")

")

")

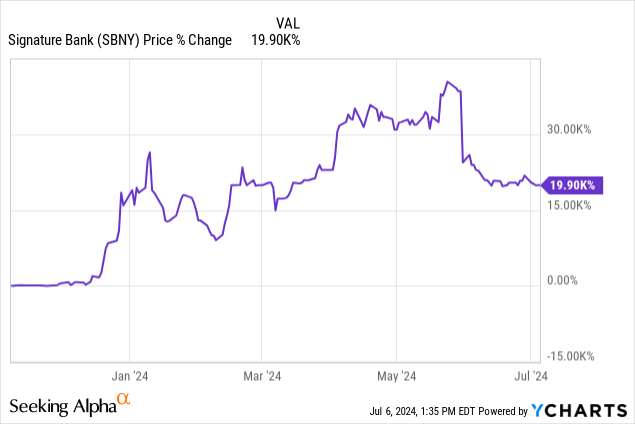

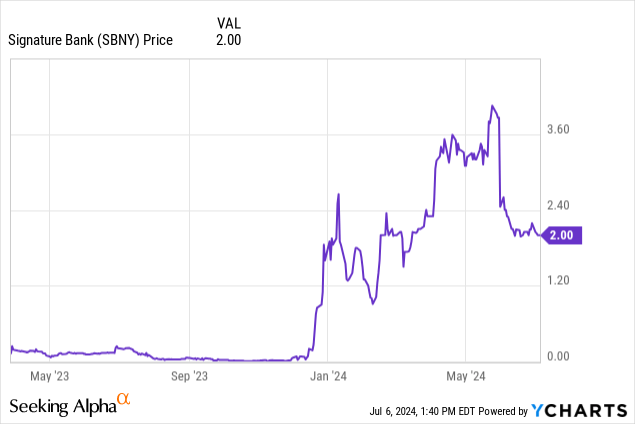

Assets of Signature Bank Corp. (OTC:SBNY) are being liquidated in a receivership by the FDIC, and because some are estimating these assets are actually worth more than originally expected the stock price has soared about 19,900% since early November. After a number of positive developments and FDIC balance sheet filings late last year, SBNY stock received new attention by speculators. There are, however, some regulations investors might be ignoring.

Receivership vs Bankruptcy

First, Signature Bank Corp. is in FDIC receivership – not Ch.11 nor Ch.7 bankruptcy. If Signature Bank Corp. was a holding company for Signature Bank it most likely would have followed the Ch.11 route that SVB Financial Corp (OTC:SIVBQ) is currently taking, but since Signature Bank Corp. was an actual bank, it could not file for Ch.11 and is in “receivership”. The FDIC is the receiver. A major difference between a receivership process and a bankruptcy process is transparency. During both Ch.11 and Ch. 7 there are many dockets filed with the court that give interested parties current information about the process, including monthly operating reports. Information contained in various motions and objections are also readily available. Usually there is even an official creditors committee appointed by the U.S. Trustee to monitor the bankruptcy process. The hearings are presided over by a bankruptcy judge that are open to the public. The FDIC receivership process operates with almost no transparency. There is very little information contained in the quarterly balance sheet filings. The FDIC process may, however, be a much cheaper process because there are fewer private lawyers billing at almost $2,000/hr. The receivership process follows the absolute priority waterfall process for payments from asset sales – no negotiated settlements and no “gifting” to lower priority classes under a Ch.11 plan. Shareholders are on the bottom.

Signature Bank Collapsed in March 2023

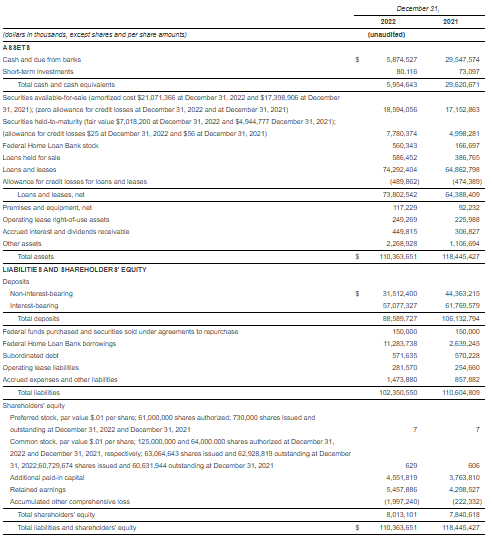

Signature Bank was closed on March 19, 2023 and the FDIC created Signature Bridge Bank. The latest Signature Bank balance sheet was for the period ending December 31, 2022.

