")

")

")

")

")

Storefront of a Watsons Pharmacy in Singapore

Recently, I covered both Jardine Matheson Holdings Ltd. (OTCPK:JARLF;OTCPK:JMHLY) and Swire Pacific Ltd. (OTCPK:SWRAF;OTCPK:SWRAY;OTCPK:SWRBF;OTCPK:SWRBY), two storied Hongkong based conglomerates. These companies trade at relatively inexpensive valuations, part of which is presumably a consequence of their exposure to the Greater China market. CK Hutchison Holdings Limited (OTCPK:CKHUF;OTCPK:CKHUY) is another such group with a similar history. In fact, one of the group’s predecessors was the first company to list at the Hong Kong stock exchange, hence the HKEX ticker 00001. Today, it is much more focused on Europe than it is on its home market.

In recent years, CK Hutchison was not exactly a growth champion. Nonetheless, its valuation has become significantly more attractive over time, given the development of its share price. The stock now trades almost 50 percent lower compared to when I last covered it, assigning a hold rating at the time. Below, I will explain why I think that CK Hutchison offers attractive value at the current price.

China Discount Is Not Warranted

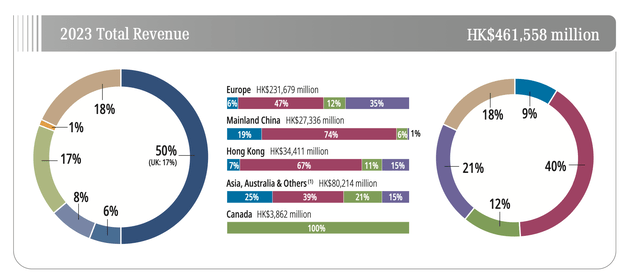

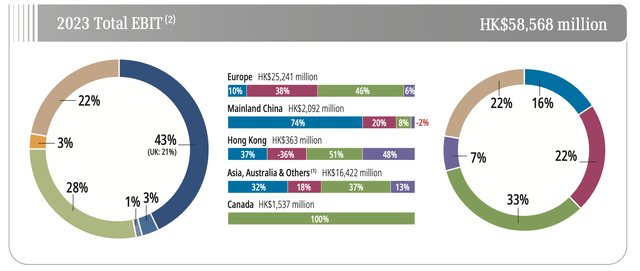

One obvious explanation for a low valuation would be a “China discount”. However, I would argue that such discount is not warranted in the case of CK Hutchison. While the company is headquartered in Hongkong, it is quite diversified geographically, with Europe being the most important market. Especially after spinning off the real estate division, CK Asset Holdings Ltd. (OTCPK:CHKGF), in 2015, the company no longer relies predominantly on Greater China. The region only accounts for 13.4 percent of revenue (7.5 percent of which Hongkong). In terms of profitability, it is even less important, with an EBIT contribution of Mainland China of 3.6 percent and an additional 0.6 percent attributable to Hongkong. Europe, meanwhile, accounts for a little more than half of revenue and 43 percent of EBIT (all figures based on FY2023 results).

CK Hutchison Revenue By Geography (CK Hutchison Holdings Ltd. Annual Report 2023, p. 4) CK Hutchison EBIT By Geography (CK Hutchison Holdings Ltd. Annual Report 2023, p. 4)

Valuation

Usually, the most straight forward method to value a company is to look at it based on a profit multiple. Currently trading at a little over 6 times 2023 earnings (HK$23.5 billion = around $3 billion), CK Hutchison is by no means expensive.

However, given its structure, I believe a sum of the parts approach to be more suitable in order to calculate the value of CK Hutchison. The group operates a central cash management for its unlisted subsidiaries. Long term financing is obtained at the group level and capital distributed as needed among the respective business. I will therefore value the unlisted entities on a debt free basis and subtract net debt afterwards.

CK Hutchison’s most important division is its Telecommunications segment. The telco business is grouped under the wholly owned subsidiary CK Hutchison Group Telecom Holdings Ltd. As parts of the respective subsidiaries and joint ventures are publicly listed, while others are not, I will value it by the sum of its individual parts rather than as a whole.

The asset that is easiest to value is a 66 percent interest in Hutchison Telecommunications Hong Kong Holdings Ltd. (OTCPK:HTCTF;OTCPK:HUTCY). At the time of writing, this represents a value of just shy of $400 million.

