")

")

")

In this analysis, we covered Fortinet, Inc. (NASDAQ:FTNT), which we identified previously in our analysis of Palo Alto (PANW), as the second-largest cybersecurity company by market share (6.2%). The company has a highly impressive growth track record with consistently high growth at a 10-year average of 24.1% and a 5-year average of 24.2%, compared with the cybersecurity growth of 16.3%. Thus, we examined whether its strong growth could be sustainable by analyzing its business segments with a comparison to the overall long-term market growth outlook. Furthermore, we examined its business model and determined if it could benefit from cross-selling opportunities and support its growth outlook. Finally, we examined whether there is possible future industry consolidation and if the company could be positioned to capitalize on M&A activity with its profitability and financial position.

Positive Double-Digit Market Growth Outlook

|

Fortinet Revenue ($ mln) |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

|

Revenue |

615 |

770 |

1,009 |

1,275 |

1,495 |

1,805 |

2,163 |

2,594 |

3,342 |

4,417 |

5,305 |

|

Revenue Growth |

15.22% |

25.21% |

31.01% |

26.36% |

17.21% |

20.72% |

19.86% |

19.94% |

28.82% |

32.17% |

20.1% |

Source: Company Data, Khaveen Investments

Based on the table of its revenue and growth above, the company has a strong track record with positive double-digit growth every year in the past 10 years for a total average of 24.1% and 24.2% in the past 5 years. Following its latest earnings release, the company’s full year 2023 growth moderated to 20.1%, below its average but followed after its strongest year of growth in 2022 (32%). We examined the market growth outlook in comparison with the company’s growth below.

|

Cybersecurity Market Segments |

Segment Size ($ bln) (2022) |

Segment Size (2027F) |

CAGR |

|

Identity & Access Management |

14.7 |

27.9 |

13.7% |

|

Vulnerability & Security Analytics |

13.9 |

29.5 |

16.2% |

|

Data Security |

4.2 |

12.3 |

23.9% |

|

Web & Email Security |

3.9 |

7.2 |

12.8% |

|

Network Security |

22.9 |

42.3 |

13.0% |

|

Endpoint Security |

9.4 |

23.4 |

20.0% |

|

Integrated Risk Management |

10.9 |

21.2 |

14.3% |

|

Total |

80 |

163.8 |

15.4% |

|

Market Historical 5-year Growth Average |

16.3% |

Source: Market Research Reports, Khaveen Investments

Based on our compilation of the cybersecurity market segments and CAGR from our previous analysis, we derived the total forecast CAGR of the cybersecurity market as 15.4%, in line with the past 5-year average of 16.3%. Though, it is lower than the company’s 5-year average growth of 24.2%. Moreover, the company specializes in the Network Security segment based on its segment breakdown from its investor presentation below.

Fortinet

As seen from its investor presentation, the largest segment of the company is Secure Networking which represents the majority or 70% of its revenues. The products stated in this segment are under network security. For example, based on its annual report, Fortinet’s product range includes FortiGate Firewall for multifaceted defense, FortiSwitch, and FortiAP for network security, FortiExtender for secure wireless connectivity, FortiNAC for access control, and FortiDDoS for mitigating DDoS attacks.

Some of the growth drivers of network security include:

- Integration of IoT, Machine Learning, and Cloud introduces fresh challenges in network security.

- Increasing cyberattacks and data breaches across various industries.

- Rising awareness and demand for network security solutions among resource-constrained SMEs.

However, the market CAGR forecast for network security segment of 13% is even lower than the overall market forecast CAGR of 15.4%.

Outlook

Overall, the company’s growth track record had been impressively stable with an average of 24.1% in the past 10 years and 24.2% in the past 5 years on average. In comparison, the company’s growth rate had been higher than market growth (5-year average of 16.3%). Therefore, we believe that its growth was driven by competitive advantages. In our previous analysis, we ranked Fortinet as the top 3 within network security, trailing behind only Palo Alto and Cisco. Moreover, our derived market forecast CAGR of 15.4% is fairly in line with the historical market growth. Thus, we believe the market growth remains sustainable and could further support its growth outlook. In the past, the company grew at a rate higher than the market by a factor of 1.49x. Assuming the company’s specific advantages remain the same, we forecast the company’s long-term growth rate to be 23% based on the same factor multiplied by the cybersecurity market forecast CAGR of 15.4%.

