")

")

")

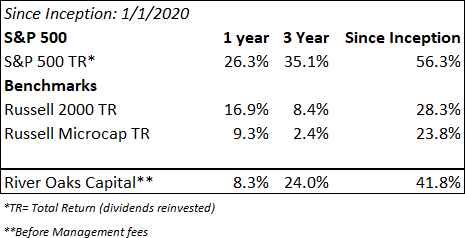

Performance

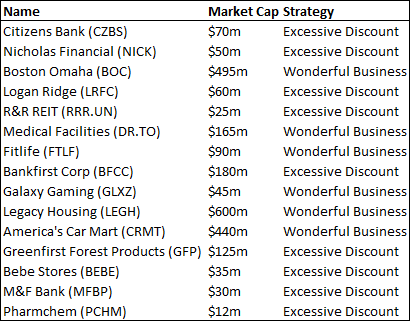

Our Companies

“When there is a frenzy of activity in one area of the market there is very often an anti-bubble of discarded companies”- Nick Sleep

Perhaps the most talked about news in the financial markets throughout 2023 was how incredible the stocks of the “Magnificent Seven” – Amazon (AMZN), Apple (AAPL), Google (GOOG,GOOGL) , META, Microsoft (MSFT), Nvidia (NVDA), and Tesla (TSLA) – performed versus the rest of the U.S stock market.

If you started 2023 with a market cap weighted portfolio of these seven stocks, you would have generated over a 75% return and over a 100% return with an equal weighted portfolio. This is compared to just a 12% return for the other 493 companies in the S&P 500! (SP500, SPX)

Although most of these seven stocks performed poorly in 2022, it is unprecedent for seven of the largest companies in the world – their average market cap is over $1 trillion – to drastically outperform the rest of the market. It is hard to even fathom where the money comes from that could create a collective $5+ trillion increase in market cap for the “Magnificent Seven” in just one year!

Some investors would say the reason for these astronomical 2023 returns are due to the rapid development of artificial intelligence, which will be a powerful tailwind in the future. Perhaps, other investors would just say this is a massive tech bubble with some similar attributes to 2000. Regardless of the reason for the “Magnificent Seven’s” 2023 performance, it has highlighted an important trend for our fund – the growth of passive investing. Passive investing is when instead of looking for mispriced stocks, an investor purchases a large basket of equities seeking to replicate an average stock market return. A common form is called ‘index investing.’

An example of this is when an investor buys all 500 companies in the S&P 500 through an ETF – Exchanged Traded Fund – instead of actively buying individual stocks they find attractive. Teresa, a 45-year-old U.S. accountant, works at KPMG. At the end of each month, she automatically invests $1,800 into her 401k. It’s likely that a significant portion of the $1,800 is being invested into an S&P 500 ETF or a similar investment vehicle. This trend has accelerated over the past decade. Historically, perhaps Teresa would have given the $1,800 to a money manager that would have actively picked stocks they found attractive. However, those days seem to mostly be long gone.

This growth of passive investing is not only happening at the individual level, but also at endowments, charities, corporations, etc. It is quite difficult to say precisely what percent of the U.S stock market is now passively invested money – most research seems to conclude it is now 50+% versus less than 15% in 2000 – but no matter how you measure it, the growth has been hard to digest. For instance, the big three index fund providers – Vanguard, State Street (STT) and Blackrock (BLK) – now own over 20% of the S&P 500!

The point here is not to criticize passive investing – it seems to be a net positive for the average investor – but rather to consider how this trend directly affects the small, underfollowed companies River Oaks Capital buys ownership in. One thing about passive investing seems certain. It disproportionately benefits larger public businesses as they are the companies that are both 1) included in indexes and 2) weighted the most heavily.

What percent of the phenomenal returns in the “Magnificent Seven” this year was driven by passive investing is a topic for another time, but it seems to have undoubtedly played some role.

“I have learned that the great opportunities are the places that have been neglected, where other people are not looking” – Sir John Templeton

I feel comfortable saying the growth in passive investing means less and less people are actively bargain hunting in publicly traded small, underfollowed companies.

This has both good and bad news for our fund. Let’s start with the bad news first.

When Teresa passively invests her $1,800 per month into index funds, almost none of that money goes into small, underfollowed public companies. Due to the small size and illiquidity – referenced in the last letter- of the small, underfollowed companies River Oaks Capital invests in, index funds are heavily constrained on being able to own these companies. For example, over the entire year BankFirst – a community bank we own – traded ~410,00 shares worth only $13m. It would take an entire year to buy just 7% of the bank on the open market. For a large index fund, it would be near impossible to buy meaningful shares in any company with a similar size and liquidity profile as BankFirst. This means passive investing will naturally direct more money towards larger companies. Right now, the average valuation of a company trading on the S&P 500 is over 22x earnings whereas the average multiple of the 15 companies we own is less than 8x earnings.

Now, the good news.

If very few investors were looking at small, underfollowed companies before the growth in passive investing, now it has become an isolated desert. There seems to be a consensus amongst many investors that small, underfollowed companies will permanently remain undervalued and investing in them will always create lower returns compared to larger companies. This has created an incredible set up for a fund that is willing to put in the work to dig up these inefficiently priced companies in this abandoned area of the market.

That’s where we can capitalize.

As River Oaks Capital puts in the necessary time requirement – often times travel is needed – of getting to deeply understand each company we own, alongside approaching each investment with a patient, business owner, long-term mindset, there are and will be incredible bargains on small, underfollowed companies.

However, the obvious question is: If no one is following these companies, how will they eventually get properly valued?

First, let us recall the qualities we look for in a company:

- Sells a wonderful product that will generate substantial cash for years to come

- Treats their customers, employees, and community admirably

- Is run by honest and able people that also have ownership in the business

- Does not take excessive risk

- Has a long-term plan for the business

- Is selling ownership at a significant discount to fair value

It seems many investors want to impatiently place a caveat at the end of the last bullet point which reads “…and will quickly be fairly valued.“

As small, underfollowed companies become ever more outcasted by investors the probability of them being fairly valued by ‘price discovery’ in a reasonable time frame is increasingly rare. ‘Price discovery’ is when investors find a company that is undervalued and bid up their stock price to a proper valuation. The trend away from ‘price discovery’ has been talked about by a few fund managers – notably David Einhorn – who invest in larger companies, but it is significantly more observable in small, underfollowed companies.

“As a value investor, what you are interested in is whether the company is creating wealth.”- Marty Whitman

Aside from the share price of a company increasing from ‘price discovery,’ there are truly only two other ways for a company to generate adequate returns for their owners:

- Return capital via dividends or share buybacks

- Re-invest the cash flow of the company back into the business at or above market returns

If either of these methods are executed properly by management, the value of our ownership in each company will continue to grow even if the share price doesn’t reflect it. That is why it is so important to put in the significant time requirement of getting to deeply understand the companies we own.

Without a true understanding of the business, confidence in our thesis, tracking the success of re- investment of cash flow, and reaching out to management and other fellow major shareholders, having a long-term mindset while investing in small, underfollowed companies would be near impossible.

