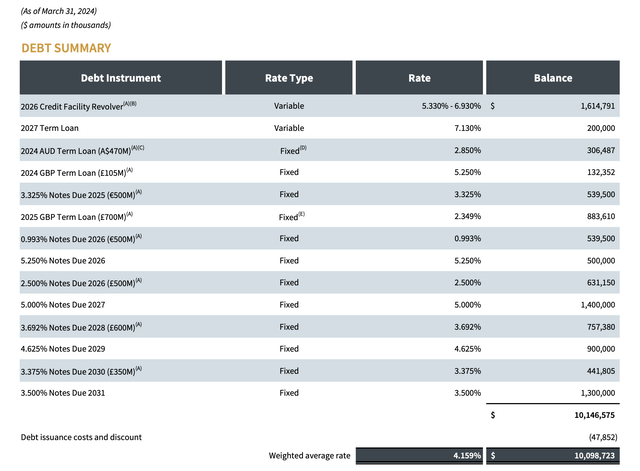

Speaking of refinancing, we believe a lot has changed and believe MPW will soon find itself in a tough position given Cash EBITDA metrics have declined substantially and cap rates have risen substantially. The main issue we still see is the fact that the current weighted average of financing for MPW lies at 4.16%, whilst outstanding bonds are trading north of 12%.

Looking for example at outstanding bonds maturing in October 2027, the yield went from a staggering 1.7% in September 2021 to now being priced at 11.69%. The yield on these Single-B loans as rated per Standard & Poor’s is also a lot higher than the weighted average index for other Single-B bonds at 7.03%. And even though Circle Health was recently able to secure financing at a relatively attractive rate of 6.9% compared to the bond yields we’re seeing of outstanding debt, we do note that this excludes debt issuance costs/ fees and is likely not be representative of the whole portfolio.

FINRA

In any case, we definitely don’t see the attractiveness of buying the common equity, chasing for yield, in this case given the underlying bonds are virtually trading at the same yield, and we’re not expecting share appreciation as will lay out in valuation. We likewise wouldn’t be surprised if bondholders themselves are also expecting a haircut, given the yield bonds are trading at. As it currently stands, MPW still has a wall of maturities it has to face over the next couple of years, despite short-term funding for 2024 being more or less secured with the recent liquidity that was raised. For example, it is expected that $800M worth of proceeds from Circle will be used to pay down the 2025 revolver in GBP and the upcoming 2024 GBP term loan. Nevertheless, we still see MPW facing a problem, running out of liquidity beginning 2025 with the easiest financing options already being swept off the table, likely triggering a surge in funding costs or more writedowns in our view if assets get sold.

Medical Properties Trust IR

And looking at Cap Rates from the CBRE, are currently at 7.0% for the broad commercial real estate market, with medical outpatient building (MOB) facilities also around a 6.9% cap rate.

CBRE

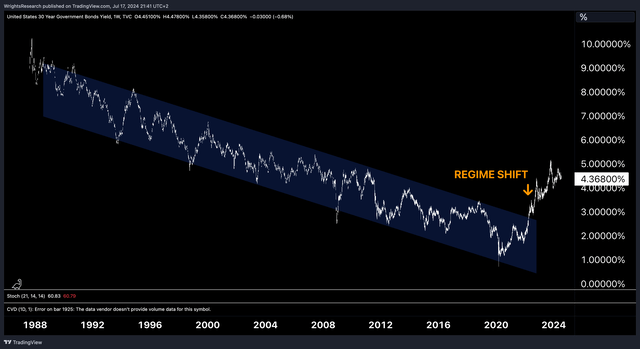

On a long-term basis, we expect Cap Rates to continue to rise, given we see a regime change after the 40-year-long bond bull market came to an end in early 2022. We don’t see many prospects to returning to ZIRP given the inflationary environment alongside with an environment consisting of rather fiscal dominance by the US government. Either way, we believe it’s fair to say that MPW’s current 4.16% financing costs for debt will be repriced a lot higher over the next couple of years.

Tradingview, Wright’s Research

Valuation

There are also quite a few big differences from our previous valuation, after a combination of Cash EBITDA contracting and Cap Rates rising slightly. Last year, we preemptively warned about the financial distress some tenants were under, and proposed what the dangers would be if rent would be cut. At that point, Cash EBITDA still amounted to $1,154M and didn’t seem sustainable over the long run to us.

