")

")

: Time To Lighten Up On CCC Exposure (Downgrade)")

Thesis

When credit spreads are tight and the equity market displays exuberance, a prudent retail investor needs to lighten up on risky exposure, not FOMO in additional risk. Everything seems to be priced for perfection these days, with an ‘immaculate disinflation‘ in the cards, and a soft landing as the base case for most economists on Wall Street. What if things end up different?

KKR Income Opportunities (NYSE:KIO) is a fixed income CEF focused on U.S. high yield. The CEF is a robust long term performer, but the fund falls in the very high beta category via its collateral composition which is focused on CCC credits. High beta references the propensity of a fund to move more than the market when risk factors change:

Beta is the volatility of a security or portfolio against its benchmark. It’s a numerical value that signifies how much a stock price jumps around. The higher the value, the more the company tends to fluctuate in value.

One of the cornerstones of active portfolio management is to increase and reduce exposures to tailor a portfolio for certain market positionings. We are of the opinion that the market is not pricing in any tail events, and we will get risk-off events this year. The best way (in our opinion) to position a portfolio for today’s environment is to decrease the beta of a portfolio rather than go all in cash (or a high cash allocation). Decreasing the beta of a portfolio ensures a lower drawdown when such market moves occur, and the maintenance of a certain risk and dividend profile in a portfolio with less overall volatility.

In this article we are going to revisit the KIO portfolio and its composition, and highlight why we believe this fixed income CEF is a high beta name which should be pruned at this stage of the macrocycle.

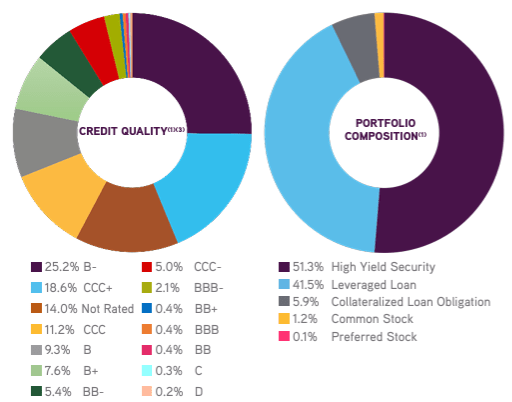

A CCC heavy collateral

The CEF is focused on U.S. high yield debt and leveraged loans:

Rating (Fact Sheet)

The collateral is almost evenly split between junk bonds and leveraged loans, with a small bucket for CLOs.

What makes KIO an outlier is its very heavy CCC exposure. As we can notice from the above table, the ‘CCC’, ‘CCC+’ and ‘Not Rated’ sleeves account for over 44% of the portfolio. That weighting is enormous, when run of the mill fixed income CEFs have CCC buckets below 10% of the collateral.

A very credit risky portfolio translates into a higher volatility metric as measured by standard deviation and drawdowns. KIO has a 12% 3-year standard deviation, and has recorded outsized drawdowns during the recent market swoons when compared to other fixed income CEFs:

KIO does a good job to mitigate some of its credit-riskiness via a low duration profile, with the fund displaying a duration of only 1.88 years. However, in a true risk-off environment credit spreads and illiquidity will play a large role in pulling prices down in the fund’s portfolio.

Spreads are stretched

Given the CEF’s large exposure to the CCC asset class, let us have a look on where credit spreads are for these names:

CCC Spreads (The Fed)

CCC spreads as measured by the ICE BofA CCC & Lower US High Yield Index, have tightened substantially in the past months, currently being at 946 bps, and at the lower end of the range in the past two years.

Tight spreads reflect the ‘immaculate landing’ scenario, but the risks are skewed to the upside in terms of a risk-off scenario. Higher spreads would result in a lower price for KIO.

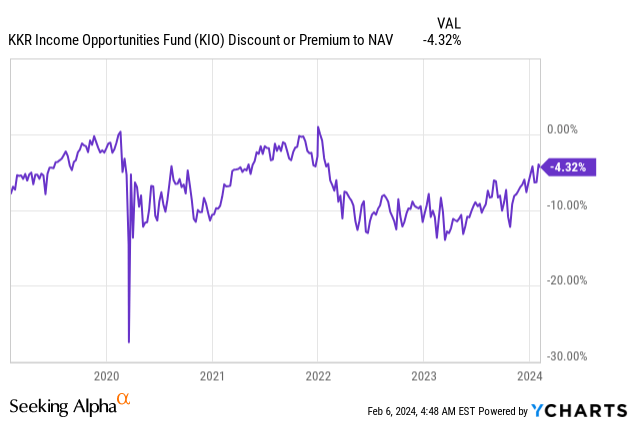

When an investor buys a fixed income CEF they need to zone in the risk factors driving performance. While we have seen peak rates, spreads are currently too tight, while KIO’s discount to NAV has tightened substantially as well (more on that topic in the section below). We feel right now the risks are skewed towards lower pricing in the CEF driven by a risk-off event and the high beta nature of the fund.

Active portfolio management

We are proponents of active portfolio management, even for true buy and hold investors. We feel certain high beta names can be successfully bought during periods of extreme market fear, and partially sold during exuberance. A high beta name will tend to outperform in both directions.

We feel this is an appropriate approach for high beta names since it manages volatility for a credit portfolio. While KIO is a robust long term performer, some of its metrics as a CEF highlight why a retail investor would do well to lighten up on exposure here:

The fund usually trades with a discount to NAV of roughly -10%, with the zero rates environment of 2021 seeing the CEF move to flat to NAV. During the October/November 2023 market risk-off event, the CEF traded at its usual discount. As of late, given the overall market exuberance, the fund is finding itself closing in on being flat to NAV again. We feel we are moving from one extreme to the other, hence our view that it is a good time to lighten up on some exposure here.

Conclusion

KIO is a fixed income CEF from the KKR platform. The fund has a very robust long term performance, but makes a name for itself via its very credit risky collateral. The fund has a ‘CCC’, ‘CCC+’ and ‘Not Rated’ rating allocation which exceeds 44%, making it a high beta name. High beta names in our opinion are best to be actively managed, even though long term they produce robust returns. In KIO’s case, buying the fund during significant market risk-off events can result in outsized returns when risk factors return to their average levels. Conversely, in a scenario like today’s when we are witnessing equity market exuberance and very tight credit spreads, the best portfolio allocation move in our opinion is to reduce exposure to the name. With risk skewed to the downside in terms of price action, we feel a retail investor is best served to reduce their CCC portfolio exposure currently.

Read the full article here

")

")

")