We would eventually get frustrated by the lack of ‘price discovery’ in small, underfollowed companies – seeing the share price never move – and likely sell our shares. In fact, this is why the opportunity exists in small, underfollowed companies in the first place. Most investors aren’t willing to put in the time requirement without a short-term reward of an increased share price.

“I am an exponent of the philosophy that the main objective of common stock investment should be pricing, not timing; and by pricing, I mean the endeavor to buy securities at prices which are attractive, letting timing take care of itself”- Ben Graham

Eventually, neglected small, underfollowed companies will almost certainly get properly valued but the path to get there may be difficult for almost all investors to stomach.

For example, you buy ownership in a small, underfollowed publicly traded furniture store franchise with a mispriced market cap of $50m but a fair value of $100m that continues to grow at 10% per year. Despite management generating above market returns for their shareholders, the stock remains stagnantly priced at or below $50m for four straight years. Suddenly, one day you wake up and the market cap has instantly increased from $50m to $140m because it was bought out by a competitor.

This story is not uncommon, and as more and more investors run away from small, underfollowed companies, there will be a continuously less smooth path to get to fair valuation. Only those with a business owner, long-term mindset will be able to endure the patience required. My job is to put in the ‘time requirement’ to ensure that each small, underfollowed company we own is allocating capital – either via number 1 or number 2 mentioned above – at or above market returns while we wait. If they are, the question “how will they eventually get properly valued?” will take care of itself.

Part of that ‘time requirement’ this year included traveling to:

- Clearwater, Florida

- Omaha

- Dallas (2x)

- Fort Worth

- Bedford, Texas

- Atlanta (2x)

- Columbia, MS

- Las Vegas

- Peachtree Corners, GA New York

- Chicago

- Washington, DC

- New Orleans conference

As well as Zoom and conference calls with a countless number of companies from as far as Germany to as close as Rogers, Arkansas.

Quick Recap

As outlined in the River Oaks Capital’ owner’s manual’, our ultimate goal is to have our fund invested in 8-15 wonderful businesses that check all six bullet points listed in the previous section.

However, due to the infrequency of wonderful businesses that sell at a significant discount to fair value, along the way we will buy excessive discount companies which are so deeply undervalued – $0.50 or less on the dollar – that almost none of the first five bullets are needed as virtually any long-term outcome will generate an acceptable return.

Companies added in H2 2023

For the past six months, we’ve mostly been increasing our ownership in a few companies already in the fund as they have remained significantly undervalued despite underlying improvements in their business.

Medical Facilities is the only new company we have bought meaningful ownership in over the past six months. While we also bought ownership in Bebe stores, it remains below 3% of our fund.

Medical Facilities is now our sixth largest position. The company has a market cap of $165m and has majority ownership in four surgical hospitals located in South Dakota, Oklahoma, and Arkansas, as well as one surgical center in California. A surgical hospital offers a more personalized, high-end experience for patients who are undergoing scheduled, non-emergency surgeries. Most of these surgeries are ‘outpatient procedures’ – meaning no overnight stay – and mainly are orthopedic and neurosurgical operations – generally hip, knee and spine. Today, around 50% and growing of ‘outpatient procedures’ are performed in surgical hospitals. This is possible due to a rapid increase in technology.

Unlike most traditional hospitals, at Medical Facilities’ four surgical hospitals you get first class amenities (e.g., a prime rib dinner). Their facilities are often referred to as hotel hospitals and typically only used by people who can afford these higher-end services. As is common at surgical hospitals, Medical Facilities owns a majority of each hospital – 51% to 65% – while a select number of doctors who work in the hospitals own the remaining minority portion.

Medical Facilities started in 2004 when they publicly listed in Canada for tax advantages. For years following their IPO, Medical Facilities was very attractive to Canadian retail investors as the company consistently paid a ~6-10% dividend yield – $26m-$32m per year – that helped supplement their retirement income.

In 2016, the prior Medical Facilities management team decided to change their capital allocation strategy and started to rapidly acquire new assets. They purchased majority ownership in Unity Medical Surgical hospital in Indiana as well as seven surgical centers – smaller, outpatient-only facilities. In total, they spent over $100m, causing a large increase in debt and overhead expenses. None of the acquisitions worked out as planned and by the end of 2019 they had to begin cutting their dividend.

These problems were further exacerbated by Covid-19, which especially hurt their seven newly acquired surgical centers. By the end of 2020, they had decreased their dividend by 75% – down to $6m per year – causing Canadian retail investors to run for the door. The market cap, which was as high as $450m prior to their acquisition spree, plummeted to $120m.

By 2022, investment fund Converium Capital launched an activist campaign that took control of the Medical Facilities’ board and replaced the CEO and a large portion of their management team. The new CEO, Jason Redman, changed the corporate strategy — suspending all acquisitions, divesting non-core assets, paying down debt, cutting corporate costs and returning capital to shareholders.

Since early 2022, Jason has held true to his word as they have sold Unity Hospital and 6 surgical centers, cut corporate costs from $12m to $8m per year, paid down $12m of corporate debt, and repurchased $45+m of shares equating to 25+% of all outstanding shares. Prior to Medical Facilities, Jason already had a history of stepping into struggling companies and quickly turning them around in preparation for a sale or new strategic direction.

Now that the short-term goals have been accomplished by Jason and his team, the remaining question is: what are the next steps?

I have spent time talking with activist shareholder Michael Rapps of Converium Capital and other large shareholders and everyone seems aligned that the goal is to return capital to shareholders as soon as possible in one of the following ways:

Four possible scenarios over the next 1-3 years:

- Sell their ownership in all four of the remaining hospitals to a large, strategic buyer for $300+m

- This is probably the best-case scenario for Medical Facilities shareholders.

- The problem is there are only a limited number of companies – Tenet (THC), Surgery Partners (SRGY), amongst a few others – that can afford to buy all four hospitals together.

- Additionally, most of these large, serial acquirers of surgical hospitals bring in a formulaic ‘corporate’ culture.

- Recall that the doctors own a minority percentage of each hospital.

- Although the doctors do not have the right to veto Medical Facilities selling their majority ownership to a specific company, they could make the transition for the new acquirer very difficult by either refusing to work or retiring.

- It is hard to gauge how realistic this risk is as many of the doctors own the hospital and would therefore be hurting their personal equity value by not cooperating.

- Sell their ownership in the Arkansas and Oklahoma hospitals to individual buyers at or above their historical purchase price of ~$40m each.

- The two South Dakota surgical hospitals – Rapid City & Sioux Falls – are the cash cows of the company, generating ~70% of the free cash flow. The company also owns the related real estate.

- Most likely, the Arkansas and Oklahoma hospitals wouldn’t get as high of a multiple on a sale versus all four being sold at once.

- Using a conservative assumption that $60m of cash is received from the sale Arkansas and Oklahoma – assuming some of the non-recourse debt is tied to these hospitals – Medical Facilities would use the proceeds to buy back 30+% of their shares at current prices.

- Sell their ownership in each hospital individually to local buyers

- This would also get a lower pay out than if all four hospitals were sold at once as local hospitals wouldn’t pay the same multiple as a major corporation such as Tenet or Surgery Partners.