Year-End Balance Sheet 2022 and 2021

www.businesswire.com

SBNY had extremely rapid growth that I consider to be based on very irrational banking decisions. For example, loans increased from $64.9 billion at the end of 2021 to $74.3 billion at the end of 2022, but total deposits decreased to $88.6 billion from $106.1 billion. Rising interest rates and crypto currency problems were catalysts that encouraged depositors to withdraw their money in early 2023. Immediately after Silicon Valley Bank closed there was a run on SBNY that could not be stopped. In an April 2023 report the FDIC asserted that “the root cause of SBNY’s failure was poor management”.

A subsidiary of New York Community Bancorp (NYCB) purchased certain SBNY assets and assumed certain liabilities. In exchange, NYCB issued the FDIC 39,032,006 NYCB shares under “an equity appreciation instrument”. In addition, NYCB “may be required to make a payment to the FDIC or the FDIC may be required to make a payment to NYCB ... one year after March 20, 2023, or as agreed upon by the FDIC and NYCB”. However, if there were any additional payments that would already be reflected on March 31, 2024 FDIC receivership balance sheet. (See further below.)

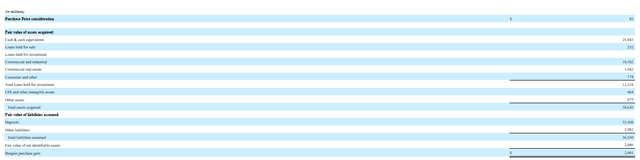

NYCB actually estimated in their 1Q 2023 filing that they would have a “bargain purchase gain on the Signature transaction” of $2.001 billion. NYCB valued the “purchase price consideration” to be $85 million. The assets purchased included $25.043 billion cash/cash equivalents, $12.45 billion total loans (including $232 million loans held for sale), and other assets for a total of $38.636 billion. Liabilities assumed totaled $36.55 billion, including deposits of $33.568 billion. The remaining SBNY items were held in the FDIC receivership account.

Fair Value of Consideration Paid, Assets Acquired, and Liabilities Assumed (March 20, 2023)

sec.gov

A June 2024 filing by NYCB lowered the value of the assets acquired to $37.8 billion. The details of that update, however, are beyond the scope of this article.

FHLB Advances/Repos Have Already Been Paid

Before going any further I want to clarify some information that seems to be confusing some investors. The FHLB advances/repos have already been fully paid and are, therefore, no longer an unpaid liability. While I don’t have the exact amount that was paid, there were approximately $11.3 billion on the December 31, 2022 SBNY balance sheet.

Investors Now Hope They May Actually Get a Recovery

Why were SBNY stock and notes trading at extremely low prices?

There were reports that the FDIC insurance fund would get stuck with an estimated $2.5 billion hit because total SBNY asset sales were expected to be less than total liabilities. This $2.5 billion and other priority liabilities would have to be fully paid before stockholders, who are on the bottom of the recovery list, get anything. The outlook for investors was very bleak.

What caused the stock and note prices to soar?

A combination of factors impacted the stock and note prices. First, there was a September 30, 2023 Signature Bridge Bank fund 10541 balance sheet filing with a net worth of $445 million, which surprised many investors who were expecting a negative amount. (Note: my links to this September balance sheet just take me to the latest March 31, 2024 filing. I contacted the FDIC to get the historical quarterly filings and I am still waiting for a reply. I will either edit this article or post that information in the comment section below when/if I get a reply.)

Second, there was significant interest by outside investors in multiple joint ventures. Blackstone paid $1.2 billion for a 20% equity interest in a joint venture and FDIC contributed $16.8 billion of “2,600 first mortgage loans on retail, market rate multifamily and office properties primarily located in the New York metropolitan area”. Santander Bank paid $1.1 billion for a 20% equity interest and FDIC contributed $9 billion of “loans collateralized by rent–stabilized or rent–controlled properties”. A partnership of the Community Preservation Corporation, Neighborhood Restore HDFC, and Related Fund Management received a 5% equity interest in two other new joint ventures. The Community Preservation Corp. will service the $5.8 billion Signature Bank loans held by these two joint ventures. 80% of the rental units associated with these loans are rent regulated.

In addition, some investors were encouraged that MFN Partners owns 6.0 million shares or about 9.5%. MFN Partners also owns 45% of liquidating Yellow Corp. (OTC:YELLQ) stock and has so far made a very large paper profit on that bankruptcy trade.

I Did Not Buy SBNY Securities Because of Regulations

The reason I did not buy any SBNY securities was because of rent regulations in New York City. Signature Bank was the largest lender to rent regulated apartments in New York. It is unclear what their exact exposure is because some apartment buildings with Signature mortgages may only have a few units that are still rent regulated while the other units are free market. Is it appropriate to include that entire mortgage in the rent regulated total mortgage number? That is up for debate. You also have the issue that some apartment units are rent controlled and some are rent stabilized. These complex rent regulations and the FDIC regulations for disposition of assets make estimating loan values very difficult.

