")

")

")

")

")

Investment Thesis

I take the view that MakeMyTrip Limited has potential upside to $77 based on continued sales growth, but will be monitoring growth in customer inducement costs across the Hotels and Packages segment.

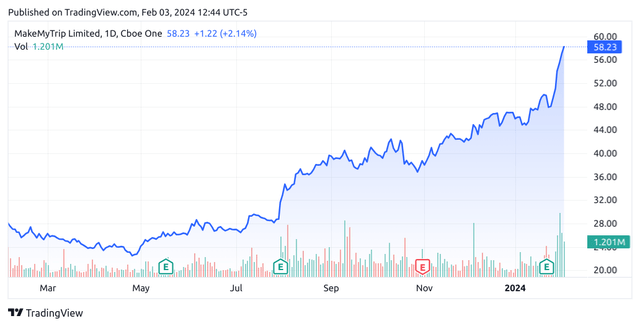

In a previous article back in November 2023, I made the argument that MakeMyTrip Limited (NASDAQ:MMYT) has the potential for further upside given continued growth in gross bookings.

Since then, the stock has ascended to a price of $58.23 at the time of writing:

TradingView.com

The purpose of this article is to elaborate on why I see potential upside to $77 for MakeMyTrip based on vibrant sales growth and also detail the risks that I will be watching for in the stock going forward.

Performance

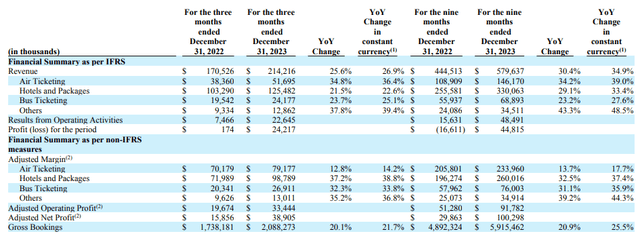

When looking at Q3 2024 earnings results for MakeMyTrip Limited as released on January 23, we can see that revenue growth across MakeMyTrip’s segments was highly impressive – showing strong double-digit growth and a 25.6% rise in overall revenue on a year-on-year basis.

MakeMyTrip Limited: Q3 2024 Earnings Release

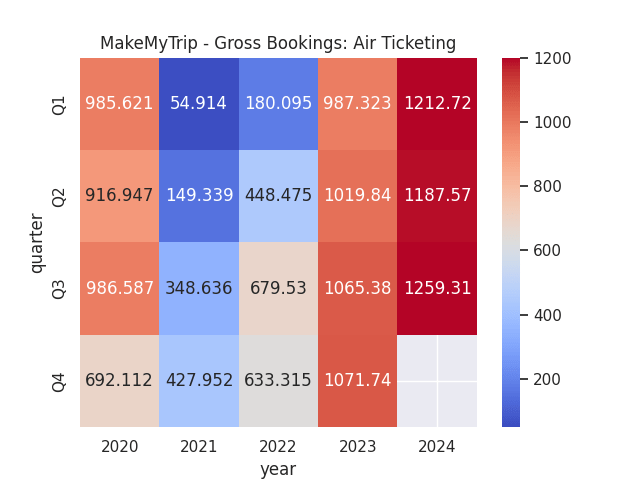

We see that on a percentage basis – the Air Ticketing segment showed the most growth at 34.8% year-on-year (excluding Others). In terms of gross bookings, the Air Ticketing segment accounts for the largest portion of bookings as compared to the Hotels and Packages and Bus Ticketing segments. From the below, we can see that gross bookings are up by 18% as compared to the prior-year quarter. We also see this to be the case for the two previous quarters in 2024.

Figures sourced from previous MakeMyTrip Earnings Releases (Q1 2020 to Q3 2024). Figures provided in USD millions. Heatmap generated by author using Python’s seaborn visualisation library.

With the months of October to March representing the high season for travel across India, growth in gross bookings across Q3 is in line with expectations, and it is reasonable to expect bookings in Q4 to come in at a similar level to this quarter if not higher.

With regards to short-term liquidity, we can see that the quick ratio of MakeMyTrip Limited (calculated as total current assets less inventories all over total current liabilities) has decreased from that of last year but still remains significantly above 1 – indicating that the company is still in a position to service its current liabilities using existing liquid assets.

| December 2022 | December 2023 | |

| Total current assets | 650851 | 836910 |

| Inventories | 16 | 16 |

| Total current liabilities | 234507 | 547117 |

| Non-current loans (long-term debt) | 3018 | 232463 |

| Total assets | 1336033 | 1525491 |

| Quick ratio | 2.78 | 1.53 |

| Long-term debt to total assets ratio | 0.23% | 15.24% |

Source: Figures (in USD thousands) sourced from MakeMyTrip Q2 2023 and Q2 2024 Press Releases. Quick ratio and long-term debt to total assets ratio calculated by author.

We can see that the long-term debt to total assets ratio is up substantially over the period, but this is due to a large portion of current loans and borrowings in Q2 2023 being re-designated as non-current in Q2 2024. Current loans and borrowings are down from USD 227.8 million in the prior year quarter to USD 16.2 million in the most recent quarter.