- However, it would most likely solve the problem of doctors not being happy with the deal as the culture of the hospital would not change.

- One roadblock is Medical Facilities’ ownership in the two South Dakota hospitals each could be worth $100+m which is a very large check for a local hospital.

- Increase the dividend

- If they can’t find a buyer at an attractive price for their ownership in the four hospitals – especially the two in South Dakota – they can use their $20-$25+m of free cash flow to equity per year to pay a 12-15% dividend yield – even over 15% if they continue to buy back shares at current prices.

- This would most likely re-attract the Canadian retail investors that fled the stock once the dividend was cut and thus increase the share price.

As mentioned, Medical Facilities currently generates free cash flow to equity of $20-$25m per year which should continue to grow at or above inflation. On a market cap of $165m, that is a 12-15% free cash to equity flow yield – 6-8 P/E ratio. Furthermore, a strategic acquirer would be able to eliminate a large percentage of the $8m of corporate overhead costs, meaning they would be able to generate $25-$30+m of free cash flow year – not including other potential synergies. The sale of all four hospitals for $250-$300+m seems to be quite a reasonable assumption – generating a 50-80%+ return for current shareholders.

Regarding downside protection, Medical Facilities is selling at 20+% below historically paid prices for each hospital – a large percentage of which was purchased 20 years ago. For reference, in 2015 they sold a surgical hospital they bought in 2005 for 3x the historical cost.

In summary, due to their dividend cut in 2019, being listed on the Canadian stock market, and not screening well for those searching for undervalued companies, Medical Facilities has been abandoned by investors allowing us to invest in a wonderful business at an overly discounted valuation.

Updates from H1 2023 Letter

ECIP Community Banks: Citizens Bank (OTCPK:CZBS), BankFirst (OTCQX:BFCC), M&F Bank (OTCPK:MFBP)

In 2022, we invested in three community banks – Citizens Bank, BankFirst and M&F Bank. At the time, they had each recently received an extraordinary amount of ECIP (Emergency Capital Investment Program) funding from the U.S government, a capital infusion which completely transformed their earnings potential.

And while 2023 was a tumultuous year for community banks in general, our three companies have weathered the storm well and are in a great position for future growth. As you likely remember, the year started off with the notable collapse of Silicon Valley Bank – the third largest bank failure in U.S history. This sent a widespread fear that deposits from smaller banks would flee into ‘systemically important’ banks such as JP Morgan Chase, Bank of America, etc.

In the latter half of 2023, there were concerns of an impending recession alongside elevated interest rates and what that would mean for community banks’ ability to lend out money – especially in the lower income communities, which are feeling economic pressures the hardest. Although some of these concerns have come to fruition, as lending has slowed down this year and deposits have remained flat or slightly declined, it has been an opportunistic time for ECIP community banks.

Each of the three ECIP community banks we own sit on a hoard of cash, which they have been able to lend out at 3-4+% higher interest rates compared to when they first received their ECIP capital in mid- 2022. While deposit rates have increased as well, they have not increased at nearly the pace of lending rates. Furthermore, recall that the maximum interest rate each bank will have to pay on their ECIP capital is just 2%!

Despite this beneficial set up, our three ECIP community banks remain incredibly undervalued. The market still seems to have a lingering fear from the Silicon Valley Bank collapse and a short-term concern about our community banks having to ‘mark down’ some of their older fixed loans that were made at much lower rates than today. Optically, this may cause a few quarters of lower accounting earnings, but over the long term a higher interest rate environment should have a positive impact on the sustainable earnings power of all three banks, each of which has significantly more cash – and a fixed 2% liability – when compared to their non- ECIP competitors.

Citizens Bank (OTCPK:CZBS) is a community bank located in Atlanta, Georgia. It is the largest position in our fund and now has a $70m market cap. In May, I attended the shareholders meeting where the only outside attendees were myself and two other shareholders. The Citizens Bank team gave us each a turn to ask questions and make any suggestions. CEO Cynthia Day, Chairman of the Board Ray Robinson, and the rest of team clearly took those suggestions to heart.

One of the main shareholder suggestions has been for Citizens Bank to start releasing a quarterly statement that gives a high-level overview of how well the bank is performing – making it clear how undervalued the bank is. At the end of Q3 of this year, the Citizens Bank team did just that!

They issued a quarterly press release highlighting their incredible annual earnings growth of 86%, their strong capitalization position with cash and marketable securities of ~$299m, and other details outlining their tremendous year so far. However, the most important news of the press release was yet another buyback announcement – this time for $4.5m. They have nearly completed the buyback in just three months. Cynthia and her team are now fully taking advantage of their extremely mispriced stock and seem intent on continuing to buy back shares.

During 2023, they will have bought back 10+% of their shares, $8m+, and paid a ~2% dividend yield. In total, a 12+% shareholders yield. Cynthia and her team are not waiting for investors to have a ‘price discovery’ that ultimately brings Citizens Bank to fair value. They are actively taking advantage of the severe mispricing of their stock and rewarding current shareholders with excellent capital allocation decisions.

It has been exciting to see how shareholder friendly Cynthia and her team are. Yet, the company remains at least 100% undervalued. Citizens Bank should generate ~$15+m of net income per year going forward in a no growth scenario which represents a 20+% free cash flow to equity yield – 5 P/E ratio. Additionally, Citizens Bank still has over $100m of cash – more than their entire market cap – at their holding company, creating an investment opportunity where even in the worst-case scenario it seems we would receive more than the current market cap.

To illustrate how undervalued Citizens Bank is and how beneficial share buybacks are at these prices, let us assume that over the next five years Citizens Bank continues to buy back $8+m per year of shares at current valuations. If we conservatively project that earnings remain flat at $15m per year, in five years Citizens Banks will be generating a ~50% free cash flow to equity yield – 2 P/E ratio!

Overall, Cynthia and her team have executed a wonderful balance of returning capital to shareholders, continuing to conservatively grow their loan book during these uncertain economic times while remaining one of the lowest cost depositors in the U.S – currently ~.52%.

BankFirst (OTCQX:BFCC) is a community bank located in Columbus, Mississippi. It is our eighth largest position in the fund and now has a market cap of $180m.

In October, I had a great catch up with CEO Moak Griffin and CFO Luke Yeatman. Their top-notch capital allocation plan to grow the bank from its current $2.7 billion in assets to $5.0 billion over the next few years remains on target. In 2022, when BankFirst received $175m in ECIP funds, they rapidly used their clever acquisition team to purchase three community banks in one year – before the rest of the ECIP community banking industry could even digest how to use their new capital.

BankFirst now has ~50m+ of cash remaining – in part due to their brilliant acquisition of Mechanics Bank that had an additional $42.5m of ECIP funds – to buy one more bank, which should bring their assets to ~$3.2 billion. After they have used all of their ECIP funds for acquisitions, their next step will most likely be to uplist onto the NASDAQ. After the uplisting, their ideal scenario would be to acquire one or two larger banks -$1-$2 billion assets. This would get BankFirst to their targeted $5 billion in assets over the next few years. I would not be surprised if one or two of these acquisitions complement their expansion in the Birmingham and Huntsville areas.

