")

")

")

")

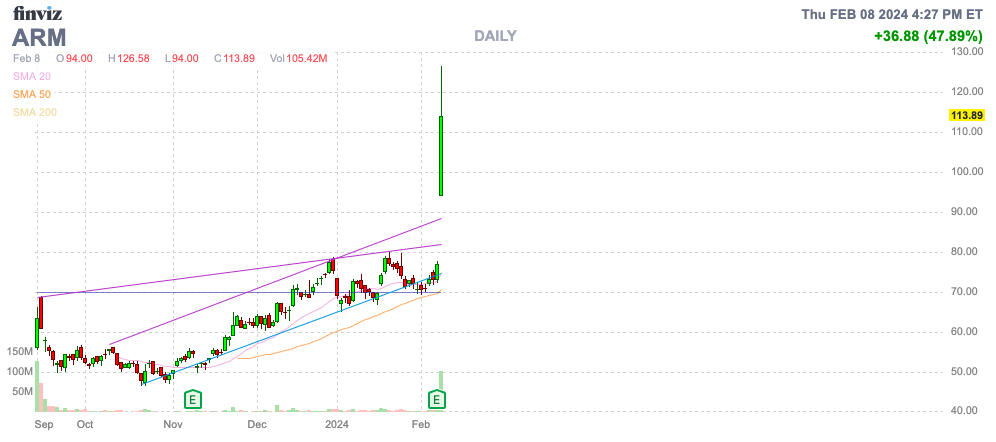

After a better than expected quarterly report, Arm Holdings plc (NASDAQ:ARM) soared nearly 50%. While the chip design company reported solid numbers with growing profits, the stock has mostly risen in the last few months due to multiple expansion, not growth. My investment thesis is ultra Bearish on the stock, as it is trading at levels not seen since the Internet bubble and a few select stocks during Covid peaks.

Source: Finviz

Misunderstood Bump

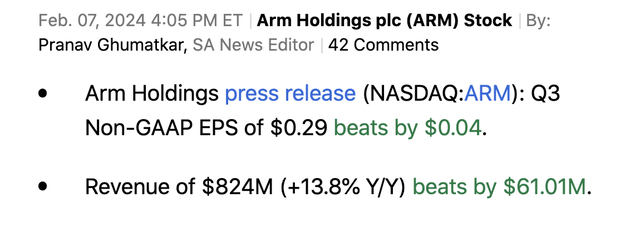

ARM reported solid FQ3 ’24 results after the close on February 7 as follows:

Source: Seeking Alpha

While the chip company smashed estimates, one needs to understand the business model of ARM. A large portion of the revenues are from upfront license deals, causing the lumpy quarterly revenues, where ARM can report a $61 million beat and only report 14% growth for the quarter.

One can easily argue that, if ARM had guided correctly, the market wouldn’t have been impressed with 14% growth with a small revenue beat. In addition, the chip company reported some other metrics that weren’t necessarily all that impressive, despite the stock surging over 50% for most of the following trading day:

- ARM based chips shipped in the September quarter declined to 7.7 billion, down from 7.9 billion.

- FQ3 growth was most isolated to double the royalty rate for the Armv9 technology.

- License revenue jumped 18%.

- Annualized Contract Value (“ACV”) only grew 15% YoY to $1.16 billion.

- Stock-based compensation (“SBC”) of $198 million was over 15% of total revenue.

The royalty revenues only grew $45 million YoY for 11% growth, but the contribution from the Armv9 technology jumped to 15% of revenues from 10% in just the prior quarter. At 15% of the $470 million in FQ3 royalty revenues, ARM generated $71 million from the Armv9 royalty, suggesting ~$35 million of the revenue boost was due to the double royalty rate compared to the older Armv8 technology.

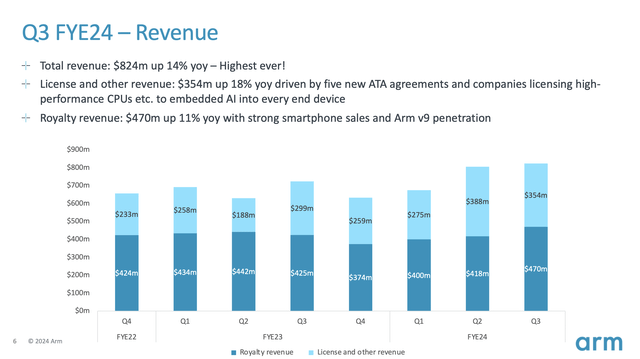

As discussed last quarter, the license revenue is very lumpy and difficult to predict. The majority of growth came from the license revenue jump in the quarter, with 5 new ATA agreements during the quarter. ARM now has over half of the top 20 customers under ATAs, limiting some of the upside from this revenue bucket, where deals contribute to sizable initial revenue values.

