Q2 2025 Earnings Call Transcript")

")

Introduction

I like oil royalty companies, as they receive a cut of the top-line revenue from the operators of the wells that are on the royalty land. This greatly reduces the risk for the royalty company, considering it doesn’t have to deal with and has no exposure to the profitability of the operator. The only downside is if that operator reduces its investments in an oil (and gas) field, resulting in a lower attributable production. But in an environment where $80 WTI is an acceptable oil price, the odds of that happening are pretty low. The downside of owning a royalty company is that the torque on the underlying commodity price is lower.

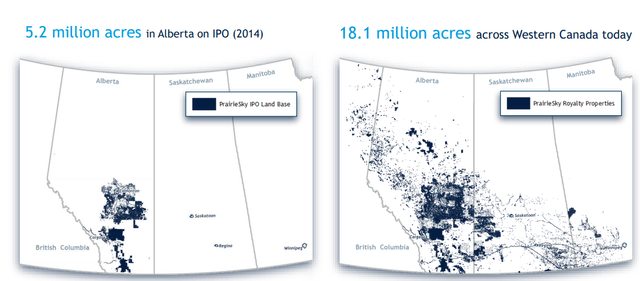

I have been following PrairieSky Royalty (TSX:PSK:CA) (OTCPK:PREKF) for several years now, and although I always found the company to be pretty expensive, it is a very well-managed oil and gas royalty player with an extensive land position in Canada totalling almost 20 million acres. The company recently published its Q2 results, so I wanted to see if I need to fine-tune my expectations and if the company is now priced at a more attractive level. You can read all my older articles on PrairieSky Royalty here.

Discussing the just-released Q2 results

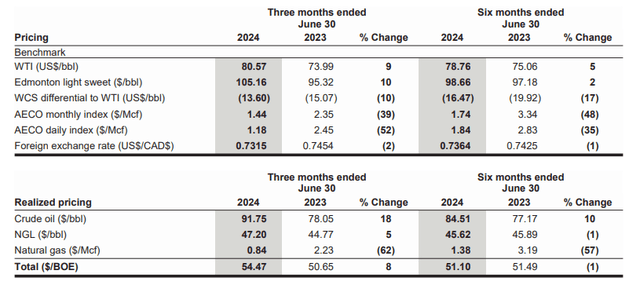

Looking at the Q2 results, we see a slightly smaller production compared to the first quarter of the year. As you can see below, PrairieSky reported a total attributable production of 25,320 boe/day, which is lower than the almost 26,000 boe/day it reported in the first quarter of the year. The majority of the production consists of oil, which makes up about 52.5% of the oil-equivalent output. The natural gas production also plays an important role, as it represents about 42% of the oil-equivalent output in the second quarter of this year.

PSK Investor Relations

That’s a pity as the natural gas price was exceptionally weak. The company reported an average realized price of just C$0.84 per Mcf which is a 62% decrease compared to the average price of C$2.23 per Mcf in the second quarter of last year.

PSK Investor Relations

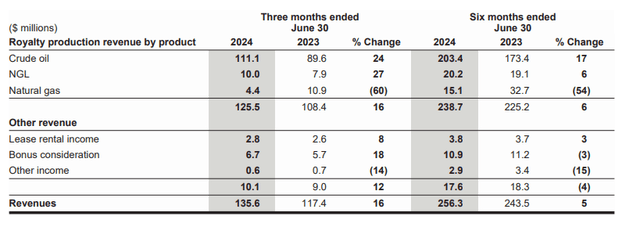

Fortunately, the oil price mitigated the very weak natural gas price. As the image above shows, the average realized price per barrel of oil-equivalent increased by just over 7% thanks to the 18% oil price increase. Looking at the revenue per commodity (shown below), the C$6.5M revenue decrease from natural gas sales is more than compensated by the oil revenue, which increased by in excess of C$20M.

PSK Investor Relations

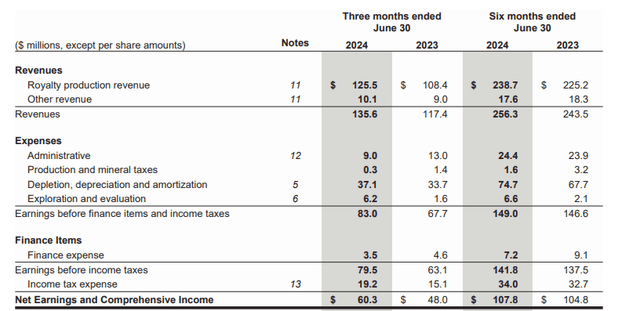

The combination of a higher oil price, higher oil production and the lower natural gas price still resulted in a 16% revenue increase, which came in at C$125.5M. The total reported revenue was C$135.6M, an increase of 16% as well.