One impediment to an acquisition strategy of this magnitude is it would require them to use their shares as currency – which are extremely undervalued right now.

So why are their shares so undervalued?

First off, roughly 80% of BankFirst’s loans are fixed rate loans as that is the preference of their rural borrowers in Mississippi and West Alabama. This creates a short-term headwind to earnings as the fixed loans written in 2022 and before bear an interest rate of 4-6% while cost of deposits continue to increase – 1.3% at the end of Q3 2023 and continuing to rise each month.

For a few quarters this will compress their net interest margin and slightly decrease earnings to below $30m per year – creating the ‘optically’ lower accounting earnings mentioned. However, as the old, fixed loans mature they will recycle that cash into new, attractive fixed loans at 8+% interest rates – meaning they will remain on track to earn $33-$35+m per year. This represents a 17-20+% free cash flow to equity yield – 5-6 P/E.

That being said, the vast majority of the reason BankFirst is undervalued is likely because it is a small, undiscovered company where very few investors understand the astute capital allocation history of Moak and Luke. Once they uplist onto the NASDAQ, hopefully more investors will pay attention to the BankFirst story, causing a ‘price discovery’ that brings the bank closer to fair value – allowing them to use their shares as currency in a major acquisition. If not, Moak and Luke are fully prepared to buy back shares until fair value is realized.

In truth, no acquisition strategy going forward even needs to unfold for us to generate an adequate return. However, without future acquisitions, BankFirst will probably never experience 10+% per year loan growth – seen at times in community banks in more populated areas. Yet, under a no future acquisition scenario, they will continue to generate a steady 6-7% organic loan growth in rural areas that seldom experience the dangerous boom and bust cycles. This prudent loan growth alongside a best-in-class management team with a significantly undervalued share price – 55% of ECIP adjusted book value – gives us abundant downside protection even in a no growth scenario.

M&F Bank (OTCPK:MFBP) is a community bank in Durham, North Carolina. It is our fourteenth largest position in the fund and now has a market cap of $30m.

In December, I re-connected with CEO James Sills. James has a phenomenal reputation throughout the community banking industry, but he is faced with the challenging prospect of growing M&F Bank from its subscale position of a ~$450m asset bank to $1+ billion asset bank over the next few years. Due to their 2022 ECIP funding, M&F Bank still has ~$75+m in cash – 2.5x their current market cap – meaning the company has more than enough liquidity to grow to a $1+ billion asset bank.

The question is: can they get there through organic growth alone?

James has said they’ve looked hard for an acquisition that could get them closer to $1 billion in assets, but they have yet to find anything attractive. For now, they are focusing on growing organically in Charolette, Raleigh and Durham. They currently only have one branch in Charolette, so they have significant room to grow in the area and are doubling down on their efforts. Nonetheless, he said that to get to $1 billion in assets organically it is going to take an expansion into even more areas of North Carolina. Even if M&F Bank is unable to achieve any organic growth, they should be able to generate ~$5+m in earnings per year, which represents a 17+% free cash flow to equity yield – 5-6 P/E ratio.

At such a depressed valuation, it makes perfect sense to use their cash – $10m+ – over the next few years to buy back shares – increasing their dividend doesn’t make economic sense due to their variable preferred equity terms. Using similar math as we did with Citizens Bank, through ~$10m of share buybacks, M&F Bank could increase their free cash flow to equity yield to ~30+% – 3 P/E ratio – and still have enough cash left to organically grow to $1 billion in assets!

I have expressed this directly to James that even though M&F Bank is unable to find a bank to acquire right now perhaps it makes sense to “acquire” – via share buybacks – more ownership in your bank at current valuations of ~5x earnings and 35% of ECIP adjusted book value.

This is starting to sound repetitive, but similar to our other two ECIP community banks: no growth is necessary for us to achieve a reasonable return.

However, eventually James and the M&F Bank team will have to start to either capitalize on the undervaluation of their stock by buying back shares or make noticeable developments in growing towards $1 billion in assets. If not, there is a risk that M&F Bank will remain significantly undervalued for years to come. James is a veteran of the community banking industry and a wonderful leader; I feel confident he will find a way to beneficially allocate their $75+m of cash to increase equity value for us shareholders.

Nicholas Financial (NICK) is a sub-prime auto lender that is now being liquidated. It is our second largest position in the fund and now has a market cap of $50m.

In November, Nicholas Financial announced it had sold its entire sub-prime loan book to Westlake Financial for ~$65m – $9 per share. In early 2023, we bought ownership in Nicholas Financial at a $39m market cap valuation. If you go back to the H1 2023 letter, the assumption was that receiving $60m of cash from their liquidation over the next two years was our downside protection.

This turned out to be a fairly accurate forecast.

However, it wasn’t until I spent time in November with Nicholas Financial CFO Irina Nashtatik that I realized what an amazing job Adam Peterson and the Nicholas Financial team did in negotiating a $9 per share deal. Recall that Nicholas Financial outsourced the collection of their liquidating loan book to Westlake Financial at the beginning of 2023. The coinciding of tumultuous economic times – that have disproportionately hurt sub-prime borrowers – alongside the outsource model not transitioning nearly as well as planned caused Q3 2023 to be one of the worst loan write downs in Nicholas Financial history!

Adam and the Nicholas team urgently began to look for quick solutions and they were able to agree to sell their loan book to Westlake for $65m – 71% of gross receivables. Given the degradation of the loan book, this turned out to be a very shrewd and shareholder friendly decision by Adam Peterson and the Nicholas team. Not only was it highly unlikely that Nicholas Financial was going to receive $65m if they let their loan book naturally liquidate over the next two years, but the company was able to collect the entirety of the cash now versus over a two-year duration.

So, step one – getting $60+m of cash from the liquidation – of our Nicholas Financial investment thesis has been completed quicker than expected.

Now, the second step of the investment thesis begins – how will Adam and his team allocate the $65m of cash going forward?

Our preference would be for them to return the cash to shareholders immediately following the closing of the deal in the next few months. Nevertheless, it seems that Adam and his team have other plans as they want to utilize their tax shielding NOL’s – net operating losses – on the balance sheet (~$54m state and $31m federal NOL’s). Having talked to Adam and his team – who own 35+% of the shares – and watching them allocate capital over the years, I feel confident they will find a clever way invest the ~$65m of cash.

It seems as though it will be an investment in real estate or a similar asset. Perhaps even an asset that eventually becomes involved with Boston Omaha (BOC) – our third largest position – which Adam is the Co-CEO of. Our decision now is whether to sell shares at a market cap of $50m or remain invested in Nicholas Financial at a 30% discount to the $65m of cash on the balance sheet.

I am eagerly awaiting to see how Adam and his team plan to allocate the capital and if the potential returns outweigh the burdensome costs of operating a small, public company. Either way, our investment in Nicholas Financial has been the “heads I win, tails I don’t lose much” scenario laid out in the previous letter. Even in a downside case, it looks like we will generate a 30+% return.

Boston Omaha (BOC) is a holding company that divides itself into four main segments: Billboard, Insurance, Broadband and Asset Management. It is our third largest position in the fund and now has a market cap of $495m.