Benefit From Cross-Selling Opportunities

Based on the company’s latest earnings briefing, management provided revenue growth guidance of 9% at the midpoint for 2024, which is considerably lower than its past growth as management highlighted “project and product digestion in 2024” affecting its outlook but is optimistic of a recovery in H2 2024. We examined other factors that could lead it to beat guidance, such as cross-selling opportunities.

|

Fortinet Segment Revenue ($ mln) |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

5-year Average |

|

Product Revenue |

674 |

789 |

916 |

1,255 |

1,781 |

1,927 |

|

|

Growth % |

16.8% |

16.9% |

16.2% |

36.9% |

41.9% |

8.2% |

24.0% |

|

Security Subscription Revenue |

606 |

751 |

919 |

1,125 |

1,427 |

1,872 |

|

|

Growth % |

20.1% |

23.9% |

22.4% |

22.5% |

26.8% |

31.2% |

25.3% |

|

Technical Support & Other Revenue |

524 |

624 |

759 |

962 |

1,210 |

1,507 |

|

|

Growth % |

26.9% |

19.0% |

21.7% |

26.7% |

25.7% |

24.6% |

23.6% |

|

Total |

1,805 |

2,163 |

2,594 |

3,342 |

4,417 |

5,305 |

|

|

Growth % |

20.7% |

19.9% |

19.9% |

28.8% |

32.2% |

20.1% |

24.2% |

Source: Company Data, Khaveen Investments

From the table, the company’s revenues are broken down into Products, Subscription and Technical Support Revenues. As seen, all segments had strong double-digit growth in the past 5 years, indicating strength across all segments. Its product segment includes hardware such as firewall equipment. As stated in its annual report, customers not only purchase their hardware equipment but also often purchase subscription and technical support services.

An end-customer deployment may involve as few as one or as many as thousands of appliances as well as other Fortinet Security Fabric products…Often, our customers also purchase our FortiGuard security subscription services and FortiCare technical support services. – Fortinet Annual Report 2022

- Product with Security Subscription

Based on its annual report, its products such as its Core Platform that includes hardware like firewalls are sold with security services such as FortiGuard.

Our Core Platform hardware and software licenses are sold with a set of Core Platform broad security services. These security services are enabled by FortiGuard Labs, which provides threat research and artificial intelligence capabilities from a global cloud network to deliver protection services. – Fortinet Annual Report 2022

The company’s FortiGuard services integrate into Fortinet’s threat intelligence platform, providing continued updates for its Security Fabric protection against evolving threats.

- Technical Support and Security Services

Between Technical Support and Security Services, the company offers remote threat monitoring services to help its customers during security incident responses as a premium service for its FortiEDR subscription.

Fortinet also offers remote, cloud-based IR and monitoring services to help customers identify, remediate and understand compromises. This service leverages our FortiEDR capabilities either as part of a premium FortiEDR subscription for continuous monitoring or alternatively, can be deployed to help deliver IR services on a per incident basis. – Fortinet Annual Report 2022

Additionally, the company also provides training services to customers through its team to assist customers and organizations in understanding the use of their services.

- Technical Support and Product

Within Technical Support, the company provides professional services personnel such as consultants and security architects that assist organizations in implementing the company’s products.

Our professional services consultants and security architects help to formulate customer-specific security strategies, develop roadmaps for securing digital initiatives and design product deployments. They work closely with end-customers to implement our products according to design, utilizing network analysis tools, traffic simulation software and scripts. – Fortinet Annual Report 2022

Furthermore, within its subscription services segment, based on its annual report, the company highlighted the bundling of products which we believe further shows its cross-selling opportunities.

Fortinet

Outlook

Overall, we believe the company’s strong cross-selling opportunities are evident across various segments such as between its products, security subscriptions and technical support segments as these products are sold together. Additionally, within security services, we believe its cross-selling is also highlighted by service bundles of various products within the segment. Furthermore, the company previously highlighted previously cross-selling opportunities for its SD-WAN customers with its new SASE solutions. Thus, we believe these cross-selling opportunities could support its total growth outlook and for the company to potentially beat its revenue guidance for 2024.

Company Could Strengthen Its Position Amid Industry Consolidation

Finally, we examined whether there could be industry consolidation and whether Fortinet could capitalize on it to support its growth outlook.

