")

")

")

Infrastructure and utilities have been one of the most hotly contested topics of conversation over the past several years. The aging infrastructure of the United States has continuously struggled to meet the current power demands causing consequences such as power outages during the Summer season.

Several years ago, this spurred President Biden to announce his Build Back Better framework which included over $1 trillion in spending initiatives around infrastructure including electricity generation and delivery. This new and ongoing investment has been critical for maintaining the United States’s ability to provide resources such as electricity and gas for the population.

However, more recently, other emerging technologies stand to play a more significant role in forward power demand. Currently, the United States is woefully unprepared for the coming generational wave in electricity demand. Facing an oncoming freight train, the Utility sector has a difficult task lying ahead.

Today, we dive into one of the highest performing, actively managed utility funds from Cohen & Steers (CNS). CNS manages a lineup of closed end funds focusing primarily on real estate and infrastructure. The Cohen & Steers Infrastructure Fund (NYSE:UTF) offers investors a monthly dividend with an opportunity for net asset value appreciation. The fund has also outperformed its underlying index over most time horizons.

Portfolio

UTF’s portfolio is built on strong operators in the utilities, infrastructure, and real estate industries. Holdings are widely diversified across industries and geography, including electricity, gas, telecommunications, and water. Services rendered by utility providers and the holdings of UTF are essential businesses which provide the building blocks for life and the economy. An investment in infrastructure is an investment that goes into just about everything that keeps your lights on and your belly full.

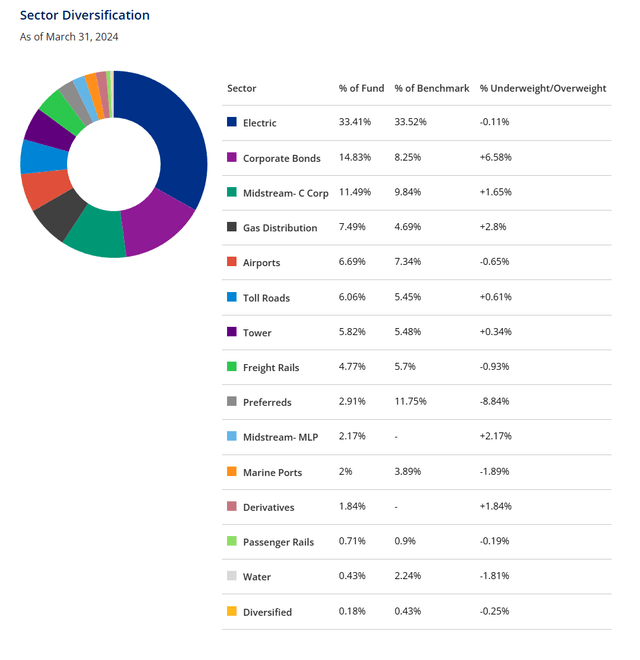

UTF Fact Sheet

Sectors are spread across industries with Electric (33.4%), Midstream (11.5%), and Gas Distribution (7.5%) leading the largest individual sectors. Over the past several years, gas and master limited partnerships have seen unpredicted tailwinds which pushed sector performance. Funds like UTF have capitalized on the opportunity and their allocations have since grown.

Interestingly, CNS has added bond positions to many of their closed end funds as interest rates rose. As the ten year treasury increased over the past three years, corporate yields have risen similarly. Maintaining their historical interest rate spreads, some bonds now offer a meaningful opportunity to contribute to UTF’s portfolio compared to the zero interest rate policy era.

The fund is spread across the globe with most geographies represented. For example, domestic investments account for only 58.8% of the fund’s assets. Canada is the second largest geography at 9.5%, followed by Australia at 5.7%. UTF is a more globally diversified fund than most other funds in the CNS lineup.