To compound the New York rent regulation problem, the FDIC disposition of assets regulations associated with certain types of housing may result in getting significantly less than maximum value – a lot less, in my opinion. The FDIC Insurance Act states:

(E) DISPOSITION OF ASSETS.–In exercising any right, power, privilege, or authority as conservator or receiver in connection with any sale or disposition of assets of any insured depository institution for which the Corporation has been appointed conservator or receiver, including any sale or disposition of assets acquired by the Corporation under section 13(d)(1), the Corporation shall conduct its operations in a manner which–

(i) maximizes the net present value return from the sale or disposition of such assets;

(ii) minimizes the amount of any loss realized in the resolution of cases;

(iii) ensures adequate competition and fair and consistent treatment of offerors;

(iv) prohibits discrimination on the basis of race, sex, or ethnic groups in the solicitation and consideration of offers; and

(V) maximizes the preservation of the availability and affordability of residential real property for low- and moderate-income individuals.

There are many rent regulated apartment buildings in New York, especially in Manhattan, where the land by itself is worth a lot more than the building/land combination, but because of local regulations it is very difficult to demolish the building and build a new structure. Therefore, if a Signature Bank borrower defaults on a loan secured by a rent regulated apartment building, the FDIC can’t become involved in some new project that would demolish an apartment building that houses moderate- and low-income tenants because the FDIC is required to preserve the availability of those units. (They may not be even able to be involved in a new building project that creates more moderate- and low-income units than the demolished building.) The defaulting borrower may instead just “hand the keys” over to Signature Bank/FDIC. This could result in loan recoveries at a lower level than many SBNY investors are expecting.

There were new stabilized rent increases approved in June – 2.75% for one-year leases and 5.25% for two-year leases signed after October 1. For many landlords these increases will not cover their expected increases in expenses putting them at risk of defaulting on mortgages.

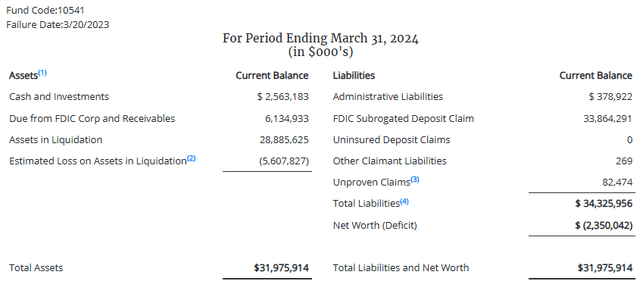

March 31, 2024 Signature Bridge Bank Report

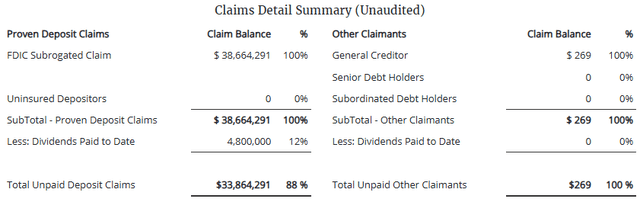

The latest March 31 balance sheet and claim details for Signature Bridge Bank are very misleading, in my opinion. First, the subordinated debt holders show “0” because technically they don’t have or need to file a claim. There was a total of $575 million subordinated debt when the FDIC became the receiver. Second, there is no mention of their $730 million 5% noncumulative preferred stock (OTC:SBNYL). (The December 31, 2022 balance sheet states the preferred shares have a par value of only $0.01, but their liquidation preference amount is $25.00 per SBNYL share.) It is unclear if the balance sheet includes the impact of the recent joint ventures because a total of $31.6 billion of loans were transferred to these joint ventures for equity interests. If they are included, how are they being reported? The receivership no longer owns those loans – it just owns equity interests in these joint ventures.

receivership.fdic.gov

receivership.fdic.gov

The net worth deficit amount of $2.35 billion was disappointing for investors because the September 2023 balance sheet had a positive $445 million number. The estimated $5.608 billion loss on $28.886 billion assets in liquidation implies a 19.4% loss. Because of the lack of transparency, it is unclear if the estimated loss factors in future interest income on loans, which could be a very significant amount because some loans do not mature for a number of years.

There are just too many unknowns associated with these FDIC receivership quarterly reports to be able to estimate rational recoveries for the various interested parties, including SBNY shareholders.

Conclusion

The problem for investors is that it could be many years before they receive any cash -if any. If loans are not sold, it could be years before they mature, especially mortgages. If borrowers go into default on a loan, it could take a long time for the litigation to be resolved. Investors need to take the present value of their estimated eventual payment using a high interest rate to reflect the high risk.

The reality is that because of various regulations the FDIC receiver has effectively turned much of the Signature Bridge Bank receivership into a de facto federally controlled moderate/low-income housing agency, which is not good for investors hoping for a recovery.

Because this FDIC receivership lacks needed transparency to make rational investment decisions, I rate all SBNY securities neutral/hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

")