")

")

Times have not been good for lifestyle brand owner Vera Bradley (NASDAQ:VRA). Back in December of 2021, I wrote an article that took a bullish stance on the company. Even though I acknowledged that the company had a mixed operating history, financial performance that was available for the first half of the 2022 fiscal year was encouraging. Revenue, profits, and cash flows were all higher year over year. Add on top of this how cheap shares were, not only on an absolute basis, but also compared to similar companies, and I could not help but to rate the company a ‘buy.’.

Since then, shares of the business have plunged 17.4%. This is a far cry from the 17.6% increase seen by the S&P 500 over the same window of time. In my opinion, this return disparity was not entirely unwarranted. Revenue generated by the company has taken a beating, and bottom line performance has been mixed. Management has implemented a program aimed at improving operations. But while profits and cash flows have improved since then, we have not seen any positive impact on the company’s top line. The good news is that shares are still very cheap. But there is no denying that there is a great deal of risk with this play.

One positive is that, in the coming days, we should have additional data about the health of the enterprise. This is because, before the market opens on June 12th, management is expected to announce financial results covering the first quarter of the 2025 fiscal year. Leading up to that point, analysts expect much of the same. This means shrinking revenue but improved profitability on a year-over-year basis. This creates a rather complicated situation that will result in either significant upside for investors in the long run or significant downside, depending on whether or not management’s initiatives are playing out as planned. The value investor in me fines the opportunity speculative, but attractive. And for investors who don’t mind taking risk, this might be an interesting prospect to consider.

Mixed results

As I mentioned at the start of this article, Vera Bradley is a lifestyle brands business. Essentially, its emphasis is on promoting two different brands. The first of these is its namesake Vera Bradley brand, while the other is Pura Vida. The first of these, Vera Bradley, is a designer of women’s handbags, luggage, travel items, fashion and home accessories, and more. As of the end of the 2024 fiscal year, the company had 43 full line stores and 81 outlet stores dedicated to these products. In addition to this, the company also sells these products to roughly 1,600 specialty retail locations throughout the US. Examples include department stores, third-party e-commerce sites, liquidators, and more. It also generates some royalties from licensing the brand name to its customers. The other brand, Pura Vida, is a digitally native lifestyle brand that focuses on bracelets, jewelry, apparel, and more. In addition to selling its products online, Vera Bradley sells Pura Vida products to wholesale retailers, department stores, and other customers.

Author – SEC EDGAR Data

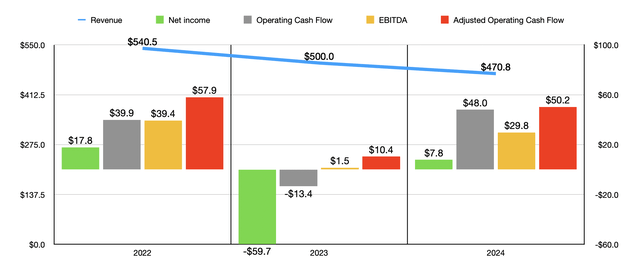

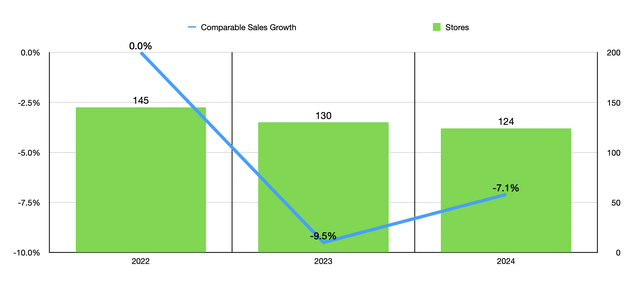

Over the past few years now, financial performance achieved by Vera Bradley has been mixed. Revenue dropped from $540.5 million in 2022 to $500 million in 2023. By 2024, revenue had fallen further to $470.8 million. This pain was driven by two factors. First, the number of locations that the company has in operation fell during this time from 145 to 124. In addition to this, comparable store sales have fallen in two of the past three years. In 2023, the sales decline was 9.5%. And in 2024, it was 7.1%. Combined, this is an aggregate comparable store sales drop of 15.9%.

Author – SEC EDGAR Data

Usually, retailers suffer tremendously when sales drop. This is because low margin, asset intensive businesses see significant margin contraction during periods of revenue weakness. But this hasn’t exactly been the case when it comes to Vera Bradley. As the first chart in this article illustrates, net profits and cash flows for the company fell from 2022 to 2023. But in 2024, the firm saw some improvements. Net income went from negative $59.7 million to positive $7.8 million. This was largely the result of a $63.8 million swing in the firm’s favor when it came to impairment charges. However, there’s more to the story than just that.