The total operating expenses remain pretty low and the depletion expenses still represent the majority of the operating expenses. This resulted in the company announcing a C$83M EBIT, which is a nice increase from the C$67.7M in the second quarter of last year.

PSK Investor Relations

Additionally, as PrairieSky has been reducing its gross debt level, the total interest expenses decreased as well and this allowed the company to post a net profit of C$60.3M, which is approximately C$0.25 per share. That’s about a quarter more than in Q1 2024 and Q2 2023.

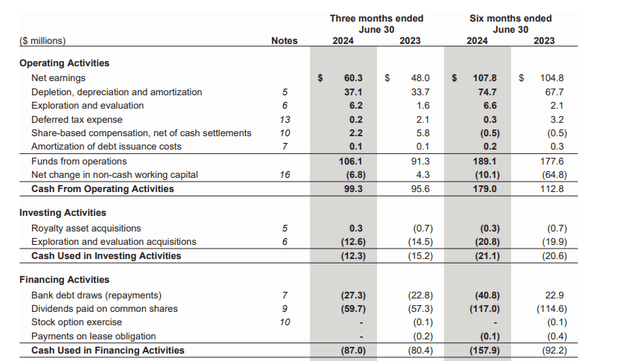

Of course, I’m also always interested in the company’s operating cash flow and free cash flow. The reported operating cash flow was C$106.1M, which represents C$0.44 per share. And as you can see below, PrairieSky spent about C$12.6M on exploration and evaluation on a capitalized basis (it also expensed C$6.2M in exploration and evaluation expenses).

PSK Investor Relations

This means the underlying free cash flow result was C$93.5M, for a net free cash flow result of C$0.39 per share. Keep in mind this includes almost C$19M or almost C$0.08 per share.

While the second quarter was dealing with an exceptionally low natural gas price and a high average oil price, the H1 results provide an interesting look under the hood using prices that are generally seen as acceptable long-term prices (although the expectations for the natural gas price are higher than the average realized price in H1 2024). Using an average realized oil price of C$85 per barrel and C$1.40 for natural gas (I think it’s okay to use C$2.75-3.00 as the average long-term price which would have added an additional C$15M in revenue in the first semester), the operating cash flow was C$189.1M while the free cash flow was C$168M or C$0.70 per share. Using C$3 natural gas would have had a positive impact of approximately C$0.05 per share). Note that C$168M in free cash flow includes approximately C$28M in capital expenditures (C$7M expensed, C$21M in ‘real’ capital expenditures that are being capitalized). At C$3 natural gas and C$84 oil, the FFO excluding the expensed exploration and evaluation expenses would be approximately C$0.85 per share, or C$1.70 per share on an annualized basis.

Thanks to the company’s strong cash flow result and relatively low dividend (C$0.25 per share per quarter), the net debt decreased fast.

PSK Investor Relations

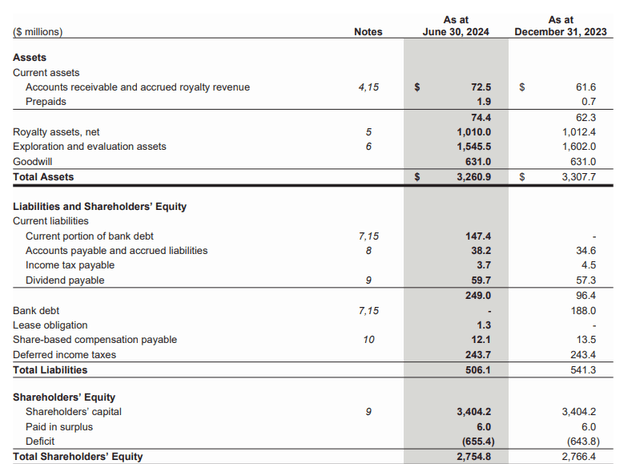

As shown in the image above, PrairieSky ended 2023 with a total net debt of C$188M, but this was already reduced to C$147M by the end of June. I am not worried that the bank debt moved from the long-term liabilities to the current liabilities, as the maturity date of the credit facility is in February 2025.

PSK Investor Relations

And given the strong cash flows and substantial asset base with almost 20 million acres of royalty-bearing land, I have zero doubt the credit facility will be extended.

Investment thesis

I still have no long position in PrairieSky Royalty, but I continue to be impressed with how well the company is run. That being said, I’m still not prepared to pay the 16.5 times the FFO (using the annualized result based on the H1 FFO excluding the exploration and evaluation expenses).

This means I am still a ‘hold’ on the stock, but I sincerely hope it eventually gets cheap enough for me to buy it. But for that to happen, I’d like to see a low double-digit multiple to the FFO.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q2 2025 Earnings Call Transcript")

")