")

A great way to reduce risk in one’s portfolio is to own a basket of stocks. While it’s easy to simply buy a lot of stocks, one must also consider valuation risk.

For example, a portfolio may have 20+ or so stocks, but if all of them are overvalued tech and growth stocks, then a sector downturn would have a broadly negative effect over the portfolio.

That’s why I prefer to have a good mix of value stocks that pay dividends in various industries. That’s because no matter how sure one is over a company’s prospects, there are no guarantees, and you wouldn’t want for any one stock to tank the portfolio returns.

This brings me to the following 2 picks, both of which are well established companies with yields ranging from 7-9%. Both stocks are beaten down in price, seemingly with risks already priced into their valuations. Let’s explore what makes them potentially great additions to a diversified income basket!

#1: BCE Inc.

BCE Inc. (BCE) is one of the Big 3 Canadian telecoms, alongside peers Telus (TU) and Rogers Corp. (ROG). Much like the US, with AT&T (T), Verizon (VZ), and T-Mobile (TMUS), the Canadian telco space has been whittled down to 3 players after ROG acquired Shaw Communications back in 2021. BCE is also the most diversified telco amongst its peers with wireless, broadband, and TV/Media offerings.

BCE hasn’t been a high performer over the past 12 months, with the stock declining by 28%. One of the drivers behind the decline has been the impact of higher interest rates on dividend-focused stocks in general, as higher rates create competition from fixed income and also results in higher interest expense.

Another factor behind the recent decline has do to with the CRTC (Canada’s telco regulator) requiring major cellular providers to open up their broadband networks to smaller rivals at prescribed rates. This could result in more competition for BCE and lower prices that it can charge. As a result, BCE plans to cut capital spending by $1 billion over the course of this year and 2025.

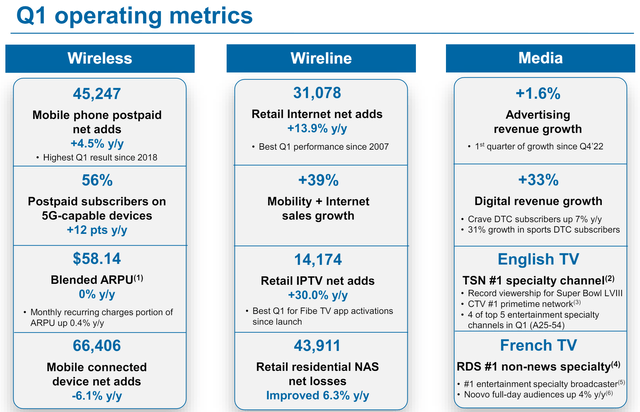

Despite uncertainty around CRTC’s actions and what they mean for BCE over the medium term, BCE continues to produce steady results. This includes growing mobile phone postpaid net adds by 4.5% YoY during Q1 2024, the highest Q1 result since 2018. BCE was able to achieve this amount of subscriber growth while keeping pricing steady at an ARPU (average revenue per user) of $58.14, which is unchanged from the prior year period, as shown below.

Investor Presentation

Moreover, BCE saw a solid 14% YoY growth in broadband connections, representing the best Q1 performance since 2007, and advertising revenue grew by 1.6% YoY. This was driven by 33% growth in digital revenues and CTV holding its #1 position for primetime viewership, and BCE retaining 4 of the top 5 viewership spots for specialty entertainment channels.

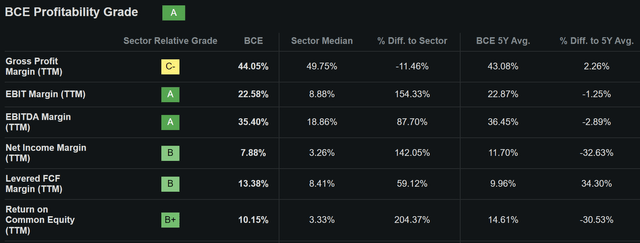

Importantly, BCE is also growing its bottom line, with adjusted EBITDA improving by 1.1% YoY, and adjusted EBITDA margin expanding by 80 basis points to 42.7%. As shown below, BCE scores an ‘A’ grade on Profitability compared to peers in the Communications Services sector.