Hutchison Asia Telecommunications meanwhile comprises a number of different businesses. The most important of these is PT Indosat Ooredeoo Hutchison Tbk (OTCPK:PTITF) which is held trough Ooredoo Hutchison Asia, a 50 percent JV with Qatari Ooredoo Group which owns 66 percent of Indosat. Theoretically, CK Hutchison economically owns around a third of the shares, which currently represent a value of around $1.7 billion. There are also Vietnamobile, a joint venture with Hanoi Telecom (which owns 51 percent) operating in Vietnam, and Hutch Sri Lanka, a joint venture with the UAE’s state owned Etisalat. Frankly, I doubt that the latter two do move the needle in a significant way, so in terms of valuation, I am going with the $1.7 billion for 33 percent economic interest in Indosat.

The most important part of the division is 3 Group Europe, which comprises subsidiaries in UK, Italy, Sweden, Denmark, Ireland and Austria. CK Hutchison has agreed to a merger of the British subsidiary with Vodafone Group plc’s (VOD) UK business. Post transaction, CK Hutchison would retain 49 percent. CK Hutchison would have a put option and Vodafone would have a call option. The transaction currently faces an in-depth CMA inquiry, so it is not certain that it will materialize. If it does, the valuation of the combined entity would be valued at around GBP15 billion. Based on that, CK Hutchison’s stake would amount to about $9.5 billion at current exchange rates.

Going forward, consolidation on the respective European telco markets has the potential to create and unlock significant value. For the time being, I think it prudent to value three group Europe at a rather conservative revenue multiple of around 1 to be on the safe side. This would give it a value of around 10 billion (2023 revenue: HK$80 billion). Just keep in mind, that this figure might be considerably higher in reality.

The second largest of the group’s divisions is the infrastructure business. Most of this segment consists of a 75.57 percent interest in CK Infrastructure Holdings Ltd. (OTCPK:CKISF;OTCPK:CKISY). At the time of writing, this represents a value of $10.6 billion based on the subsidiaries market capitalization. In addition, CK Hutchison also holds direct stakes in some CK Infrastructure led projects. CK Infrastructure owns a geographically diversified infrastructure portfolio focused primarily on energy generation and transmission. It also holds a 36.01 percent equity stake in Power Assets Holdings Limited (OTCPK:HGKGF). Other than Power Assets Holdings’ Hong Kong and Chinese operations, CK Infrastructures exposure to mainland China is limited to around 150 kilometers of toll roads and bridges in Guangdong province.

CK Hutchison furthermore has exposure to a global portfolio of ports and related infrastructure held through its 80 percent interest (the remaining 20 percent are owned by Singapore’s PSA International) in Hutchison Port Holdings Ltd. That subsidiary is not to be confused with publicly listed Hutchison Port Holdings Trust (HCPTF), in which CK Hutchison has a 30 percent interest. In 2023, the segment generated revenue of HK$40.85 billion (around $5.2 billion) while posting HK$10.58 billion (around $1.28 billion) in EBIT. At conservative multiple of 5 that amounts to a value of around $6.4 billion.

CK Hutchison’s retail business is grouped under AS Watson Group. Temasek is a minority shareholder in AS Watson owning a 25 percent stake. Started as an eponymous Hongkong pharmacy, the group now comprises a diversified brand portfolio. AS Watson also has a 40 percent interest in German drug store chain Dirk Rossman GmbH. In 2023, AS Watson generated revenue of HK$183 billion (around $23.4 billion) and EBIT of HK$12.88 billion (around $1.65 billion). Applying a conservative multiple of 5 times EBIT, that translates to a value of $8.25 billion. Consequently, the group’s 75 percent stake should be worth around $6.2 billion. Greater China accounts for a little under a third of the segment’s revenues.

In addition to the aforementioned divisions, CK Hutchison also holds a number of financial investments (for reporting purposes, those are referred to as the “Finance & Investment” segment). The most important of these assets is a 16.69 percent stake in Cenovus Energy Inc. (CVE) which at the time of writing has a market value of around $6.3 billion. For perspective: this asset alone has a value of about a third of CK Hutchison’s current market capitalization.

Another significant asset is a 38.17 percent interest in biopharmaceutical company Hutchmed (China) Ltd. (HCM). At the time of writing, the investment has a market value of around $1.13 billion.

Smaller listed assets include a 45 percent interest in CK Life Sciences International Holdings Ltd. (listed at HKEX under the ticker symbol 775), which is at the time of writing had a market value of about $200 million. There is also a 36.1 percent stake in TOM Group Ltd. (OTCPK:TOCOF), a digital media conglomerate focused on the Hongkong market. Currently, this asset has a market value of around $90 million.