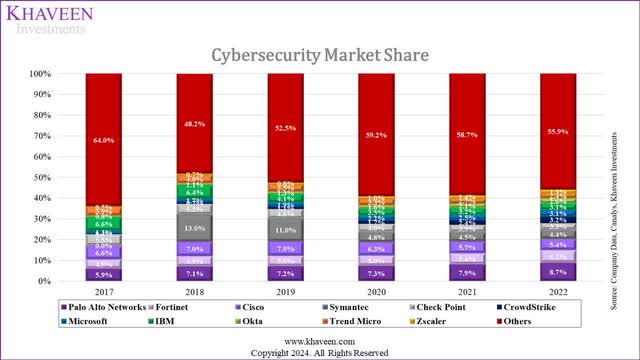

Company Data, Canalys, Khaveen Investments

Firstly, in terms of the cybersecurity market share from our previous analysis, the top 10 companies’ market share combined had increased in the past 6 years.

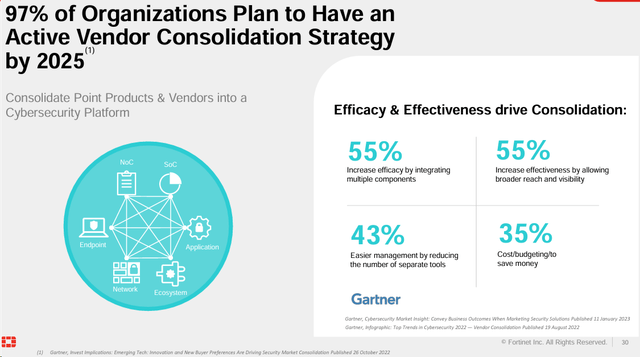

Furthermore, the company also highlighted vendor consolidation strategies by organizations in its investor presentation. Vendor consolidation involves “reducing the number of security vendors by buying multiple solutions from a single provider”. According to the Ponemon Institute, an average company uses 45 various security products. There are several benefits of vendor consolidation in cybersecurity such as:

- Mitigating Cybersecurity Risks: Reducing the number of security vendors significantly lowers the risk of supply chain attacks, simplifying the vetting process for security policies and source code. According to Gartner, a majority of surveyed organizations, specifically 65%, anticipate enhancing their overall risk posture.

- Enhancing Operational Efficiency: Unified sales and support streamline issue resolution and deepen understanding of the client’s needs, while reduced administration redirects valuable time and resources towards critical security tasks.

- Achieving Cost-Effectiveness: Integration and interoperability between tools, coupled with bundle opportunities for reduced costs, create a streamlined and cost-effective security strategy. Notably, vendor consolidation eases compliance with industry standards, as managing fewer security policies and vendors simplifies the auditing process. According to Gartner, 35% of survey respondents anticipate achieving cost savings.

Fortinet, Gartner

Based on its presentation citing Gartner, 97% of organizations have vendor consolidation plans. The 2023 Pen Testing Report stated that 80% of participants deem it somewhat crucial for enhancing overall cybersecurity posture. Furthermore, the industry has seen several large M&A deals above $300 mln as highlighted below.

Source: Company Data, Khaveen Investments

Based on the table, we compiled a total of 9 significant acquisitions since 2016 of cybersecurity companies with 2023 having the most acquisitions. As seen, the largest deal is the planned acquisition of Splunk by Cisco (CSCO) in 2023 with a deal valued at $28 bln, which is 2.6x higher than the second largest deal, Broadcom’s (AVGO) acquisition of Symantec in 2019. However, Fortinet has not had any significant acquisitions in the period, with an average total spending on acquisitions per year of $27 mln in the past 10 years. Nonetheless, the company’s management had previously indicated that could be open to future acquisitions in the quote below, highlighting its appetite for M&A opportunities which could support further growth.

We feel we are the strongest on the internal innovation engineering among all the space, player. But on the same time, we also were open to looking for some other companies which we can work together, join together. – Ken Xie, Founder, Chairman & Chief Executive Officer

Outlook

Overall, we believe the cybersecurity market could face consolidation as seen by the increasing market share of the top 10 cybersecurity companies in the past 6 years. Studies also show that organizations are increasingly pursuing vendor consolidation strategies to streamline their security operations. Moreover, there has been an increase in M&A deals in 2023 with the largest deal by Cisco’s acquisition of Splunk which we believe further indicates consolidation. While Fortinet had yet to make significant deals, management indicated that they could be open for more M&A deals going forward.