Source: ARM Holdings FQ3’24 presentation

These key license revenues were actually down from the FQ2 ’24 levels of $388 million. Again, revenues for the December quarter weren’t all that impressive, with total revenue only growing $18 million sequentially to $824 million.

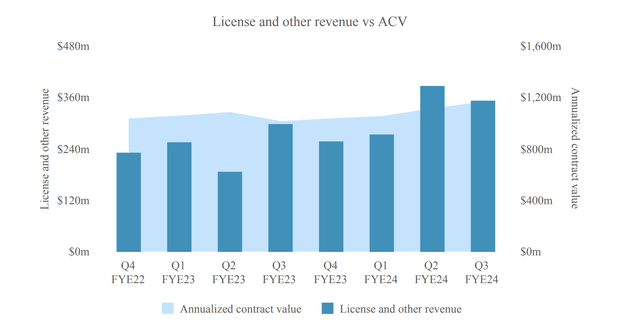

Ultimately, the ACV metric wasn’t supportive of any blowout AI demand. ARM is seeing strong AI demand, leading to solid expectations for growth in the years ahead, but the numbers probably aren’t much different from Taiwan Semiconductor (TSM).

As the below chart highlights, ACV hit $1.16 billion for only 15% growth.

Source: ARM Holdings FQ3’24 earnings release

On top of the lack of growth metrics that support the stock exuberance, ARM has a substantial amount of stock-based compensation. While I am not against SBC, the amount is excessive in the case of ARM and wipes out the majority of the $338 million in adjusted operating income. Strip out the $198 million in SBC, and operating income would only have been $140 million.

The company now has 1.05 billion shares outstanding, and a big reason the stock is surging is the lack of a float, with only 10% outstanding following the IPO. The combination of a low float and high SBC will ultimately contribute to massive pressure on the stock as large amounts of additional shares are dumped on the market.

ARM guided to FQ4 revenues in the range of $850 to $900 million, with consensus analyst estimates at $860 million for 36% growth. The March quarter growth looks impressive, but the prior FQ was very weak, with revenues slipping from the FQ4’22 levels of $657 million.

Multiple Expansion Won’t Last

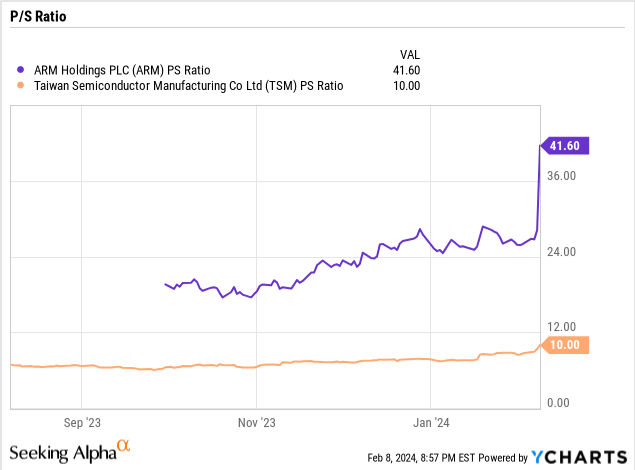

A prime example of the excessive exuberance in the stock market is ARM now trades at over 40 trailing sales and 37x targets for FY24. The company guided to revenues of $3.18 billion, and the stock now has a market cap of nearly $120 billion.

As the chart highlights, TSM only trades at 10x sales targets. The chip company has large capex spending, but the company generates similar massive operating margins in the 40% range. ARM only licenses the chip technology, while TSM or another chip manufacturer is still needed to produce the chips.

TSM only trades at 20x EPS targets of $6.27, while ARM now trades at ~100x the updated EPS targets for FY24 of $1.22. One can definitely understand the benefits of a license business with strong margins, but a premium valuation of 5x the leading chip producer is beyond excessive.

At the Covid peak when sales surged 100%, Zoom Video Communications (ZM) traded at over 40x sales targets when the stock topped over $500. Zoom stock has absolutely collapsed since sales growth slowed, and now the stock only trades at 4x forward sales targets.

Takeaway

The key investor takeaway is that Arm Holdings plc has a bright future due to AI chip demand and a shift to ARM-based chips. Though, the stock is currently vastly disconnected from the opportunity ahead, with ARM trading at multiples above a logical valuation that will ultimately fall into the 10x to 15x sales range.

Investors should use the current surge in the stock to exit ARM at the highs.

Read the full article here

")

")

")

")

")

")