Earlier this year, I went to the Boston Omaha shareholder meeting where I was able to briefly catch up with co-CEO’s Adam Peterson and Alex Rozek as well as connect with a few of their key team members. Over the past few years, I have also spent time with Gary Solomon – Chairman of Crescent Bank, Tal Keinan – CEO of Sky Harbour, and Ben Elkins – CEO of Airebeam. Each of their companies are backed by Boston Omaha. Not only are all three impressive individuals who are top of class in their industry but what truly amazed me is they each had almost identical feedback on their wonderful partnership with Adam and Alex.

Each commented on how brilliant Adam and Alex are at allocating capital with a long-term vision – 20+ years – as well as how hands off they are – allowing each CEO to autonomously run their individual company. Whether at the Boston Omaha annual meetings or getting to know someone affiliated with the company, you can just feel the distinct, first-class culture Adam and Alex have created. Although it may take a while for investors to discover Boston Omaha, the team, culture, and groundwork have largely already been laid out.

Now onto their performance over the past six months

The billboard business is still the core of Boston Omaha as they have invested $200+m of capital into this segment since 2015. It is the sixth largest billboard company in the U.S. However, as mentioned in the last letter, Adam and Alex’s attention currently seems laser focused on growing their rural fiber internet companies. After talking with Ben Elkins – CEO of rural internet provider Airebeam – he reiterated what a pivotal time this is for the rural fiber internet industry.

The U.S government has dedicated $60+ billion to help fund ‘underserved’ internet areas throughout the United States as they have deemed it a necessity for every U.S citizen to have high speed internet. An ‘underserved’ area is a where the internet speed is below the high-speed threshold. These areas are often located in rural or small-town locations that still often run on dial-up internet or DSL. In these ‘underserved’ areas, the U.S. government will heavily subsidize the build out of fiber internet – which is substantially faster than even cable internet.

The key is for the rural internet companies Boston Omaha owns – Airebeam, Infowest, Ubb, and Fiber Fast Homes – to move fast, win government contracts and dominate their rural, fiber internet markets. Once fiber is built into a sparsely populated area it makes very little economic sense for a competitor to build there – a true ‘first mover’ advantage. This is why Boston Omaha is on pace to spend $75+m in 2023 towards expanding their fiber internet businesses’ footprint – $37.5m coming from raising equity (at an average share price of ~$24.50 per share) and the rest from free cash flow generated at their other business segments.

Although the holding company structure of Boston Omaha has been beneficial in that they can allocate capital from their other cash flowing companies into their high growth rural fiber internet businesses, it makes it very challenging for investors to value the company. Boston Omaha’s market cap has declined to $495m – a ~40% decrease since the beginning of the year – despite nothing material changing over the past year. If anything, there has been more good news than bad! Their depressed share price may partially be due to macroeconomic fears but no doubt some of the volatility is due to the difficulty of valuing the company.

Before we ascribe a valuation to their three core business – Billboard, Broadband and Insurance – let’s start with their fourth division – Asset Management. This segment alone consists of seven companies that have a valuation of ~$160m – 33% of their total market cap. Sky Harbour – a private aviation hangar company run by Tal Keinan – is the largest company in the Asset Management division and Boston Omaha’s equity stake in the company is worth $100+m. (Detailed in our H2 2022 letter)

Sky Harbour CEO Tal Keinan and his team have had a transformative year by raising ~$58m in equity and increasing their footprint to nine airports – a few of which I have personally visited and are beautiful facilities. They are well on their way to the short-term target of being in twenty airports. If we apply a $160m valuation for Boston Omaha’s Asset Management division and then use the historical costs of their Billboard, Broadband and Insurance companies, then Boston Omaha is currently trading at ~80-85% of book value.

The historical cost, especially for their Billboard business, is well below fair value. On a $495m market cap, Boston Omaha generates an 8-10% free cash flow to equity yield – 10-13 P/E ratio. This valuation may seem appropriate – especially considering the often applied holding company discount – until you spend time understanding the complexities of each company they own.

For essentially every company, we are in the early innings of development where they have already invested the upfront capital needed – $550+m in total – but the businesses have yet to mature. Eventually, as Boston Omaha’s companies start to mature, their earnings will continue to grow yet material growth capital will no longer be required. Over the years, they should develop into a free cash flow machine as their three largest investment –

Billboards, Broadband and Sky Harbour – require intense upfront capital (which has already been largely paid for) and little maintenance capital once maturity is reached. We have used the current undervaluation to increase our ownership in Boston Omaha. Being able to invest at below book value in two early 40’s, top-notch capital allocators who have laid the foundation, culture, and strategic plan for multiple decades of success is a rare occurrence. We are very lucky to have Adam and Alex investing our capital for years to come.

Logan Ridge Financial (LRFC) is a BDC (Business Development Company) that provides financing to small and midsize private companies in the form of either debt or equity. This is an option of financing for those companies that outgrow their local bank but aren’t big enough for Wall Street or larger banks. It is our fourth largest position in the fund and now has a market cap of $60m.

Over the past six months, BC Partners’ turnaround of Logan Ridge has continued to develop positively. Of the six bullets of improvements BC Partners’ outlined when they took over the company in 2021 (listed in the H1 2023 letter), they are now nearly 100% complete. All that remains is continuing to decrease their equity investments (which have gone from ~28% of the portfolio when BC Partners took over to ~17% ) and keeping up their dividend growth (which has gone from a 0% dividend yield when BC Partners took over to ~5% – not including repurchased shares).

The last major step is merging Logan Ridge into BC Partners’ main BDC – Portman Ridge – which is also run by Logan Ridge CEO Ted Goldthorpe and his team. I caught up again with Ted in September and he reiterated the positive trajectory of business and that the desired outcome still remains to have Logan Ridge merge with Portman Ridge. Only a month or so after our conversation, the largest shareholder of Logan Ridge and eighth largest shareholder of Portman Ridge – Punch and Associates – sent out a ‘suggestivist letter’ to Ted and his team (attached here – Exhibit 7.2).

The letter addresses the exact concerns myself and all other major shareholders I’ve spoken with have expressed as well. Highlighting that Logan Ridge is subscale, and the required overhead costs are too burdensome for a standalone BDC with ~$100m in assets. No matter how much BC Partners’ re-shapes the loan portfolio, generating adequate returns is too difficult at their current size. The only way for Logan Ridge to get to a proper valuation – they are currently trading at 60% of Net Asset Value – is to increase in size via a merger with Portman Ridge which needs to happen in the near future.

The letter goes on to explain that not only does this make sense for Logan Ridge, but it makes sense for Portman Ridge as well. Upon acquiring Logan Ridge, Portman Ridge would be able to get rid of ~$4m of Logan Ridge’s overhead redundant costs as both the companies are run by the same BC Partners team. Furthermore, Portman Ridge itself needs to grow to reach adequate scale and the addition of $100m of assets that the management team intimately knows is a no-brainer way to expand their stagnant portfolio.