My Perspective and Looking Forward

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, the fact that gross bookings have continued to see growth and overall revenue growth has remained vibrant is encouraging.

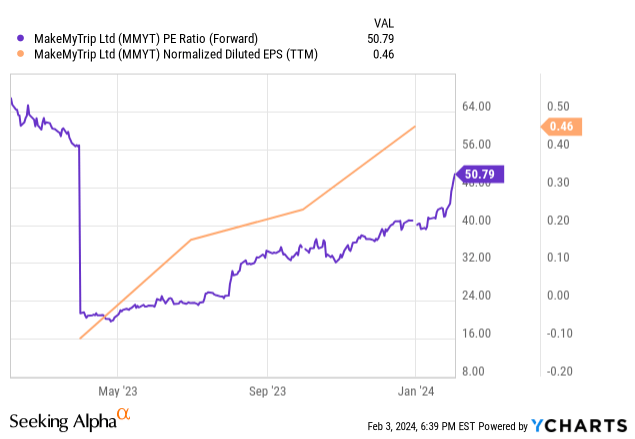

When looking at the earnings trajectory of MakeMyTrip, we can see that the company has seen strong earnings growth over the past year – but the P/E ratio has also been rising, indicating that growth in price is outpacing that of earnings.

ycharts.com

Given that the company has only started to see earnings grow into positive territory within the last year, I do not deem it appropriate to attempt to value MakeMyTrip on an earnings basis at this time. However, the company’s rising P/E ratio would indicate that price is rising faster than earnings at this time.

With that being said, given that MakeMyTrip continues to see a rising P/E ratio and revenue growth continues to remain vibrant for the company – I take the view that the stock has further room to rise on a revenue basis – provided we continue to see accompanying earnings growth.

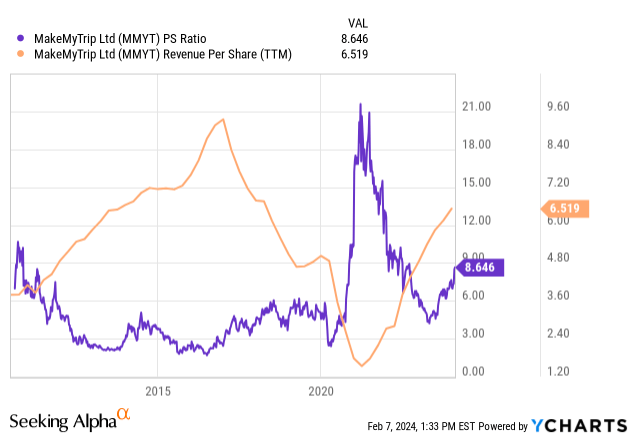

When looking at MakeMyTrip’s price to sales ratio as an alternative measure of value – we can see that the price to sales ratio is higher than pre-2020 levels while revenue per share is on an upward trajectory yet remains below the highs seen previously.

ycharts.com

In this regard, given a fair value of $56 ($6.519 revenue per share * 8.646x P/S ratio = $56.36) – I take the view that if we see revenue per share continue to grow back to previous highs of $9, then fair value on this basis would increase to $77 ($9 revenue per share * 8.646x P/S ratio = $77.81). In this regard, I take the view that for as long as sales growth continues to remain supported by earnings – MakeMyTrip could potentially have upside to $77 if sales growth remains robust.

Risks

While I see potential upside based on continued sales growth, the main risk for MakeMyTrip in my view is that earnings do not grow sufficiently in line with sales due to higher costs accompanying such revenue growth.

We can see that the company recorded an increase in both marketing and sales promotion expenses, as well as a rise in customer inducement costs recorded as a reduction of revenue:

MakeMyTrip Q3 FY24 Earnings Release

When analysing this in more detail, we can see that customer inducement costs saw a significant increase of 41% across the Hotels and packages segment.

MakeMyTrip Q3 FY24 Earnings Release

This is notable given that Hotels and Packages is the largest segment by revenue but showed lower year-on-year revenue growth as compared to other segments – albeit at a respectable 21.5%. In this regard, should we see customer inducement costs continue to outpace revenue growth across this segment, then this could give investors pause. While revenue growth across the Air Ticketing segment remains vibrant – a slowdown across the Hotels and Packages segment could hinder further growth in the stock.

In this regard, I will be paying particular attention going forward as to whether growth in customer inducement costs across the Hotels and Packages segment can be contained. Specifically, I would like to see a significant slowdown in growth across costs to the extent that this does not exceed revenue growth – i.e. if revenue for the next quarter is up by 20% for Hotels and Packages, then growth in inducement costs should not exceed this.

Conclusion

To conclude, MakeMyTrip Limited has seen encouraging revenue and gross bookings growth across the Air Ticketing segment. However, customer inducement costs across the Hotels and Packages segment continue to rise. While I remain bullish on the stock and see an upside based on continued sales growth, I will continue to monitor if MakeMyTrip can ultimately bolster revenue growth across the Hotels and Packages segment while also reducing the rate of growth in customer inducement costs.

Read the full article here

")

")

")

")