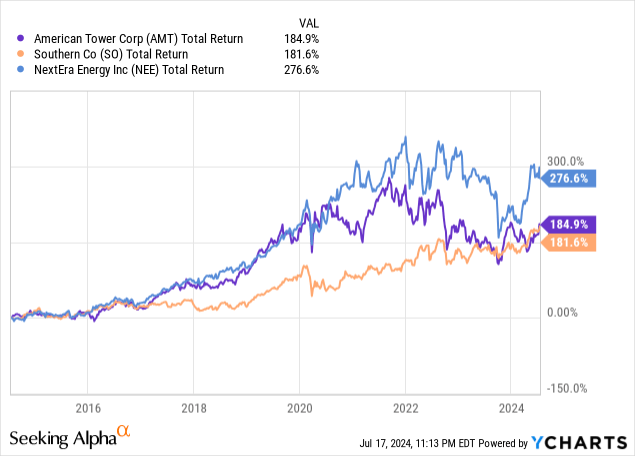

The largest holdings in UTF’s portfolio are the largest names in the utility industry. The top three holdings are American Tower Corporation (AMT), Southern Company (SO) and NextEra Energy (NEE), representing 4.0%, 3.7%, 3.5%, respectively. Each of these companies is a key player in the infrastructure segment.

AMT is one of the largest owners and developers of cell towers around the globe. The company has an enormous global footprint of telecommunications assets and is the largest REIT by market capitalization. However, the company is different from a typical real estate business, providing infrastructure for cell phones around the world. AMT has experienced enormous growth over the past decade as the company leads the way providing communications capabilities to emerging geographies.

SO provides resources for the transmission and distribution of electricity. SO builds, owns, and manages power generation facilities, including renewable energy projects. SO manages a variety of resources including nuclear, coal, hydroelectric, solar, and wind. SO has nearly nine million customers nationally and works with larger commercial and government clients.

NEE sells electricity generated from wind, solar, and other clean energy sources. NEE is a pioneer in the clean energy market leading the way in a variety of clean energy solutions like battery storage and modern electrical transmission projects. With over 30 gigawatts of generation capacity, NEE has become one of the largest and most modern energy providers in the industry.

The remainder of UTF’s portfolio is allocated to similarly impressive businesses who are innovating.

Leverage & Valuation

As with most funds from CNS, UTF is leveraged. Like many closed end funds, UTF borrows to reinvest the proceeds juicing long term returns at the expense of added volatility and risk. The fund’s current leverage ratio is 30.3%, which is aligned with historical leverage rates.

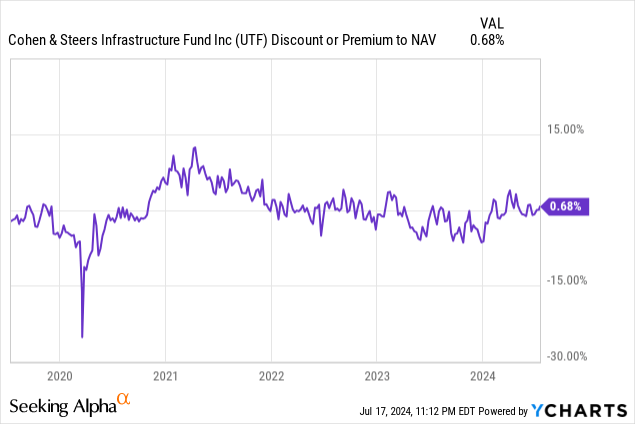

Additionally, UTF is currently trading in line with net asset value or NAV. During the low interest rate era, UTF traded at a meaningful premium to net asset value as investors sought high yielding assets. However as rates have broadly increased, funds like UTF have lost a degree of their luster. Over the past two years, UTF has traded at an occasional discount to net asset value. Year to date, pricing has realigned with NAV.

Another contributing factor to the realignment has been broad sentiment that interest rates will come down. Utilities as a sector and closed end funds as an asset are both exposed to interest rate risk. With the Federal Reserve hinting that rates will decline sooner rather than later, UTF and similar funds have broadly seen improved pricing.

At a current premium of less than 100 basis points, UTF is fairly priced.

