")

")

")

")

Thesis

Kenvue Inc. (NYSE:KVUE) represents an ideal candidate for a low-risk income-producing strategy of writing covered calls to enhance the dividend. In a previous article, I discussed how the riskiness of the underlying investment changes covered call option choices.

The company operates in the highly stable Personal Care Products subsector of the economically low-sensitive Consumer Staples sector. Having spun out of Johnson & Johnson (JNJ) less than a year ago, I expect the company, which is profitable and owns well-known brands, to have modest growth and improving margins in the next few years.

The $0.80 per share annualized dividend currently yields close to 4%, and I expect the payout to grow over time. In addition, the Kenvue stock options’ value is elevated compared to similar companies. Selling covered calls with upside strikes thus adds to the total return that can be had from owning this investment.

Kenvue’s Revenue Stability

As a standalone business, KVUE Inc. is a premier over-the-counter consumer health product company with some of the best brand recognition in the world. It generates over $15B in revenues. Seven of the company’s brands, Tylenol, Nicorette, Zyrtec, Neutrogena, Listerine, Johnson’s, and Band-Aid, hold the #1 market share globally in their respective categories. Aveeno, Ogx, and Motrin round out KVUE Inc.’s top brands, each having over $400M in sales. Half of these revenues are generated in North America, while Asia Pacific (APAC) Europe, the Middle East, and Africa (EMEA) each accounted for 21% of 2022 sales, and Latin America represented about 8%.

The company reports sales across three segments: Self Care (40%) includes cough, cold and allergy, pain care, digestive health, smoking cessation, and other products. Skin Health and Beauty (29%) has face and body care, hair, and sun care products. Essential Health (31%) focuses on oral care, baby care, women’s health, and wound care.

According to Kenvue’s prospectus, from 2020 to 2022, net sales increased from $14.5 billion to $15.0 billion, representing a CAGR of 1.7%, which was impacted by the decision to reduce the number of stock-keeping units (“SKU’s”) by 21% through 2022. The company expects the total addressable consumer health market to continue expanding at a CAGR of 3% to 4% globally through 2025, driven by favorable demographic trends and an increasing focus on health and wellness.

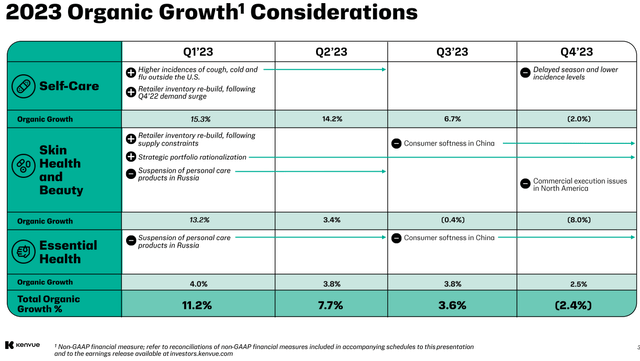

KVUE reported that full-year 2023 sales increased 3.3% to $15.4B. This included organic growth of 5.0% (7.7% price and product mix gains offset by 2.7% volume declines) and an unfavorable foreign exchange impact on reported sales of 1.7%. The volume decline accelerated to 8.2% in the year’s final quarter, driven by poor execution of the North America Skin Health and Beauty segment, lapping a strong 2022 early start of the cold and flu season, product discontinuations, and customer inventory destocking.

Kenvue Inc.

For 2024, the company gave an outlook for sales growth of 1.0% – 3.0%, with organic growth of 2.0% – 4.0% offset by continuing foreign currency headwinds of about 1%. Margins will be impacted by increasing costs associated with being a standalone public company, resulting in a forecast adjusted EPS of $1.10 – $1.20 for the year, down from the $1.29 earned in 2023. I guess that this may prove to be conservative guidance.

While the company has already begun rationalizing its product portfolio and concentrating on profitable growth, it will likely enhance this process and look for tuck-in acquisitions as a standalone entity.

Income Investing With KVUE Covered Calls

The company generated about $2.7B in free cash flow in 2023, more than adequate to cover the $1.5B annualized dividend payout. A full-year 2024 EPS of $1.10 – $1.20 implies strong coverage for the $.80 annual payout.