The letter perfectly lays out the argument on how the combined entity would increase Net Asset Value per share for all those involved. After the letter was released, I spoke with Punch and Associates. It is fantastic news for us that they have gotten publicly involved as they are very sensible investors. Ted and his team have been wonderful stewards of our capital and I have little doubt that they are ultimately going to get the Portman Ridge deal done regardless. However, Punch and Associates being involved almost certainly pushes the timetable of the deal forward.

Portman Ridge shareholders have been hesitant for the deal to go across and have been waiting for Logan Ridge to further decrease their equity exposure and increase their dividend. Hopefully, the Punch and Associates letter will help Ted and his team convince Portman Ridge shareholders that the benefits of adding scale and increasing NAV per share outweigh waiting for Logan Ridge to continue to improve. If the merger does go through in the next 6-12 months, Logan Ridge shareholders will receive shares in Portman Ridge.

Without going into the math specifics of the deal, we would most likely receive a 17+% dividend yield through the combined entity and still have Ted and his team wisely allocating capital for us. In a downside scenario, where the deal doesn’t go through, Logan Ridge will remain a standalone company. We will have ownership in a BDC that is undervalued – 60% of NAV – that will continue to increase the dividend to an 8-10% yield while buying back shares at a depressed valuation. This is an investment set up I have often talked about where “Head we win, tails we don’t lose much.”

R&R REIT (RRR.UN) is a REIT (Real Estate Investment Trust) that owns 17 budget hotels – Red Roof Inns and Hometowne Studios – throughout the U.S. It is our fifth largest position in the fund and now has a $25m market cap.

This history of R&R REIT was outlined in the last letter but recall that Majid Mangalji – billionaire hotel entrepreneur who sold a REIT in 2016 for over $1 billion – alongside the rest of the R&R management team own 93% of R&R REIT’s equity. The fact that a best-in-class real estate investor is heavily aligned with us in wanting to create as much equity value as possible in R&R REIT is no doubt a positive. However, Majid and the rest of the R&R REIT team owning 93% of a $25m market cap company means that very few shares trade on the stock market.

On average less than $20,000 worth of shares trade per day, making the stock price incredibly volatile if an investor is eagerly buying or selling. Over the past six months, R&R REIT’s equity value has fluctuated nearly 100% in between a market cap of $19m ($0.09 CAD per share) to $36m ($0.17 CAD per share). We have taken advantage of this volatility by continuing to increase our ownership in R&R whenever the price rapidly falls. Our average purchase price has been below $0.13 CAD per share.

Recall, every time Majid Mangali has sold a hotel to R&R REIT in exchange for equity in the company, he has done so at a $0.20 CAD per share valuation. So, over the past six months due to the low liquidity and underfollowed nature of R&R REIT, we have been able to increase our ownership at a price 65+% below what an expert real estate investor feels is fair value. After digging deeper, even $0.20 CAD per share is most likely too low of an estimate for fair value. A 2019 asset appraisal of R&R REIT valued the company at $0.33 CAD per share.

Using more traditional real estate valuation metrics, we are able to buy R&R REIT at a 16+ cap rate and 17+% free cash flow to equity yield – 5-6 P/E ratio. While talking with management, they made it clear the future plan is to use the $10+m of cash on the balance sheet and $15m+ of debt capacity to opportunistically acquire hotels that are under distress due to rising interest rates. Right now, our estimated fair value for R&R REIT is $0.25-$0.33 CAD per share and that is using the assumption that Majid and his team add no value with their acquisition strategy.

If over the next few years, Majid and his team can significantly grow R&R REIT – as they did with their previous REIT – our upside potential on this company is hard to even quantify. R&R REIT appears to be a classic example of a $0.50 on the dollar investment. Regardless, I will continue to check in with management and monitor how they are allocating their $4.5-$5.0m of free cash flow per year to ensure our equity value is growing even if R&R REIT remains significantly undervalued.

Fitlife Brands (FTLF) develops and markets nutritional supplements – protein powders, pre-workout, amino acids, weight loss products, fish oils etc. – under 13 different brand names. It is our seventh largest position in the fund and now has a market cap of $90m. Through CEO Dayton Judd’s innovative capital allocation decisions since taking over in 2018, he has turned a near bankrupt company that sells commodity branded products into a wonderful business. Each step of Dayton’s remarkable turnaround from 2018 to H1 2023 was highlighted in the last letter.

I recently caught up with Dayton – who owns 55% of the company – and unsurprisingly the continued progress of Fitlife hasn’t subsided, as he yet again made two brilliant strategic decisions in the second half of 2023. First, in September, Fitlife uplisted their shares from over-the-counter markets to the NASDAQ exchange. Although the company has only been listed on the NASDAQ for a few months, their volume of shares traded has increased 5x , they have been added to two index funds, and there seems to be more chatter about Fitlife.

Then, in October, Fitlife acquired the MusclePharm brand for $18.5m which has more upside potential than any brand Dayton has ever acquired. MusclePharm is a well-known sports nutrition brand that was started 15 years ago and eventually grew to over $150m in revenue. In the past, they have had major celebrity endorsers such as Arnold Schwarzenegger and Tiger Woods.

In late 2022, MusclePharm filed for bankruptcy after continuously experiencing numerous operational, legal, and financial troubles. Similar to when Dayton acquired Mimi’s out of bankruptcy in December of 2022, he had been keeping a close eye on MusclePharm for years as he knew they were in financial trouble. His patience and ability to acquire top-notch yet distressed brands at the lowest possible price has been truly incredible to watch.

As MusclePharm started to experience troubles in the past few years, many of their major domestic retailers – Costco, iHerb.com, Walmart, GNC, Vitamin shoppe, and others – either stopped carrying their brand or held very limited inventory. Dayton has outlined that step one of the turnaround is to re-develop MusclePharm’s relationship with the major domestic retailers who have a sour taste from how the brand was previously run. This turnaround is already starting as one of their major e-commerce sites has re-listed MusclePharm’s products back on their site and will start selling their products in early 2024.

Secondly, Dayton plans to continue to grow MusclePharm’s already strong international sales – which will help diversify Fitlife’s U.S concentrated revenue.

Finally, and most excitingly, Dayton plans on using Fitlife’s online sales expertise to sell MusclePharm’s products direct to consumers – mainly on their own website and Amazon. It appears Dayton only paid an estimated 6-7x free cash flow to equity for MusclePharm. However, that isn’t factoring in that Musclepharm dropped from $150+m in sales in 2015 to below $20m in sales by 2022.

If Dayton can execute another turnaround strategy – which he has flawlessly done multiple times since 2018 – and even just doubles MusclePharm’s 2022 revenues alongside increasing margins, this acquisition could be enormous for shareholder value. MusclePharm seems to be the last major acquisition Fitlife will make in the short term. Dayton will now focus on fully integrating Mimi’s and MusclePharm into the Fitlife family of brands.

Over the next year as this implementation process starts to bear fruit, Fitlife should generate 12+m of free cash flow which represents a ~13+% free cash flow to equity yield – 8 P/E ratio. Free cash flow should continue to rapidly grow as Dayton continues to increase gross margins with his direct-to- consumer e-commerce plan alongside his impeccable ability to reduce overhead costs.

