")

")

")

Overview

I covered Peabody Energy Corporation (NYSE:BTU) in January, which was more of an overview on the company, and that article can be found here. In this article, I wanted to focus on the company’s Q4 2023 results, released earlier today. I also wanted to discuss the recent S&P SmallCap 600 index inclusion that happened in late January, and the implications from that.

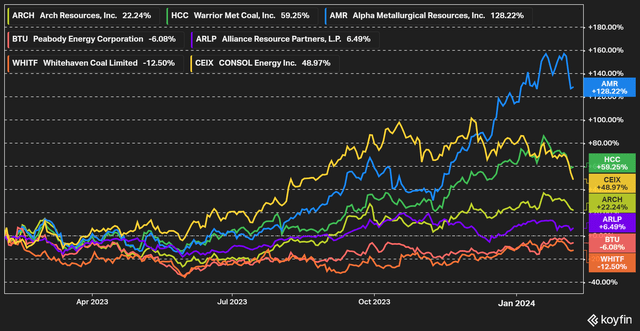

Figure 1 – Source: Koyfin

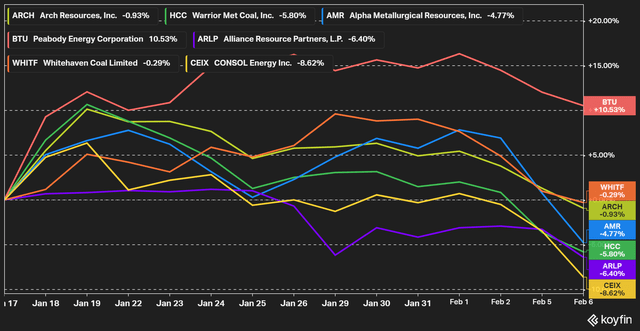

Peabody has lagged many of the better-performing coal mining companies over the last year, but it has, since the index inclusion announcement, had a relatively strong performance, as illustrated in the chart below. Even if you took a day to digest the index inclusion news, you would have done better in Peabody than the other peers in the chart below.

Figure 2 – Source: Koyfin

Index Inclusion & ETF Buying

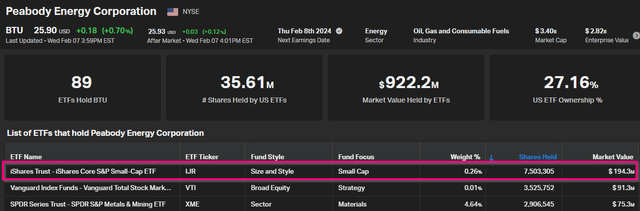

Before the open at the 18th of January this year, it was announced that Peabody would be included in the S&P SmallCap 600 index, and the effective date of the index inclusion was the 23rd of January.

Figure 3 – Source: Koyfin

U.S. ETFs did at that time of the announcement hold 25M shares of Peabody, equal to 19% of the basic shares outstanding. Because of the index inclusion, we have seen the ETF ownership increase substantially, to now 35.6M shares and 27% of the company. Much of this increase has come from the iShares Core S&P Small-Cap ETF (IJR), as highlighted in the figure below. However, there have been smaller tracker ETFs which have contributed to the increased ETF ownership as well.

Figure 4 – Source: Koyfin

The ETF buying is unlikely to be completely over at this point, though. Most index trackers will have bought their Peabody shares around the effective date, but there are also ETFs that are more indirectly linked to that index, which have yet to rebalance since the index inclusion of Peabody.

I am specifically thinking of Pacer US Small Cap Cash Cows 100 ETF (CALF). That is another large ETF, with $7.8B in assets under management. The ETF selects the top 100 companies in the index, based on the trailing free cash flow yield, where Peabody is highly likely to be included in the next quarterly rebalancing. From that and other smaller ETFs, I would roughly expect another 4-7M shares to be bought in Peabody by ETFs over the coming months.

Q4 2023 Result

Peabody did in Q4 report an adjusted EBITDA of $345.1M, compared to $270.0M in the prior quarter. Net Income was $192.0M or $1.33 per diluted share, compared to $119.9M or $0.82 per diluted share in Q3. The Q4 EPS was somewhat below the consensus estimate of $1.42 at Seeking Alpha. The company did by the end of the year have a very impressive $969M in cash and cash equivalents.

