")

")

")

BigBear.ai Holdings, Inc. (NYSE:BBAI) is a stock we have previously traded. It has been a trader’s stock, but investors have been on a roller coaster ride. We timed this one well, as back in December 2023, we had offered up a speculative buy for BBAI that we considered a high-risk, high-reward play that stemmed from our service’s work in our high-risk, high-reward trading sub-room that features a speculative idea once a month. That played out nicely.

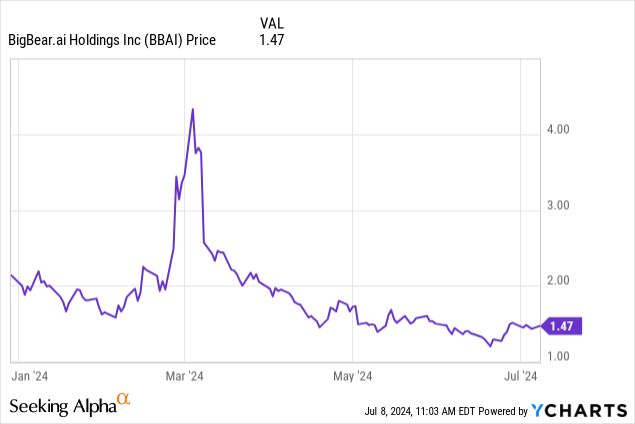

Back in March, however, we publicly commented that we thought that BigBear was going to head into ‘hibernation’ mode and downgraded the stock. Since then, shares have moved slowly downward/sideways.

What concerns us here is that despite AI-related names running nicely, along with the ten-year yields simmering down, BBAI stock has not really moved. We suspect that the next catalysts will be updates on earnings expectations and news on any future contracts/customers. But for now, we expect more sideways action. Let us discuss.

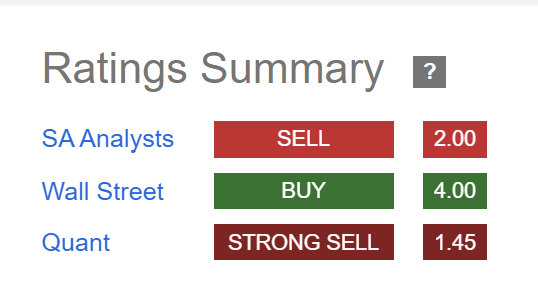

We continued to keep the stock at a hold here. Make no mistake, there are plenty of bets being placed against this stock. About 17% of the float is sold short. This is concerning, as the AI momentum has remained strong, but BBAI stock has not participated in the last few months. As we said in our article from March, “we think it retraces.” We continue to think that the stock will be range-bound, but any positive unexpected news could spark a tradable short covering rally. Long-term, this is an interesting story, but it remains extremely speculative. For the record, the Seeking Alpha Quant Rating and Seeking Alpha Analyst Rating are a strong sell, and a sell, respectively, for BBAI. But the Wall Street Analyst’s Rating is still a buy.

Seeking Alpha BBAI Ratings

The company’s product offerings are designed to translate data into information, which as we know, information is a powerful currency in today’s society. However, there are many competitors in this space to overcome. The company loses money as it tries to ramp up revenues. While BigBear’s offerings help customers make complex decisions, and improve efficiency, one has to question what type of moat if any exists here. That said, the company does boast customers that include the U.S. intelligence community, as well as other branches of the U.S. Federal Government. The company has also grown with the acquisition of Pangiam Intermediate to add facial recognition and advanced biometrics to the company’s computer vision capabilities and help BigBear open up the visual AI industry. However, revenues have been falling.

So while the company continues to work to grow its customer base, we need to be aware that the balance sheet here carries a lot of debt and saw revenues drop year-over-year. In the recently reported quarter, revenue was down 21.6% from a year ago. It came in at $33.1 million and missed consensus by a wide $10.6 million.

There was hope building here just a few quarters ago, when back in Q3, BigBear swung to its first net income positive quarter since going public. However, now, it appears to be a one-off. Back in Q4, the company lost money, but did deliver its second straight quarter of positive EBITDA. In Q1, however, adjusted EBITDA swung back to a loss, though it was a much narrower loss than a year ago.

We want to address why revenues were down so much. A decline was expected, but it was indeed wider than anticipated. We knew about a wind-down of the Air Force EPASS program in mid-2023 which was good for about $6.8 million in comps and, of course, from last year’s revenue from Virgin Orbit of about $1.5 million as they filed for bankruptcy. One point stood out in the release, however. Management noted the company “experienced delays in contract awards due to continuing resolutions.” So this may mean revenue gets pushed forward later in the year, and despite the revenue miss, management did reiterate its annual revenue guide, a small positive here.

Now, despite efforts to control costs, we saw gross margins narrow. This is not going to give the Street any reason to cover shorts or bid up the stock. Gross margin narrowed to just 21.1%, down to 24.2% a year ago, and a far cry from the 30% range hit in late 2023. So, a chunk of this was driven by an increase in stock-based compensation (“SBC”) expense of $1.8 million, along with the loss of revenues aforementioned.

We had previously noted that recurring SG&A is on the decline, down to $12.3 million in Q4. Here in Q1, recurring SG&A was down from a year ago, but increased sequentially. A year ago, it was $15.3 million, but fell compared to that figure to $13.6 million, a net improvement of $1.7 million. However, the increase from Q4 is notable. Adjusted EBITDA swung back to a loss of $1.8 million. Net loss of $125.1 million surged from a year ago thanks to a goodwill charge, acquisition costs, and lower margins, though there were some warrant issuances that partially offset this.

Here is the main concern. We have pressure on sales, and the company continues to lose money. But this is also a very debt-heavy company. The balance sheet is quite levered. Folks, there is $195 million of long-term debt and $0.86 million of short-term debt. There are also lease liabilities of $11.3 million. So, when considering this debt and the recent EBITDA results, you can see the significant leverage.

It is important to note also that there have been potentially dilutive moves made to raise cash. After recent warrants, the company has $81.4 million in cash on hand, along with a $296 million backlog. For now, the company has the cash to operate for several quarters. We do believe the acquisition of Pangiam will fuel growth, but the upside from here may be limited by the added dilution and the leverage on the balance sheet.

The good news here is, despite a tough quarter, revenue was reiterated to be between $195 million and $215 million. As we move forward, there remain risks. If management does not execute, BigBear might not be able to acquire new contracts. New contracts are not guaranteed. There has been some momentum in new contracts, but future commitments are critical to keep the train running here. There are tons of competitors here, all vying for limited contract dollars.

BigBear.ai Holdings, Inc. is burning cash, and the stock action has been weak during a time that has been good for AI-related stocks. Given the leverage and debt here, the price action, one would think, would benefit from lower yields.

We continue to expect sideways action here from BigBear.ai Holdings, Inc. To spark short covering, we will need to see positive catalysts and developments. The stock remains speculative otherwise.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")