The turnaround Dayton continues to execute at Fitlife is nothing short of amazing! The company has gone from near bankruptcy when he took over in 2018 to close to a $100m business. We are incredibly fortunate to have Dayton allocating capital for us and it won’t be long until more and more investors start to discover that he is a best-in-class operator.

Galaxy Gaming (OTCQB:GLXZ) licenses proprietary tables games to casinos – most notably ’21+3.’ It is our ninth largest position in the fund and now has a market cap of $45m. Since our fund started in 2020, Galaxy Gaming has been the most disappointing investment I have made thus far as their team continues to get in the way of a wonderful business by making short-term minded, often nonsensical decisions.

This problem started long before we were investors in the company. But once former CEO Todd Cravens took over for Galaxy Gaming’s founder – who had to step away from the company in 2018 due to nefarious business activities that almost caused Galaxy Gaming to lose their gambling license – I thought the company’s problematic days were finally behind them. As we invested in 2021, I flew out to Las Vegas to visit with Todd and the Galaxy Gaming team. My takeaway from the meeting was that Galaxy Gaming was Todd’s company to run and he was the main decision maker.

Todd navigated Galaxy Gaming through Covid quite well, was constantly finding innovative acquisitions, and most importantly developed a strong relationship with Evolution Gaming to help grow their iGaming business. This past year was progressing very nicely as Galaxy Gaming signed a 10-year contract with Evolution Gaming, hired key employees to increase ‘bench strength’ and structured a very creative deal to acquire the EZ Baccarat table game. No doubt there were hiccups along the way since we invested in 2021. Most notably, their poor implementation of the previous gaming operating system, not hedging their variable debt, and not investing their excess cash into the money market.

However, Todd had Galaxy Gaming trending in the right direction by continuously generating 15+% revenue growth per year and bringing much needed stability to a company that had been on a rollercoaster ride for years. It felt as though 2024 was going to be Galaxy Gaming’s best year so far and their strategy to bring ‘gamification’ – slot machine type activity – to felt games seems to have created another niche market they can dominate. Then, in September, the board of directors decided to fire Todd out of nowhere.

This was a shock to all outsider shareholders, me included, and the press release of the announcement was handled very poorly. I had spent time with Todd in May, and he really seemed to have full control of the company and finally settled into his role as CEO for the long term. I briefly spoke with Todd after he was let go, and it was no doubt a shock to him.

When we first invested in Galaxy Gaming, I deceived myself into thinking it checked off all six bullet points we look for in a wonderful business. I inaccurately checked off the bullet point “Is run by honest and able people that also have ownership in the business.”

The mistake here was twofold.

First, Todd is honest and able, and I thought it was his company to run. Apparently, the board of directors had much more power than I realized and not only were they misaligned with outside shareholders, but they had a poor relationship with the CEO.

Secondly, prior to a modified compensation structure, the board of directors had too liberally given themselves shares in Galaxy Gaming in exchange for being on the board. In hindsight, this was a red flag I overlooked as almost all their ownership was gifted to themselves – except for one outsider -and not bought with their hard earn money. They don’t truly have skin in the game.

Nonetheless, the board’s decision to fire Todd is yet again another example of the Galaxy Gaming team getting in the way of a wonderful business. Since the announcement, the market cap of the company has gone down ~35%. Although this is no doubt bad news, I think the one silver lining is Galaxy Gaming is now ripe for a major change. The board members who made this erratic decision only own ~20% of the company and the chairman of the board is coming up for re-election this annual meeting.

Galaxy Gaming has ~$54m in debt – from buying out their founder – with a variable interest rate now at ~13% – $7m of cash per year. This means nearly all their $8-$10+m of free cash flow before taxes is used to pay interest. However, if a strategic acquirer were to buy Galaxy Gaming, they could take out $12+m of redundant costs, use the ~$16m of cash on the balance sheet to pay down debt, and refinance the remaining debt with the acquirer’s superior credit rating – reducing interest expenses to $2.5-3.0m per year.

This translates into a strategic acquirer being able to generate $18m+ of free cash flow before taxes – including ~$6+m which is guaranteed for 10 years in the Evolution Gaming contract. Depending on the growth prospects determined by a strategic acquirer, I assume they would be willing to pay a $175+m market cap- over 3x the current price.

There are a lot of “ifs” in those statements, and we will be closely monitoring Galaxy Gaming over the next six months. Unless there is a drastic change in leadership, Galaxy Gaming will no longer complete our six-point checklist and we will most likely need to move on.

(See ‘Biggest Mistake’ section for further discussion)

Legacy Housing (LEGH) builds and finances manufactured homes. It is our tenth largest position in the fund and now has a market cap of $580m. In October, I went to the Legacy Housing Home Show where the company displayed its new manufactured home styles to dealers. Afterwards I was able to attend the annual dinner where I spent time with the two co-founders Curt Hodgson and Kenny Shipley as well as CEO Duncan Bates and some of their new team members.

Since being hired as CEO less than two years ago, Duncan has made amazing progress. He has done a fantastic job at professionalizing the business, improving investor relations, and continuing to hire top tier talent. Their most recent hire was CFO Jeff Fiedelman in September. I spoke with him at the annual dinner, and he seemed like a perfect fit for their team – all the other Legacy Housing team members spoke very highly of him as well. Jeff seems to be the last major piece needed to complete a well-rounded, top- notch team going forward.

Make no mistake about it, the underlying business has been exceptional since Curt and Kenny founded it in 2006. However, Duncan has implemented the necessary adjustments needed to seamlessly run a public company while still allowing Curt and Kenny’s entrepreneurial instincts to continue to innovate the company faster than competitors.

The next area where Curt and Kenny’s industry expertise should flourish is at the one thousand acres of land they own in Austin, Dallas, and San Antonio.

Manufactured Housing Parks – subdivisions with tens to hundreds of manufactured homes – have attracted the attention of many investment funds. Curt, Kenny, and the Legacy team are in the process of finding a creative way to use their one thousand acres of land to capitalize on this new Manufactured Housing Park wave.

If history repeats itself, Legacy Housing will find a way to remain one step ahead of the market and use their acreage to creatively grow both their manufactured homes sales and lending. Currently, despite the manufacturing housing industry temporarily declining compared to 2022, Legacy Housing currently offers investors a ~10-11% free cash flow to equity yield – 9-10 P/E ratio.

As the Legacy Housing team is able to turnaround the Georgia plant, monetize their one thousand acres of land, grow their loan book, prudently increase debt, and perhaps acquire a small manufacturing business, it would not be a surprise to see them continue to grow the equity value of the company at the historical rate of 15+% per year.

America’s Car Mart (CRMT) is a deep sub-prime auto lender and car dealership. It is our eleventh largest position in the fund and now has a $450m market cap. In September, it was announced that Jeff Williams will retire as CEO and Doug Campbell will be his replacement. Jeff has done an incredible job since taking over the company in 2018 with their book value increasing over 100%.