Dividend

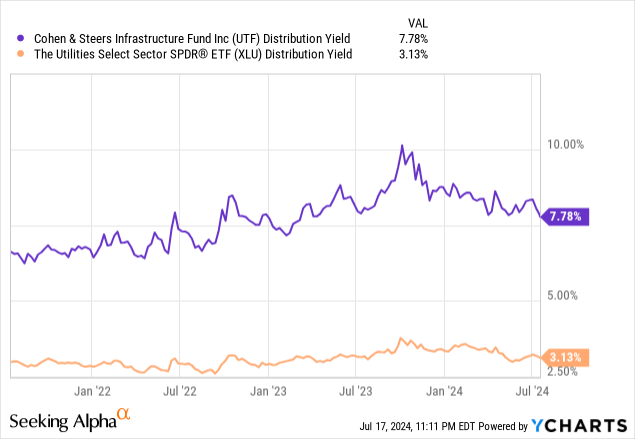

UTF distributes a level monthly dividend like most closed end funds. Based on current share price and a monthly distribution of $0.155 per share, UTF yields just under 8%. The current monthly distribution has been maintained since 2018, when it increased from $0.134 per share. Notably, CNS manages their funds such that there is typically no special dividend. Some fund managers opt for a conservative monthly dividend supplemented by a larger year end payout as required.

In 2016 and 2017, UTF sent special dividends of $0.432 and $0.16, respectively. As a result, CNS increased the regular distribution and it has remained there since. UTF’s monthly distribution is attractive for those seeking income as it presents a meaningful yield premium against the Utilities Select Sector SPDR ETF (XLU) which currently pays 3.13% worth of quarterly dividends.

Bear in mind that UTF sources the distributions from dividends and capital gains within the portfolio. Appreciating positions are responsible for covering a portion of the annual distribution which accounts for the spread between the dividends of the underlying positions and the fund’s annualized yield.

Performance

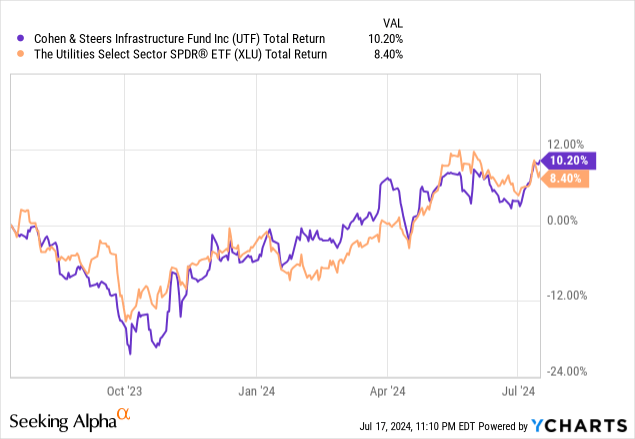

UTF is performing well because of speculation that interest rates could decline and tailwinds in the sector. Year to date, the fund has returned 17.1% as the sector rallies.

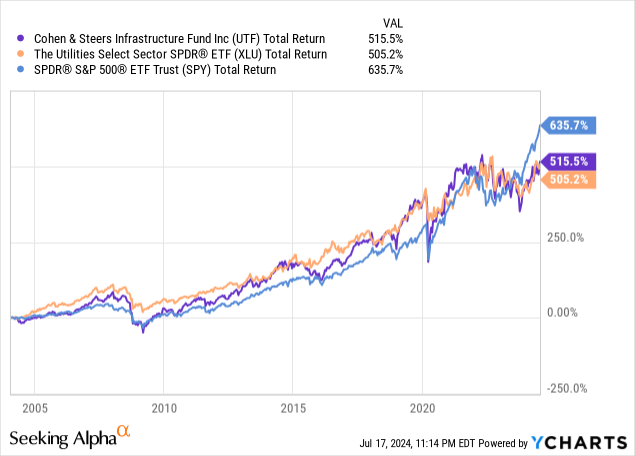

CNS has been an exceptional manager of closed end funds. Their lineup of real estate and infrastructure funds have outperformed their benchmark handily over long and short time frames. UTF is no exception to this, outperforming XLU.

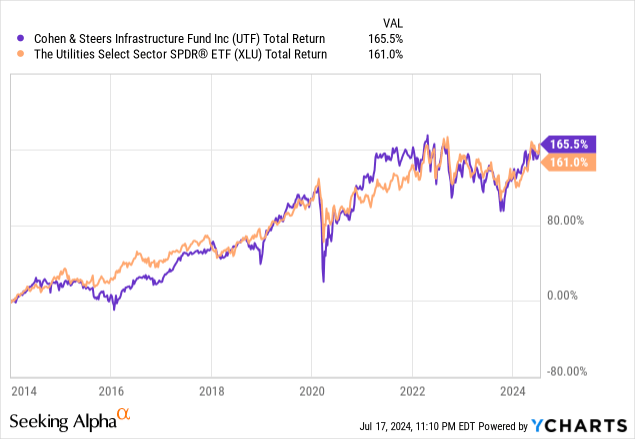

Over the past twelve months, UTF has outperformed the benchmark by 1.8%, partially due to improvements to the fund’s valuation. Since 2014, the fund has also outperformed the passively managed benchmark by around 5% on a total return basis.

