")

")

")

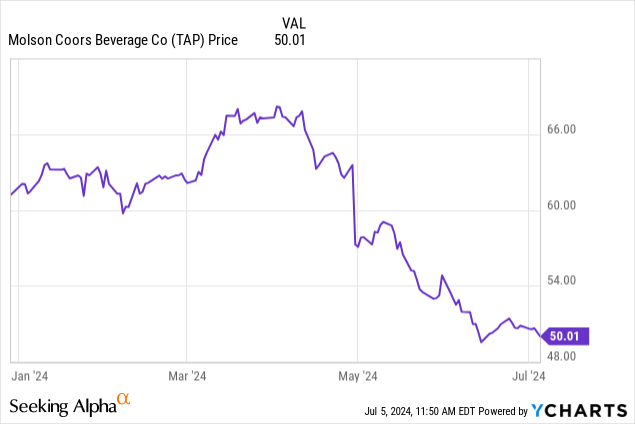

Poking around companies in the realm of 52-week lows, I came across venerable brewing company Molson Coors Beverage (NYSE: TAP). Dipping below $50 per share, the company is far away from the stable levels one generally expects of the price of such a normally stable business.

Today we’ll be looking at Molson Coors, with an eye on where it stands as a value play after dropping so much from the first of the year, along with what we can expect going forward and what the company is doing to return value to shareholders.

Understanding Molson Coors

Molson Coors has been making beer for over two centuries, and with the 2015 acquisition of SABMiller is one of the largest such brewing companies out there.

At its core, the company takes hops, water and barley, and turn it into beer. Molson Coors has a broad portfolio of brands for its brewery products, going from core brands like Coors Light and Miller Light, premium brands like Madri and Blue Moon, right down to economy brands like Miller Higher Life, Keystone and Icehouse.

That’s a big part of the company’s portfolio, but Molson Coors also produces spirits and even non-alcoholic beverages, trying to diversify into these markets even as they focus on growing the strength of their core brands.

Looking at Molson Coors Balance Sheet

|

Cash and Equivalents |

$458 million |

|

Total Current Assets |

$2.68 billion |

|

Total Assets |

$26.0 billion |

|

Total Current Liabilities |

$3.86 billion |

|

Long-Term Debt |

$5.31 billion |

|

Total Liabilities |

$12.7 billion |

|

Total Shareholder Equity |

$13.3 billion |

(source: most recent 10-Q from SEC)

Molson Coors is a big company with a lot of assets, and while they have a substantial long-term debt, they have issued bonds at very modest interest rates, and certainly supportable for a company with growing revenue streams.

The company trades at a price/book value right now in the ballpark of 0.73. That’s a reasonable discount, and quite cheap for one with so many recognizable brands that usually would command a premium.

The Risks

For a company this old, we don’t usually think of them as having an awful lot of risks to contend with. That’s not necessarily the case, however.

The company’s revenue comes from all over the world. Even though almost none of its business ever came from Russia, the company’s most recent 10-K noted that the ongoing Russia-Ukraine conflict has been a drag on sales in the overseas segment, particularly in Eastern Europe.

Doing huge amounts of brewing and delivering the product all over the world also makes the company very sensitive to the cost of fuel and electricity.

Beer consumption in some markets is closely tied to general economic conditions and it is important to think of the business as discretionary consumer spending, so that if the economy gets too bad, people will be buying less product.

The final risk we’ll be talking about is the most obvious. Humans have been making beer for thousands of years, so there’s a lot of competition on the market. Increased pushes by the competition could force Molson Coors to reduce prices to keep up, and that could ultimately hurt the gross margins.

Share Repurchase Program

Last year, Molson Coors unveiled a $2 billion stock buyback program. In 2023, they bought back $211 million in shares at an average price of $61.06. In the first quarter of this year, they bought another $111 million shares off the market, putting the average price of those in the ballpark of $63.18.

In both cases, the buybacks have been done with the stock trading below its book value. You’ll also notice that the per share price is considerable higher than it is at present (as I write this, the stock is trading below $50 per share). That means the present time would be an ideal opportunity for Molson Coors to buyback more shares at a very reasonable price.

Looking at the Earnings

|

2021 |

2022 |

2023 |

Q1 of 2024 |

|

|

Total Sales |

$12.4 billion |

$12.8 billion |

$13.9 billion |

$3.0 billion |

|

Gross Profit |

$4.0 billion |

$3.6 billion |

$4.4 billion |

$963 million |

|

Net Income |

$1.0 billion |

($186 million) |

$956 million |

$210 million |

|

Diluted EPS |

$4.62 |

(81¢) |

$4.37 |

97¢ |

(source: 10-K from SEC)

As you can see, Molson Coors revenue has been growing slowly, but steadily in recent years. The estimates for 2024 and 2025 also predict this will continue, and there is even some estimation for years down the road predicting continued slow growth.

The P/E ratio for the most recent year’s earnings is around 11.4. That’s right in the meaty part of the value range, but it’s only getting better in the years to come. Estimates for 2024 and 2025 put the earnings per share at $5.67 and $5.88, respectively. That gives us forward P/E ratios in the 8.78 range and will only continue to improve going forward.

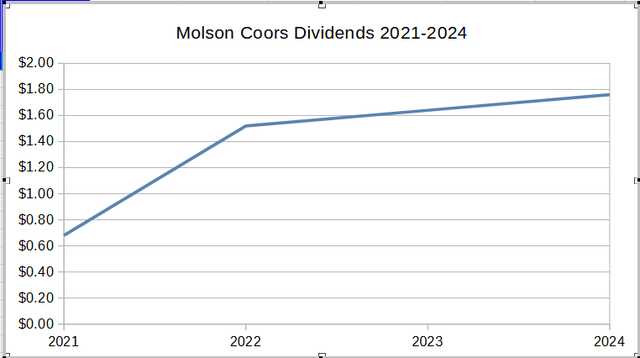

dividends for TAP

Molson Coors also pays some nice dividends, and those dividends have been growing in recent years. The company had temporarily suspended dividends in 2021 because of the coronavirus, but since then these been rock solid in paying, and fits nearly in the income growth range.

Conclusion

Molson Coors has really been beaten down in recent months, and is far from its 52-week highs. Maybe it’s fair for the price to have dropped off those highs, but in my opinion, they’ve gone too far.

Molson Coors is a rock solid company with strong earnings, and between the share buyback and the growing dividend, yielding over 3%, they are doing all the right things in returning value to the shareholders.

I see the company as a buy, particularly if you want to diversify your portfolio to include something in the beverage market. I personally used the sub-$50 price as an opportunity to enter the market recently, and I feel strongly about this being a buy and hold for the long term.

Read the full article here

")

")

")

")

")