There are also some closely held subsidiaries, including French perfumerie chain Marionnaud, which was spun off from AS Watson about a decade ago. While I assume that this business represents a positive value, it is hard to pin a number on based on publicly available information. In any case, I doubt that it moves the needle in the grand scheme of things. Therefore, I will largely disregard Marionnaud for the time being. Through Hutchison Whampoa (China) Ltd., the company also operates diverse businesses in mainland China. That portfolio comprises quite a potpourri of largely unrelated businesses spanning aircraft maintenance, agriculture, consumer products of various kinds. For these businesses, a substantial “China discount” is warranted in my opinion. I will, therefore, exclude them from my valuation. Indirectly, through a 87.87 percent stake in Hutchison Telecommunications (Australia) Ltd., the group also controls 25.05 percent of TPG Telecom Ltd. (OTCPK:TPGTF). This asset has a value of around $1.23 billion. I would, however, argue that a sizeable discount is in order. Notably, CK Hutchison does not group it under the Telecommunications segment for reporting purposes.

Adding up these parts, one would arrive at around $44.6 billion. After subtracting consolidated net debt of around HK$130.5 billion (16.65 billion), one arrives at a sum of the parts value of close to $38 billion. Even applying a sizeable conglomerate discount of around 30 percent, this would still amount to $26.6 billion. Based on a market capitalization of around $18.65 billion, that would translate to more than 40 percent upside. And keep in mind that the consolidated debt figure takes into account debt that should already be factored into the valuation of the respective listed subsidiaries. Notably, the listed stakes alone represent a value of currently around $22 billion, or 20 percent above the current market valuation.

Attractive Dividend

CK Hutchison tends to pays attractive, but not necessarily stable (the dividend was cut by around 13 percent compared to FY2022) dividends. Distributions are usually made bi-annually, with a smaller amount paid as interim dividend and a larger final dividend. For FY2023, the company paid a cumulative dividend of HK$2.53 (around $0.32) per share. Assuming a distribution in line with that for 2024, this translates to a dividend yield of around 6.7 percent. The relatively high dividend yield is, in my assessment, more a function of the low valuation than it is the result of a particularly superior dividend policy. In recent years, the payout ratio was usually between roughly 30 and 40 percent, which appears sustainable.

Risk Factors

As with any investment, there are certain risks to be considered. As I alluded to above, I don’t believe that a “China discount” is warranted for CK Hutchison as a whole. Being under de facto Chinese jurisdiction may, however, be disadvantageous given an increasingly cautious sentiment vis-à-vis all things China among European governments. The telco business in particular might face scrutiny, especially with regard to further consolidation by way of mergers and/or acquisitions.

Another downside is the unnecessarily complicated group structure. Having minority shareholders and joint ventures at various levels inevitably adds complexity. Nor are intra-group cross-shareholdings usually considered particularly desirable by capital markets.

One should furthermore be aware of an inherent currency risk. CK Hutchison is especially vulnerable to a strong US Dollar, as it tends to lend in Dollar while generating most revenues in other currencies. There is also some uncertainty regarding the future of the Hongkong Dollar peg to the US Dollar. If the Hong Monetary Authority would no longer be able or willing to keep the currency pegged to the US Dollar, that might disproportionately impact CK Hutchison and deteriorate its balance sheet quality markedly. While not an acute risk, in my assessment, I would not entirely rule out such a scenario. Notably, there has been some speculation in this regard not too long ago.

Another issue is the quality of leadership. Executive chairman Victor Li – unlike his father and predecessor, Li Ka-Shing – does not have a great track record so far. A common theme with family controlled companies is that leadership does often not automatically pass to the most qualified person. I would, however, argue that Mr. Li, Jr.’s performance is not abysmal, either. Also, Mr. Li, Sr. remains somewhat engaged as a senior advisor.

Conclusion

All in all, I think that CK Hutchison is currently undervalued by around 40 percent. Based on the sum of its part, I believe that the stock represents a fair value of up to $6.8 per share. Consequently, I am assigning a buy rating. Investors should, however, be aware of what you are buying with this company. CK Hutchison is not a growth investment. With this stock, it is all about value. Also, I don’t think that the valuation gap will close overnight. A long term investment horizon is required in order for CK Hutchison to make sense as an investment. Those who have, may also collect a relatively sizeable dividend while waiting for the share price to catch up. In the meantime, the mature nature of core businesses and the inexpensive valuation offer some downside protection.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")

(OTCMKTS:DTEGY)")