Jeff will remain on the board and help Doug in his transition to CEO. I have yet to meet Doug, but I plan on scheduling a trip to Arkansas soon! When I met with Jeff and CFO Vickie Judy and talked over the phone with America’s Car Mart board members, they all spoke very highly of Doug. His prior background at Avis and AutoNation makes him well equipped for America’s Car Mart’s transition of centralizing their car purchase operations. This will allow dealership managers to concentrate solely on increasing the number of cars sold per dealership – with a short-term goal of increasing the average from 33 per month to 40.

Since the pandemic, the sub-prime auto lending industry has become increasingly more difficult as used car prices have skyrocketed by over 50%. To make ends meet, America’s Car Mart had to extend their loans from ~30 months to ~44 months creating more credit risk within the business. Additionally, over the past year with increasing interest rates, a tough economy for deep sub-prime borrowers and no more COVID stimulus money, the subprime auto industry is in a tumultuous period.

Although this has the potential to create short-term pain for America’s Car Mart, in the long run this should be a net positive as it wards off any potential new entrants and puts financial strain on their current competitors. Recall that the deep subprime auto industry is very fragmented and mainly run by mom-and-pop stores that thrive during booming times but during tough economic times are unable to compete against America’s Car Mart’s low cost 154 store franchise.

During these tough times, America’s Car Mart has historically capitalized by acquiring mom and pops stores. In fact, in December, they bought a mom-and-pop dealership in Hot Springs, Arkansas. River Oaks Capital will continue to monitor the growing duration of their loan book and any risk it may pose if deep subprime auto market conditions get worse. Nevertheless, we own a conservatively financed, low cost deep subprime auto dealer that is well positioned to consistently gain market share over the next 5-10 years regardless of economic conditions.

When I met former CEO Jeff Williams, he re-iterated to me that America’s Car Mart has gotten very little benefit out of being a publicly traded company, as the share price is so volatile while their capital allocation plans are in 5-10-year periods. The volatility of their stock has again made the company valued at ~85-90% of book value – 10-15% below where the company would most likely be sold in a fire sale scenario. Whether Dan, Vickie and the America’s Car Mart team decide to use this as a time to buy back their undervalued shares or allocate capital towards gaining market share, we are fortunate to be investing alongside such a wonderful team who makes each decision with the long-term shareholders best interest in mind.

Greenfirst Forest Products (GFP.V) – (numbers are in $USD)– owns and operates four lumber mills in the Ontario providence of Canada. It is our twelfth largest position in the fund and now has a market cap of $125m. Since starting Greenfirst in 2021, Paul Rivett – former Fairfax president – and his team have rapidly sold ~$110m of non-core assets, reduced net debt from $70+m to below $12m, cut corporate overhead expenses, turned around the papermill and continue to assemble a highly qualified management team.

In November, Joel Fournier was hired as CEO. Joel has an extensive background in the Canadian lumber industry and a resume well suited for running Greenfirst. Paul Rivett – who was serving as interim CEO – will remain head of the board of directors and continue to make the major capital allocation decisions while Joel runs the day-to-day operations of the business.

In the third quarter, Greenfirst was roughly breakeven as lumber prices were in the $500-$550 Mfbm range. Over an entire lumber commodity cycle, if prices are to average ~$550-$600+ Mfbm, Greenfirst should be able generate an average of $15-$20+m of free cash flow to equity per year – which represents a 10- 13+% (8-10 P/E ratio). This is not an unreasonable assumption for average lumber prices, but it requires us to do the impossible of predicting: 1) commodity prices and 2) how long a commodity cycle will last.

However, what makes Greenfirst such a unique investment is the misunderstood downside protection. As mentioned in prior letters, Canadian lumber companies must pay duties to the U.S government whenever they sell lumber into the U.S. The U.S government collects these duties and lets them accumulate for years until a settlement is made between the U.S and Canada. Upon settlement, a certain percentage of the duties are returned to the Canadian lumber companies. The last decision, in 2006, returned 80% of the duties to Canadian lumber companies.

Right now, Greenfirst has ~$73m of duties on deposit. It is highly probable that a large percentage of the duties will be returned but it is unknown when that will be. In November 2021 – when Interfor acquired Canadian lumber company EACOM – they valued their duties at .55 cents on the dollar. Using this assumption, Greenfirst’s duties are worth ~$40m. If we then factor in that they still have three valuable non-core real estate assets on the balance sheet, a ~$15m overfunded pension plan and $100+m of tax loss carryforward to shield gains, it is reasonable to assume that ~50+% of the market cap is in non-core assets.

On top of that, if we add in the ~$35m of net inventory less debt, you get close to the entire value of the market cap before you even factor in the four lumber mills and their forest land. If we use an overly conservative assumption that non-core assets are worthless, their four lumber mills in Ontario are valued well below ~$150 MMfbm. This is significantly below liquidation value and at a price that a large Canadian lumber company such as Interfor – which already owns 16% of Greenfirst – would almost certainly pay a significant premium above.

Paul and the Greenfirst team have masterfully executed their capital allocation plan laid out in 2021. One of the few remaining steps in their plan is to begin to return capital to shareholders, which should start sooner than later.

All Companies below 3% of our fund

We own three companies that are below 3% of the fund: BEBE’s, M&F Bank and Pharmchem. As usual, if these companies’ positions grow in size, I will provide a detailed write-up (there is one in the section above on M&F Bank). If you are interested in learning more about these companies now, please feel free to give me a call or I can e-mail you a write-up.

Companies sold over the past six months

None

Biggest mistake

I have already outlined my biggest mistake under ‘Galaxy Gaming’ in the section above. The error wasn’t a mis-assessment of the quality of the business. Galaxy Gaming’s underlying business remains what we look for in a small, underfollowed “wonderful business.” They dominate an obscure, niche market that is not large enough for it to make logical sense for a large corporation to spend the marketing and R&D dollars to enter. This off the radar market creates a ‘hidden moat’ where the business can generate durable, excess returns for many years.

Galaxy Gaming perfectly fit this criteria, so I was mistakenly willing to look past the fact that it did not fully check the third bullet point of our checklist: “Is run by honest and able people that also have ownership in the business.”

After meeting with former Galaxy CEO, Todd Cravens, multiple times I found him to be “honest and able” but in hindsight I knew the second part “also have ownership in the business” wasn’t truly fulfilled – especially by those on the board. Although the Galaxy team and board have ownership in the company it is almost all through stock options gifted to themselves. This is just not the same as buying ownership in a business with your hard- earned money.

I knew the importance of having at least one person – CEO, chairman of the board, founder, etc. – being a large shareholder when investing in a small, underfollowed company that often has very few eyeballs watching to make sure it is being run with all owner’s best interest in mind.

Yet, I overlooked this importance at Galaxy Gaming. No one on the board – expect one outsider – had real skin in the game. This caused a misalignment with long-term minded shareholders. Ultimately, the board made a knee-jerk, short-term decision to get rid of Todd as CEO which unnecessarily destabilized the prospects of the company.

This mistake is a learning experience I will use to better our funds’ performance going forward – ensuring all six bullet points are fully checked when investing in a “wonderful business” – but my decision to invest in Galaxy Gaming has hurt us in the short term.

Best,

Whit Huguley, CFA

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")