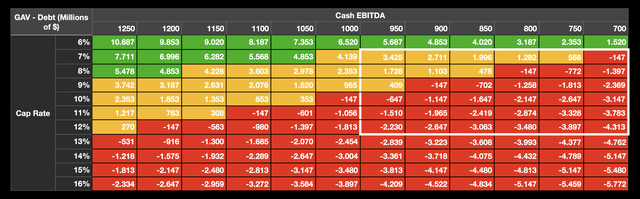

Now at $743.41M Cash EBITDA and average Cap Rates of 7%, would leave us with a Gross Asset Value of $10.62BN. Subtracting this with $10.15BN worth of debt however leaves common shareholders only with a perceived $473.57M worth of equity, which is still far less than the $2.83BN market cap MPW is traded at today. On the other hand, we see a 7% cap rate also being quite generous, especially with the Steward bankruptcy that’s moving quite slow and a DOJ investigation hanging over its head.

Author’s Valuation Model

Some may also hope for an improvement in this Cash EBITDA metric, but we’re rather critical of MPW’s future prospects given questionable actions taken in the past. This includes but is not limited to the continuation of using straight line rent accounting while we saw tenants were visibly already in distress, potentially misaligned compensation plans which stimulated transaction volume instead of asset quality, lending to their own tenants, and financial woes among tenants not only being limited to Steward Health.

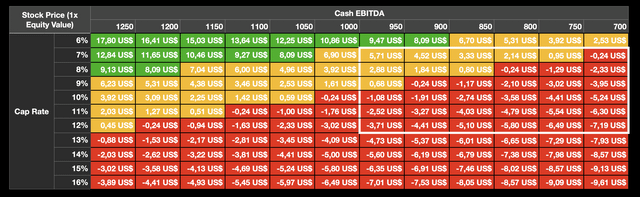

Especially, the questionable practice of lending to own tenants made it difficult for us to determine the actual underlying cash profitability of tenants, making MPW essentially a cash flow exercise. This is also the reason why we regard Cash EBITDA over the trailing 12 months (TTM) as the single most important metric. In any sense, there is very room for error in our valuation before the equity becomes potentially worthless. At the previously mentioned 8% Cap Rate, which is not unwarranted given the 11-12% outstanding underlying corporate bond yields, and $750M in Cash EBITDA, it seems to us like there could even be no equity left at all anymore for shareholders.

Author’s Valuation Model

Above, you can see what this would mean in terms of share prices when we divide the equity by 600.3M diluted shares outstanding. In our previously mentioned example, with the current TTM Cash EBITDA of $743.41M and a 7% Cap Rate, would mean fair value estimated at $0.79 per share. Also, if we are right in this method of valuation, we estimate the loan to value (LTV) ratio of MPW to be closer to 95%, which would be a lot higher than the currently perceived ratio of 55-60%. In commercial real estate, a ratio of 56-80% if acceptable, with a ratio of higher than 80% virtually deemed risky for lenders when extending financing.

The Bottom Line

With continuing refinancing pressures and tenant issues at MPW, we believe that the company may have entered the “end game”. With the current outlook, we quite don’t see the value in the common stock, as well as a lack of any room of safety at all.

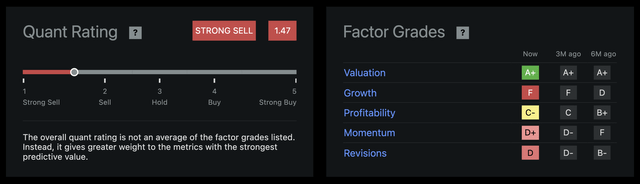

Furthermore, we think the risk-reward of buying common shares rather than the underlying debt is particularly unappealing, given that we do not see a path to recovery for MPW’s share price and the fact that both the debt and the equity offer virtually the same yield. We’re also downgrading MPW to a “Strong Sell”, as underlying fundamentals previously outlined seem to be in further decline. Seeking Alpha’s Quant Rating currently holds MPW in between a “Sell” and a “Strong Sell”, which we agree with.

Seeking Alpha

Read the full article here

")