Figure 5 – Source: Peabody Quarterly Reports

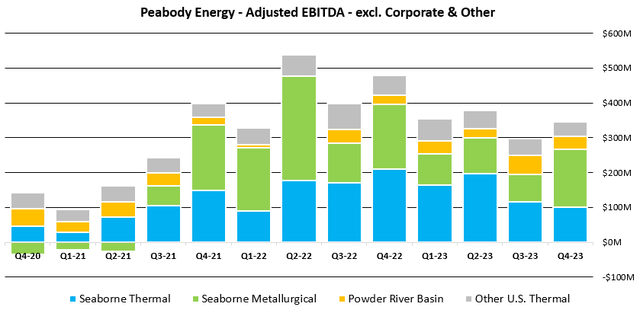

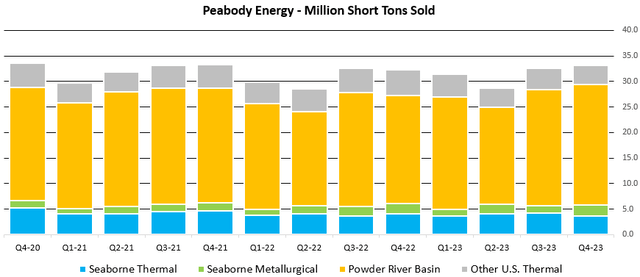

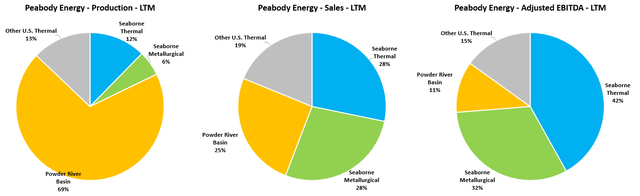

The solid quarterly result was due to healthy production volumes and relatively good margins in most of the operating segments.

Figure 6 – Source: Peabody Quarterly Reports

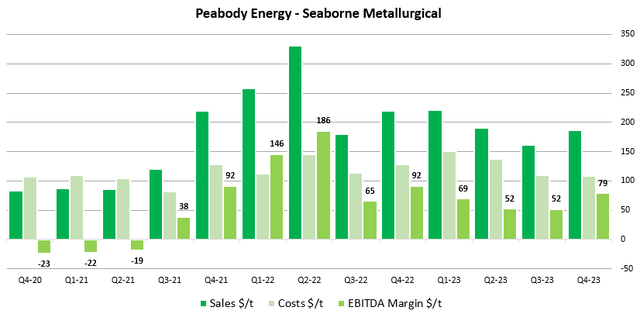

The margin was especially impressive in the Seaborne Metallurgical segment, where we saw a substantial improvement in Q4 compared to Q3. The Seaborne Metallurgical segment experienced a $27/t increase in Q4 compared to Q3.

Figure 7 – Source: Peabody Quarterly Reports

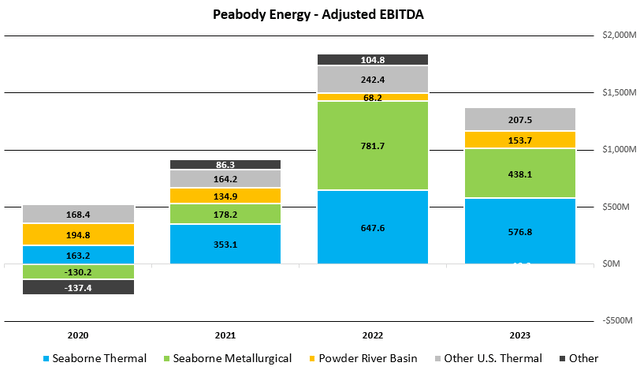

2023 was a good year overall, with an adjusted EBITDA of $1,363.9M, down somewhat from the record $1,844.7M in 2022. The company did in 2023, similar to 2022, get most of the adjusted EBITDA from the two seaborne segments. Diluted EPS did in 2023 come to $5.00 compared to $8.31 in 2022.

Figure 8 – Source: Peabody Quarterly Reports

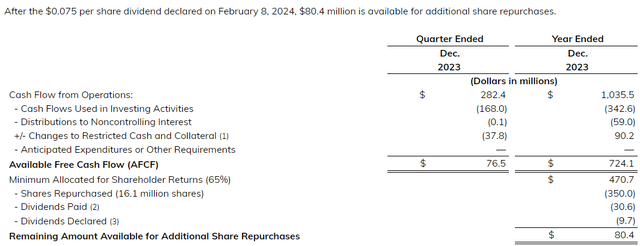

The available free cash flow for the full year was an impressive $724.1M in 2023. Peabody has during the year bought back more than 11% of the shares outstanding, where I would note that the company still has $80.4M left from the 2023 free cash flow to be used for buybacks. That would equal about 3M shares to be bought back.

Figure 9 – Source: Q4-23 Result

Valuation & Conclusion

I continue to think Peabody is an attractive investment here. This is a relatively diversified coal mining company, in relation to countries, regions, and types of coal. So, while the company is looking to become more of a metallurgical coal producer in the future, the exposure is at this point relatively mixed.

Figure 10 – Source: Peabody Quarterly Reports

The free cash flow yield based on 2023 reported figures is now 26%, using the latest diluted shares and enterprise value. With the market cap, the 2023 free cash flow yield is 19%.

I don’t doubt we will see some margin compression in the thermal sales during 2024, primarily due to lower prices. However, the company has also guided for an increased sales volume of metallurgical coal and lower costs in both two seaborne segments during 2024.

For 2024, we can likely expect the free cash flow yield to roughly be around 15%, using market cap, and around 20% with the enterprise value. So, when we consider how well capitalized Peabody is, the high free cash flow yield, a commitment to buybacks, which has also been demonstrated over the last year, together with some more expected ETF buying, I like the prospects for Peabody Energy Corporation going forward.

Read the full article here

")

")

")