")

Federal Reserve guidance has been in flux these past few months. We had a hawkish Fed during most of 2023, with significant rate hikes and hawkish guidance. The Fed began to pivot in very late 2023, and guided for several rate cuts this year. These have failed to materialize, due to a lack of further progress on inflation. Off course, the latest CPI figures show no change in prices this past May, which could presage a dovish shift in the coming months. Assuming inflation remains extremely low, at least.

Considering the above, and as the Fed continues to expect some rate cuts this year, thought to have a thought to have a closer look at how interest rates stand right now.

Rates remain elevated, with basically all fixed-income asset classes offering above-average yields. Treasuries and investment-grade bonds have seen their yields rise YTD, as sentiment and guidance turns hawkish.

Credit spreads have tightened and are nearing historical lows. Higher-quality, investment-grade bonds seem much more attractive than high-yield bonds right now, on risk-adjusted grounds at least.

Expectations have turned hawkish, with the market expecting fewer rate cuts in the coming years. This increases the attractiveness of long-term bonds vis-à-vis short-term and variable rate securities. In my opinion, expectations are reasonable, so I’m not expecting significant outperformance from either group moving forward.

Considering the above, I’m quite bullish on most bonds and fixed-income sub-asset classes, with investment-grade bonds offering particularly strong risk-adjusted yields and returns.

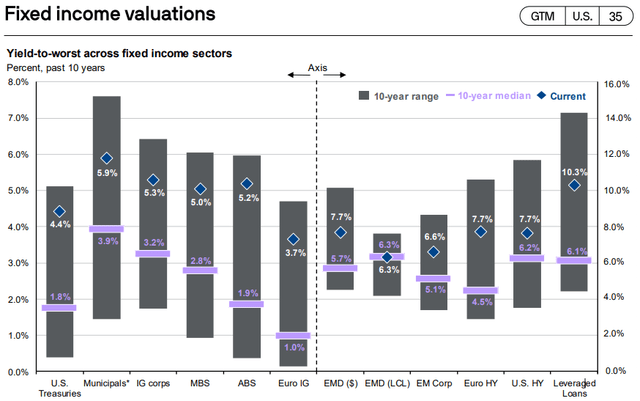

Rates Remain Elevated

Interest rates are currently elevated, due to past Federal Reserve hikes. Rates are significantly higher than long-term historical averages, across fixed-income asset classes. Spreads are particularly wide for treasuries and senior loans.

JPMorgan Guide to the Markets

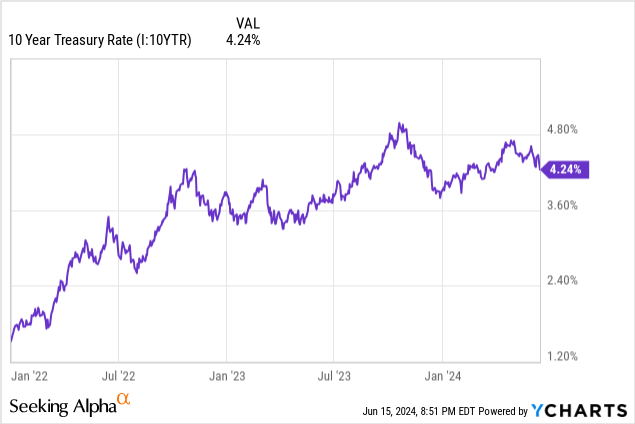

Interest rates are higher now than during most of the past two years, with some exceptions.

Data by YCharts

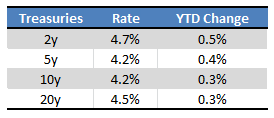

Rates have also increased these past few months, as inflation remains stubbornly above target, and both investors and the Fed have become more hawkish. Recent inflation data has somewhat reversed this trend, but not completely. Benchmark 10y treasury rates are up 0.3% YTD, with shorter-term treasuries seeing marginally higher increases.

Seeking Alpha – Table by Author

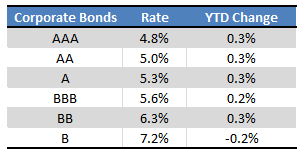

Corporate bond interest rates are also up, with the exception of B-rated bonds. In other words, credit spreads are tightnening.

Seeking Alpha – Table by Author

Above-average rates increase the attractiveness of bonds as an asset class, for obvious reasons. I’ve argued the same in the past, with most of my top picks performing quite well.