Seeking Alpha

Management reaffirmed financial guidance for 2024, including 2% revenue growth and 3% adjusted EBITDA growth at the midpoint of range. It also expects to achieve between $150 and $200 million worth of cost efficiencies this year as a result of workforce restructuring this year, and reduce capital spend by $500 million this year, with a focus on core network investments and improving operational efficiency.

Meanwhile, BCE maintains a BBB+ investment grade credit rating from S&P and has $4.7 billion in available liquidity, including $789 million in cash. It has no remaining debt maturities this year and has a debt to EBITDA ratio of 3.6x, with an internal target of reaching 3.0x.

The drop in BCE’s price has resulted in a 9.0% dividend yield. While the dividend-to-FCF payout ratio is at 107% over the trailing 12 months, I would expect for this ratio to improve based on management’s plan to reduce capital spending this year and next.

Plus, the dividend is well-covered by operating cash flow, with a 45% payout ratio based on this financial metric over the trailing 12 months. It’s also worth noting that management raised its dividend rate by 3% this year.

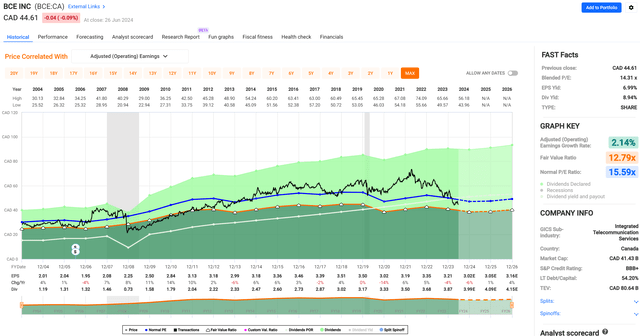

At the current price of $32.39, I find BCE to be appealing with a forward PE of 14.7. Because earnings takes into account depreciation, which is derived from capital spending, lower CapEx over the next couple of years should equate to higher earnings while holding all else equal. As shown below, BCE currently trades below its historical PE of 15.6.

FAST Graphs

With a 9.0% dividend yield, BCE would only need to produce around 1% annual EPS growth to achieve market level total returns. Sell side analysts who follow the company estimate 2-4% annual EPS growth between 2025-2026, which I believe is reasonable considering plans for reduced capital spending and respectable growth in wireless customers. As such, BCE appears to be a great choice for value investors who prize getting the majority of total returns in the form of dividends.

#2: Bank of Nova Scotia

Bank of Nova Scotia (BNS), otherwise known as Scotiabank, is one of the Big 5 Canadian Banks alongside peers TD Bank (TD), Royal Bank of Canada (RY), Bank of Montreal (BMO), and Canadian Imperial Bank of Commerce (CM). It operates in personal and commercial banking, global wealth management, and capital markets.

What sets BNS apart from its peers is that it also has a meaningful presence in Latin America, giving it another avenue for growth beyond its traditional Canadian market.

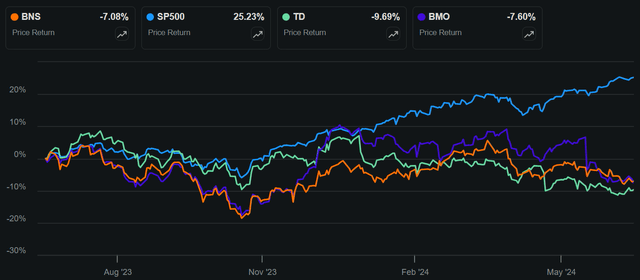

Uncertainty over the direction of interest rates and what higher rates could mean for borrowers’ ability to service their debt has weighted on BNS and its close peers. As shown below, the stock has declined by 7.1% over the past 12 months along with the 10% and 8% declines of TD and BMO respectively, underperforming the 25% rise in the S&P 500 (SPY) over the same time frame.