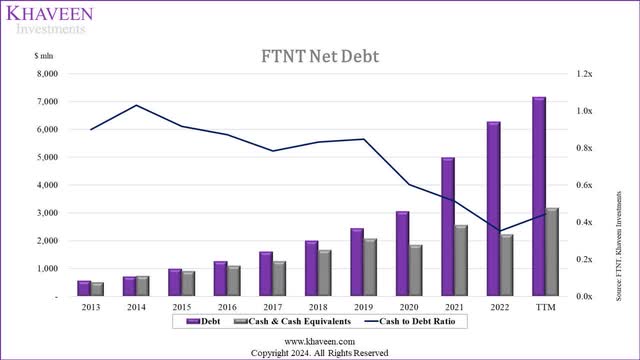

Company Data, Khaveen Investments

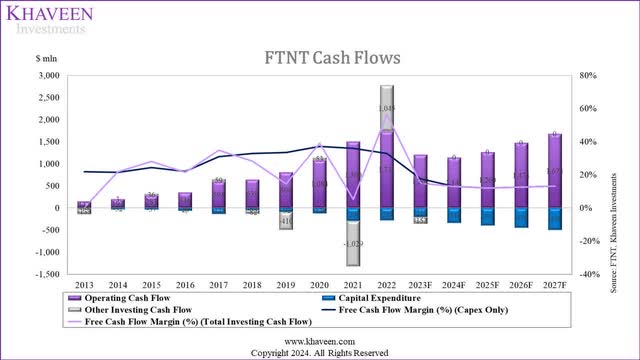

At first glance, analyzing the company’s financial position, we see that its net-to-debt ratio has deteriorated in the past 10 years which does not bode well for it to pursue M&A.

Company Data, Khaveen Investments

However, examining its FCF margins, we see that it has strong and stable FCFs with an average FCF margin of 28.7% (5-year average) and 25% (10-year average). Based on our forecast, we modeled the company to generate $772 mln in FCF in 2024. Based on the average system software companies with $1 bln in revenues’ P/S of 1.87x, we estimate the company could generate $413 mln in revenues from acquisitions, which is a boost of 7.7% to its 2023 revenues.

Risk: Competition From Market Leader Palo Alto

We believe one of the risks of the company is competition from larger players such as Palo Alto which is the market leader of the cybersecurity market, and we previously ranked it as the top in terms of cybersecurity companies. Moreover, the company competes directly with Palo Alto in the network security segment, which is Fortinet’s largest segment and also superior to the company in terms of Network Firewall and SSE products in our comparison analysis, potentially gaining share over competitors including Fortinet.

Verdict

All in all, the company has maintained impressive and stable positive growth, averaging 24% over the past 10 years, surpassing the market growth rate of 16.3%. We believe this robust growth is attributed to its competitive advantages, positioning Fortinet as a top 3 player in network security. Moreover, we also believe cross-selling opportunities are evident in various segments, including products, security subscriptions, and technical support. We believe these opportunities, along with service bundles within the security services segment, could support growth for the total company and potentially surpass its revenue guidance of 9% in 2024.

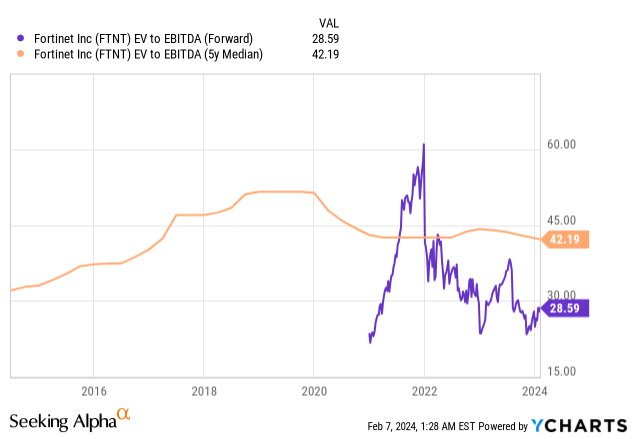

Furthermore, in the cybersecurity market, we anticipate consolidation, indicated by the increasing market share of the top 10 companies over the past 6 years. Organizational trends toward vendor consolidation align with this, supported by increased M&A activity, such as Cisco’s acquisition of Splunk. While Fortinet has not made significant deals, management expressed openness to future M&A. Despite a deteriorating net-to-debt ratio over the past 10 years, the company exhibits strong and stable FCFs, with an average FCF margin of 28.7% (5-year average) and 25% (10-year average). Projecting $772 mln in FCF in 2024, we believe the company is primed for future acquisitions with potential revenues from acquisitions at $413 mln, providing a boost of 7.7% to its growth. Based on the chart below, the company’s forward EV/EBITDA is 32% below its 5-year median of 42.19x, indicating an attractive valuation.

YCharts

Thus, we assigned a Buy rating for Fortinet based on the highest range of analysts’ consensus price target is $77, an upside of 14%.

Read the full article here

")

")

")