Elevated rates also increase the attractiveness of high-yield bonds, senior loans, and CLOs versus equities. The Panagram BBB-B Clo ETF (NYSEARCA: CLOZ) offers investors a 9.3% yield without significant credit risk, while the VanEck BDC Income ETF (NYSEARCA: BIZD) sports a growing 10.5%, albeit with high credit risk. Equity valuations seem elevated, including those centered on earning yield spreads to bond rates.

JPMorgan Guide to the Markets

So, bonds and high-yield bonds currently trade with attractive prices, valuations, and yields. Equities do not.

In my opinion and considering the above, income investors, retirees, and investors looking for strong risk-adjusted returns should focus on bonds over equities. I still expect equities to outperform long-term, but at much greater risk. Investors should be able to achieve equity-like returns without equity risk through high-yield bonds and similar investments. At the same time, do remember that equity returns are not equal to safe withdrawal rates. Investors must generally withdraw less than the stock market returns, to keep their portfolio safe long-term, and to prevent excessive selling during downturns and bear markets.

Tight Credit Spreads

Credit spreads are currently narrower than average, with non-investment grade corporate bonds yielding around 3.3% more than treasuries of comparable maturities. Long-term spreads average 5.6%, more than 2.0% higher than prevailing rates.

JPMorgan Guide to the Markets

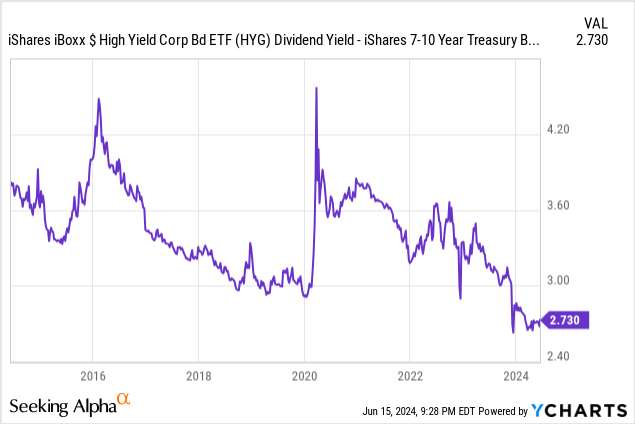

Narrow credit spreads are also apparent between high-yield and treasury ETFs. The benchmark iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA: HYG) currently yields 2.7% more than the iShares 7-10 Year Treasury Bond ETF (NASDAQ: IEF), lowest spread in history.

Data by YCharts

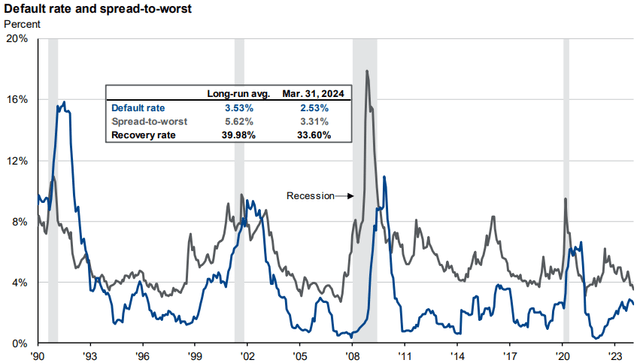

Default rates are also higher than average. S&P estimates these at 4.9%, compared to a long-term average of 4.1%. Accounting for compositional issues, default rates drop to 4.3%, only marginally higher than average.

Considering the above, it seems clear that investment-grade bonds and securities offer comparatively strong risk-adjusted returns and yields right now, at least compared to high-yield bonds. I’m still bullish on the latter, as their yields remain attractive.

Some specific figures on the above. Right now, treasuries yield 2.6% more than average. Investment-grade bonds yield 2.1% more, while high-yield bonds yield 1.5% more. Conditions seem bullish for all, although obviously more for treasuries.

JPMorgan Guide to the Markets

Considering the above, I think investors should lean towards high-quality, investment-grade securities over riskier ones. I have a couple of good choices in this regard.

The Angel Oak Income ETF (NYSEARCA: CARY) is an above-average one, with a diversified portfolio of fixed-income securities, and a 6.1% dividend yield.

The Janus Henderson AAA CLO ETF (NYSEARCA: JAAA) is a fantastic one, with an incredibly stable share price, extremely low credit risk, and a 6.4% dividend yield. JAAA focuses on AAA-rated CLO tranches, which are variable rate investments. Dividends should decrease as the Fed cuts.