BNS vs. Peers 1-Yr Price Return (Seeking Alpha)

Despite these concerns, BNS grew its Q1 2024 revenue by 5% YoY, driven by higher net interest income, non-interest income, and positive impact of foreign currency translation. Higher interest rates also continue to benefit BNS, as the Canadian Banking unit saw net interest margin expand by 26 basis points YoY. Its worth noting, however, that return on equity declined by 1 percentage point to 11.2% due to higher provision for credit losses and higher expenses.

While economic uncertainty and potential for lower in mark-to-market valuations on the Canadian property market weights on BNS, its core operating performance remains strong, with banking deposits growing 7% YoY. This figure far outpaced Scotiabank’s relatively steady loan book, which declined by just 1% YoY during the first quarter.

International Banking continues to be a bright spot for BNS with revenue and deposit growth of 6%, and net interest margin expansion of 11 basis points YoY. Moreover, Wealth Management saw earnings and AUM growth of 8% and 6% YoY, respectively.

The outlook for BNS remains choppy in the near term, as management expects the current high interest rate environment to weigh on its borrowers, and they expect for PCL (provision for credit losses) to be at the high end of the 2024 guidance at 55 bps of total loan book.

On the other hand, management appears to be prepared for an uncertain market by raising the CET1 (common equity tier 1) ratio by 90 basis YoY to 13.2%, sitting comfortably above the 11.5% minimum requirement set by Canada’s banking regulator. BNS also carries a strong A+ credit rating from S&P.

Importantly for income investors, BNS currently yields an attractive 6.9%. The dividend is well-covered by a 67% payout ratio and comes with a 5-year CAGR of 4.6%.

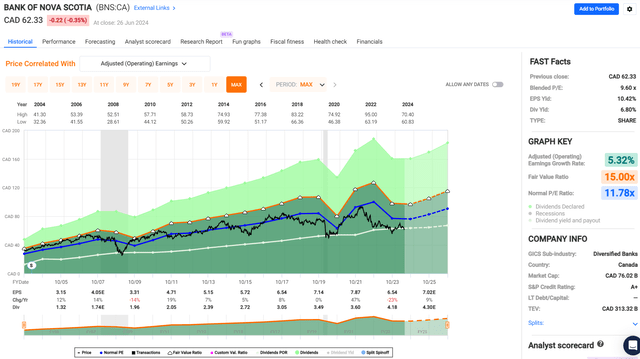

Lastly, I find BNS to be highly attractive at the current price of $45.57 with a forward PE of 9.6, sitting well below its historical PE of 11.8, as shown below.

FAST Graphs

At the current PE, it seems that a lot of potential headwinds are already baked into the price while the potential positives from continued deposit growth, interest margin expansion, and growth in global wealth management are being largely ignored.

Sell side analysts who follow the company estimate 6-11% annual EPS growth in 2025-2026, while I have a more conservative estimate of around mid-single digit EPS growth based on a more cautious outlook for Canada and Latin America. Even with my base case scenario, BNS could produce market beating returns in combination with its near-7% dividend yield, offering investors plenty of value at the current price.

Investor Takeaway

BCE Inc. and Scotiabank can provide great diversification and high yields for income-focused investors due to their undervaluation and established market positions. BCE, a diversified Canadian telecom, offers a 9.0% yield and has demonstrated steady growth in mobile and broadband connections, despite recent regulatory and interest rate challenges.

Meanwhile, Scotiabank, one of Canada’s big five banks with significant operations in Latin America, provides a 6.9% yield and has shown resilience with robust deposit growth and interest margin expansion. Both companies are trading at attractive valuations, suggesting that potential risks are already priced in, making them potentially valuable additions to a diversified income portfolio.

Read the full article here

")

")

")