In addition to this dividend income, call options on KVUE stock are priced at an implied volatility (IV30) of about 27%. Compared to its competitors, this appears very elevated:

|

Option Implied Volatility |

|

| Proctor & Gamble (PG) | 11% |

| Kimberly-Clark (KMB) | 13% |

| Colgate-Palmolive (CL) | 13% |

| Unilever (UL) | 15% |

| Consumer Staples Select Sector SPD Fund (XLP) | 11% |

As a result, with the stock currently trading at about $19.95 per share, an investor can buy the stock and sell an upside March 15 $21.00 Call at $0.15 for a net cost of $19.80 as I am writing this. In addition, February 13 is the ex-dividend date to collect the current $0.20 dividend. Thus, if the stock trades up through the strike price, holders of KVUE could realize a total gain of $1.40 per share, or 7.0%, in just 36 days.

The $21.00 strike price is reasonable for it to trade up to, as this represents about 18.3x the company’s guidance and is within the range of competitors’ multiples.

Litigation Risks

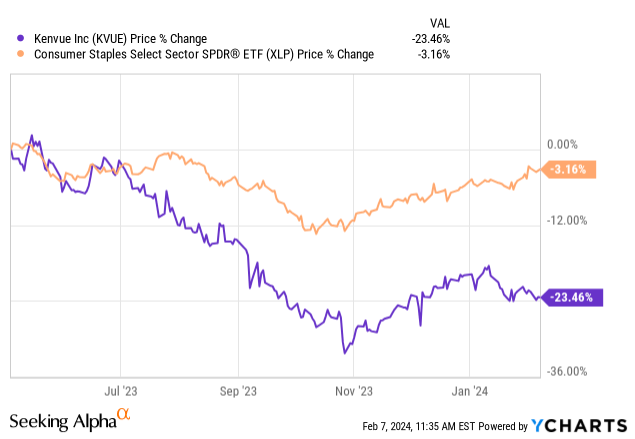

KVUE stock has performed poorly since its IPO despite the strength in the overall market. This likely reflects the preference of many investors for more significant growth and the belief that the economy is in for a “soft landing,” with no need to overweight the defensive consumer staple names.

However, as seen in the above chart, Kenvue has underperformed in the sector. What is surprising is that this has stayed the same despite positive developments in the litigation risks that the company faces, which I outline below.

Tylenol Class Action Suit

In October 2022, over 440 lawsuits were consolidated in a class action against the company, alleging that pregnant women’s use of Tylenol caused Autism and ADHD in children. In December 2023, U.S. District Judge Denise Cote granted Kenvue’s motion to exclude the plaintiff’s expert evidence, which failed to prove causation between exposure to acetaminophen, Tylenol’s active ingredient, and those childhood disorders.

CEO Thibaut Mongon commented on the 3Q23 earnings conference call:

FDA continues to maintain the same pregnancy advice on acetaminophen labels that has been in place for decades. This conclusion is based on multiple reviews since 2014 with the most recent being March 2023 that recent studies do not change FDA’s view on acetaminophen’s safety.

Indeed, in a Drug Safety Communication that is current as of January 2023 regarding NSAIDs and pregnancy after 20 weeks, the FDA states:

Other medicines, such as acetaminophen, are available to treat pain and fever during pregnancy. Talk to your pharmacist or health care professional for help deciding which might be best.

Kenvue has said that it will seek dismissal of the lawsuits based on the plaintiff’s lack of admissible evidence. Before the hearings and ruling on the evidence, analysts had predicted potential exposure to the company in the $3B to $10B range, which is significant to KVUE’s approximately $40B equity market capitalization.

Talc-Related Exposure

I hesitated even to mention this litigation since I do not believe it will be material to Kenvue’s financials. I only do so because other authors have pointed to this as a potentially significant risk to the company. Johnson & Johnson retained all liabilities related to the presence or exposure to talc and related products in the U.S. and Canada, primarily due to past sales of Johnson’s Baby Powder.

The company will remain liable for liabilities from talc-related products sold outside the U.S. and Canada. However, that will be a small fraction of the $12B that JNJ reserved to pay out over the next 25 years. The U.S. and Canada represented more than half of these sales and litigation costs in the rest of the world, but they are a fraction of those in North America.

It should also be noted that the formula for Johnson’s Baby Powder was switched from talc-based to cornstarch in 2020 in North America, and in 2023 this switch was completed for the rest of the world. The once iconic Johnson’s product had fallen to less than 0.5% of U.S. consumer product sales.

Conclusion

Full-year Kenvue Inc. 2023 earnings are out, and I am disappointed as investors will likely have to wait for the back half of 2024 to become comfortable with the growth and earnings story. If it does, the implied volatility will fall, bringing the call option prices down. However, as long as the implied volatility of this relatively stable company remains elevated, investors can continue to realize healthy annualized returns through its dividend payout and selling the relatively expensive call options against the position.

Read the full article here

")

")

")

")

")

")