The Janus Henderson B-BBB CLO ETF (BATS: JBBB) is another great choice, with below-average volatility, low credit risk, and a 7.8% dividend yield. JBBB focuses on BBB-rated CLO tranches, so dividends should also decrease as the Fed cuts rates.

As mentioned previously, high-yield bonds continue to offer above-average yields, so I remain bullish on these. Spreads do advantage investment-grade bonds, however.

Expectations Turning Hawkish

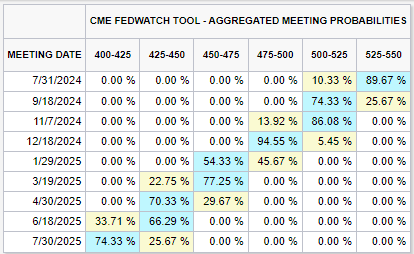

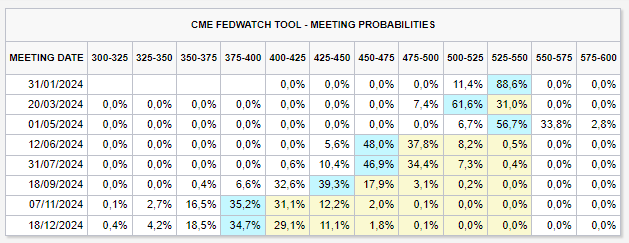

Right now, the market expects some rate cuts in the coming years. Specifically, futures markets are pricing 2 cuts this year, followed by 3 cuts next year.

CME FedWatch Tool

Expectations are much more hawkish, or less dovish, than before. Investors expected 5-6 cuts this year during mid-2023, for instance.

CME FedWatch Tool

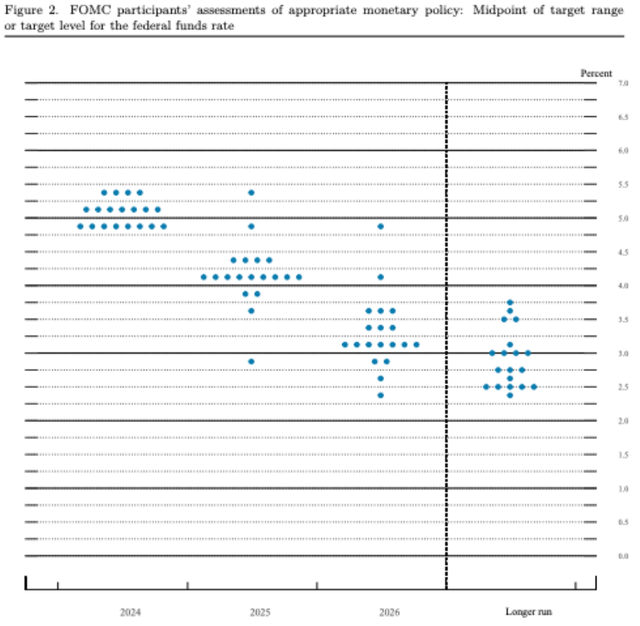

Market expectations seem slightly more dovish than those from the Fed.

Federal Reserve

Expectations have shifted as inflation has remained above target during most of the year. The latest CPI report was an outlier in this regard and could presage a dovish shift if monthly inflation remains at 0% moving forward.

As investors are pricing a couple rate cuts already, bond prices might not necessarily fall that much in the event of slight / moderate rate cuts. Do note that the market is not expecting significant rate cuts, so these would almost certainly impact bond prices.

In my opinion, market expectations are broadly reasonable, so I’m not expecting significant increases to bond market prices from Fed cuts: these seem priced-in already. I’m not expecting significant outperformance from either short-term or long-term bonds either, for the same reason.

Notwithstanding the above, I still have a slight lean towards short-term and variable rate investments, as these offer above-average yields right now, and Fed cuts are not a 100% certainty. This is a very slight lean though, and mostly on risk / uncertainty grounds.

As a final point, although the above might seem a bit wishy-washy, it does reflect my understanding / thoughts on the market. In prior articles, I was much more bullish on short-term and variable rate investments, as I believed market conditions at the time were advantageous for these investments. Right now, the situation is more muddled.

Conclusion

Interest rates remain elevated, with effectively all fixed-income asset classes trading with above-average yields.

Credit spreads have tightened and are nearing historical lows.

Expectations have turned hawkish but seem reasonable.

In my opinion, and considering the above, bonds and fixed-income are a broad buy. Investment-grade bonds seem like a particularly strong choice.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")