You see, in 2024, gross profit for the company came in at $256.4 million. That was up from the $238.9 million reported one year earlier. Management attributed this to lower year over year inbound and outbound freight expenses, a reduction in supply chain costs, the sell-through of previously reserved inventories, and lower year over year inventory reserve charges. This wasn’t the only improvement that the company saw. From 2023 to 2024, Vera Bradley saw its selling, general, and administrative costs drop from $265 million to $241.5 million. This decline of 8.9% was mostly due to employee related expenses falling as the company reduced its headcount. It is worth noting that the improvement would have been larger had it not been for increases in incentive compensation. But that’s largely because of one time severance costs related to the retirement of its CEO and because of the transition of its CFO. Other profitability metrics also improved during this window of time. Operating cash flow and from negative $13.4 million to positive $48 million. If we adjust for changes in working capital, we get an increase from $10.4 million to $50.2 million. And finally, EBITDA for the company expanded from only $1.5 million to $29.8 million.

When it comes to the 2025 fiscal year in its entirety, management expects revenue to remain range bound. They expect overall sales of between $460 million and $480 million. Operating cash flow is expected to fall to between $22 million and $24 million. But that very well could be because of working capital changes as opposed to other operational changes. Net income, meanwhile, should shoot up to between $16.3 million and $19.2 million. Given the uncertainty regarding these metrics, I think valuing the company based on 2023 and 2024 data would be more sensible.

Author – SEC EDGAR Data

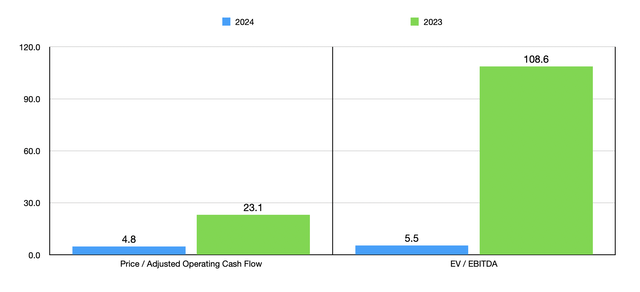

Following this approach, you can see how the stock is priced in the chart above. Using the 2024 figures, Vera Bradley looks quite cheap. I then, in the table below, compared the company to five similar firms. On a price to operating cash flow basis, I found that only one of the five companies ended up being cheaper than our candidate. The same also holds true when using the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Vera Bradley | 4.8 | 5.5 |

| Oxford Industries (OXM) | 6.7 | 11.2 |

| Lakeland Industries (LAKE) | 22.5 | 12.5 |

| Superior Group of Companies (SGC) | 5.3 | 11.5 |

| Movado Group (MOV) | 7.4 | 5.6 |

| Jerash Holdings (JRSH) | 4.3 | 4.0 |

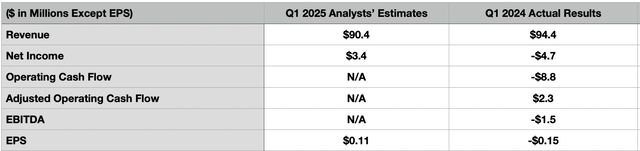

Of course, the picture can always change. And as I mentioned at the start of this article, management is expected to announce financial results for the first quarter of the 2025 fiscal year before the market opens on June 12th. The current expectation that analysts have is for revenue to total about $90.4 million. If this turns out to be correct, it would imply a year-over-year decline of 4.2% compared to the $94.4 million reported in the first quarter of 2024. Even though revenue is expected to fall, profits are expected to rise. Earnings per share should come in at around $0.11. That’s well above the $0.15 per share loss generated for the first quarter of 2024. This would translate to net income of $3.4 million, compared to the $4.7 million loss reported last year. Analysts have not provided estimates when it comes to other profitability metrics. But in the table below, you can see what some of these were for the first quarter of last year. In all likelihood, these should also improve.

Author – SEC EDGAR Data

Takeaway

The way I see it, Vera Bradley is a very risky play. Shares are cheap and there has been some nice progress on the company’s bottom line. If the firm can stabilize operations, with its store count eventually flat-lining and comparable store sales no longer falling, upside could be significant. But if we don’t see these things come to pass, the end result could be additional pain for investors. Clearly, this is not the kind of opportunity for those who can’t handle risk. For those who can, it could be a solid prospect. Of course, once earnings are announced, will have a better idea of where things stand. But absent some major change, that will only dispel short-term concerns. Due to these factors, I am keeping the company rated a soft ‘buy,’ with the understanding that it is truly a speculative one.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")