However, as investors know well, past performance is no indicator of future returns. One critical piece of the puzzle for UTF and similar funds will be the outlook of utilities. Infrastructure spending is poised to accelerate at an unprecedented pace over the next five years. Let’s explore in greater detail.

Resource Demand

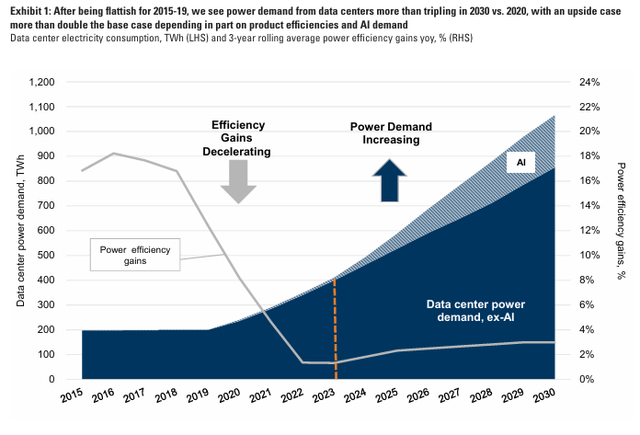

Artificial intelligence is driving unprecedented demand for electricity. Market participants in a position to deliver can capitalize on a generational gold rush. Demand for electricity is beginning to accelerate due to a variety of factors. However, in addition to rising forward demand, AI is causing a deceleration in energy efficiency. As a result, forward projections around electricity usage are deviating from historical trends. The primary culprit behind this new trajectory is power hungry data centers.

Goldman Sachs

Global data center power demand is forecasted to double over the next five years. This extraordinary expansion comes after stagnant demand for the past ten years. Despite increased connectivity, the demand for electricity has been offset by efficiency changes. This calculus has changed dramatically.

Most of this increased demand stems from the prolific adoption of generative AI and similar GPU-based technologies. Although similar to a Google query, the software behind ChatGPT and similar programs requires significantly more power. According to research from EPRI, a traditional search on Google uses 0.3 watt-hours of electricity. A search using ChatGPT requires 2.9 watt-hours. That’s nearly ten times the energy!

So, who is expected to meet this extraordinary wave of demand for electricity? The answer is utility providers, such as those owned by UTF. Companies like SO and NEE will be critical in meeting the upcoming demand for power. Power companies that work with data centers or sell electricity on a wholesale basis must prepare.

According to a recent article from Reuters, some utility providers are projecting sales growth several times higher than historical growth rates or their outdated projections. According to their research, data centers accounted for the top growth center for nine of ten utility providers. Research from Goldman Sachs (GS) estimates that data center power demand will grow by 15% annually through 2030. If these projections pan out, data centers will comprise 8% of aggregate power demand in the United States. This is up from current usage rates of less than 2%.

As one of the largest components of forward demand, data center demand is poised to increase the net growth rate of electricity usage to 2.4% per year. This means utility providers have a significant gap to fill. Research suggests that up to 50 GW of additional incremental power generation capacity will be required to meet forward demand. This extraordinary demand gap leaves significant room for large providers to expand into new geographies or deepen their existing investments. GS estimates that this could amount to at least $50 billion of spending on new power and infrastructure assets nationally in the coming years.

Conclusion

UTF is one of the best utilities-specific closed end funds. The fund offers a high dividend yield in the form of monthly distributions of dividends and capital gains. UTF is currently trading in line with NAV following improvements to the fund’s valuation. As tailwinds behind electricity demand begin to mount, UTF’s portfolio stands to benefit, earning the fund a “Buy”. Generational power demand is likely to continue powering the fund’s strong near term performance. Over longer time periods, the manager adds meaningful value to the fund resulting in outperformance relative to the underlying index.

Read the full article here

")

")