")

")

")

")

")

After upgrading the stock in September, shares of FLEX LNG (NYSE:FLNG) have underperformed, down about -9%. With the stock taking a hit following its Q4 earnings report earlier this week, let’s catch up on the name.

Company Profile

As a reminder, FLNG owns and operates a fleet of LNG carriers. It has a young, modern fleet all with XDF or MEGI propulsion engines and an average age under 4 years.

As of the end of 2023, ten of its vessels were on time charters expiring in 2026 or later. Its next open vessel is in Q2 2024.

Q4 Results And Increasing Spot Exposure

For its most-recent quarter, FLNG recorded vessel operating revenue of $97.2 million, down -1% from $97.9 million a year ago but up 3% sequentially from $94.6 million in Q3.

The company realized time charter equivalent (TCE) rates of $81,114 a day in the quarter, down from $81,699 last year. However, it saw an improvement from $ 79,207 in Q3.

Opex per day rose to $15,402 from $13,548 a year ago and $14,161 in Q3.

Net income came in at $19.4 million, or 36 cents per share, versus $41.4 million, or 77 cents a share, a year ago. Adjusted net income was $37.8 million, or 70 cents, versus $54.5 million, or $1.02 a share, a year ago. The results were hurt by $3.1 million in additional interest expense as a result of higher interest rates, as well as $2.2 million in higher vessel operating expenses.

Adjusted EBITDA came in at $76.2 million, down -4% from $79.1 million a year ago, and up 2% from $74.7 million in Q3.

The company declared a dividend of 75 cents for the quarter.

Turning to its balance sheet, FLNG ended the quarter with debt of $1.81 billion. It had cash and equivalents of $410.4 million. The company has no debt maturities before 2028.

Most of its rates are floating, but the company did enter swap transactions to create a fixed rate on $720 million of its debt. These hedges produced a loss of -$11.6 million in the quarter. It also has $144.4 million of fixed rate debt.

The company noted that the charter of its FLEX Constellation vessel will not exercise their extension option on the ship when it expires in Q2 of this year. FLNG will take delivery on the ship at the end of Q1 or the beginning of Q2 and then have it undergo its five-year drydocking maintenance. It will then market the vessel for short or long-term contracts.

The company noted that spot rates peaked in Q3 at around $200,000 per day, while 1-3 year rates were around $120,000 a day in the fall. Currently 1-3 years have fallen to $70,000-90,000 per day as more vessels enter the market. Longer term rates of 5-10 years were sitting around $95,000-105,000 per day, given the expectation of a tighter LNG shipping market as more LNG production comes online in a few years.

The global LNG fleet stood at about 630 vessels at the end of 2023, with 69 newbuild orders scheduled to be delivered in 2024.

Commenting on its outlook, CEO Oystein Kelleklev said:

“Over the next two years, we do see a somewhat more challenging freight market as there are more ships for delivery compared to the expected new export volumes. Hence, we think FLEX LNG is very well positioned as we have 94% charter coverage for 2024 and 50 years minimum firm charter backlog, which may increase to 71 years if all charterer’s options are extended. Additionally, our fleet consists entirely of large LNG carriers fitted with the most modern two-stroke propulsion system resulting in significant fuel savings compared to older generation tonnage. Reduced fuel consumption is also good for the environment and with EU Emission Trading System coming into force from 2024, this further enhances the premium which our ships can achieve in the market given the costs associated with such carbon emissions. Lastly, we have a very strong balance sheet where all the LNG carriers are financed with attractive long-term debt while our cash balance at year-end was a comfortable $411 million, giving us a high degree of financial flexibility.”

With the FLEX Constellation coming off contract, the company currently has spot market exposure of 13.3% for 2014 and 21.9% for 2025. The FLEX Courageous, meanwhile, is set to come off contract in Q1 2025, if its option is not exercised.

Notably, FLEX Constellation has been at a time charter rate of $80,000 a day. With FLEX Courageous delivered shortly after it, I’d expect a similar rate. Given current charter rates FLNG should be able to get a similar short-term rate for the vessels, or a higher rate on a longer term contract. However, the company should see lower rates from its FLEX Artemis vessel given its market-linked contract.

Overall, it was once again a steady quarter from FLNG, and an improvement over Q3. Interest rates remain a headwind, so the company’s results could benefit from potential Fed rate cuts later this year. Opex has also been on the rise, and is something I’d like to see reigned in a bit.

Valuation

FLNG trades at 9.5x the 2024 EBITDA estimates of $294.9 million and 9.4x the 2024 EBITDA consensus of $297.6 million.

On a P/E basis, it trades at 10.5x EPS estimates of $2.55. Based on the 2024 consensus for EPS of $2.78, it trades at 9.6x.

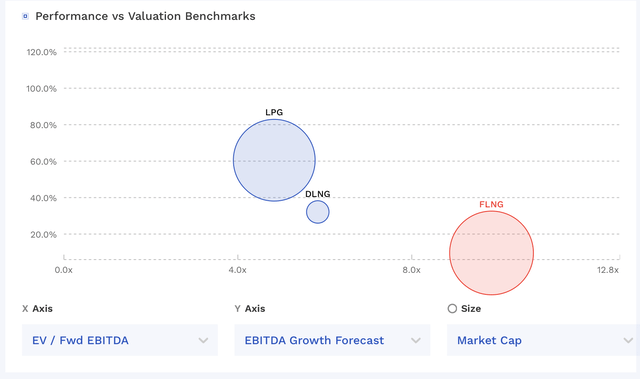

FLNG trades at a premium to other LNG and LPG shipping operators such as Dorian (LPG) and Dynagas (DLNG), although it has a younger, more modern fleet.

FLNG Valuation Vs Peers (FinBox)

It would cost about $3.38 billion to replicate FLNG’s fleet based on the prices FLNG has said where the newbuild market has settled at around $260 million per vessel. Discount that back by 10-15% due to the fleet being a few years old, and you’d get a value of between $30-$33.

Conclusion

With FLEX Constellation coming off charter this year and FLEX Courageous potentially coming off charter next year, FLNG will have more spot exposure until these vessels get recontacted out. However, the rates these vessels get shouldn’t be too different from where they are currently contracted out. Much will depend on the length of the new contracts, and FLNG’s results could get a boost if it charters out the vessels on longer term contracts.

The LNG transport market is in a bit of a transition period as more vessels come to market before an expected surge in LNG production. The Biden Administration, however, added a new twist to the market when they paused all permits for new LNG facilities that still need Department of Energy (“DOE”) approval to evaluate environment and economic impacts. The number of new LNG facilities already approved will still move forward, as of course will any non-U.S. facilities such as Qatar’s North Field Expansion project. However, it could delay or even potentially cancel some large LNG projects expected to come online in a few years.

I’m going to stay with my “Buy” rating, but lower my target to $30 from $38 to reflect slightly lower newbuild prices and the uncertainty caused by the Biden LNG facility pause. I think the latter issue is the biggest risk FLNG and others in the space face, so I would continue to monitor what happens here. Notably, with the Presidential election set for this year, a Republican win would likely wipe out this risk. At the same time, expect a weaker spot market in 2024 and 2025 before an improvement in 2026 and beyond when approved LNG projects come online.

Read the full article here

")

")

")

")

")