")

")

")

Introduction

Parker-Hannifin Corporation (NYSE:PH) just recently reported its Q2 2024 results which led to a nice pop in the share price. In this article, I’ll delve deeper into the recent results, provide some context on how we got here, and assess the current valuation and risks as it relates to the future outlook of the company.

Background

Parker-Hannifin is an industrial company that sells motion and control technologies that include hydraulics, pneumatics, electromechanical, process control, and more. The company serves customers in a wide range of industries including aerospace, life sciences, construction, oil and gas, military, and defense. The company has two main segments: Diversified Industrial and Aerospace Systems. Diversified Industrial can be separated into North America (48% of total revenues) and International (30% of total revenues). This segment mostly sells to OEMs and distributers selling sealing, shielding, thermal products, adhesives, coatings, and noise vibration solutions. As one might imagine, this has applications in many industries.

In the Aerospace Systems segment, the company sells to OEMs and end users who use the company’s products in commercial and military airframe and engine programs. Essentially, these are all products that are essential to the successful functioning of different kinds of aircraft including business jets, commercial transport, military, helicopters, and more. The segment accounts for the remaining 22% of total revenues.

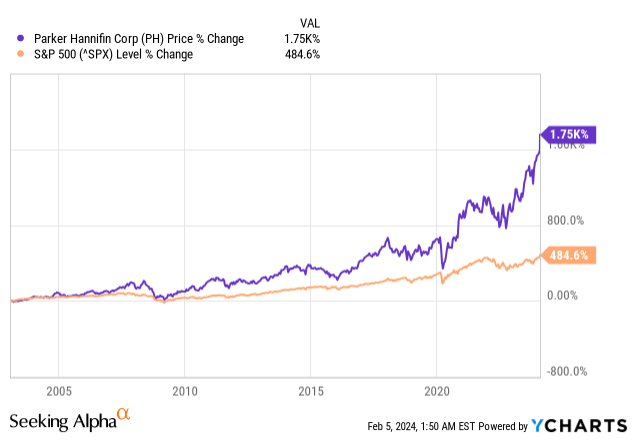

Despite appearing to be a boring industrial company, Parker-Hannifin has put up great returns for shareholders over the long-run. Since 2003, the company’s shares have returned a staggering 1753% return compared to the S&P500’s return of 485% (excluding dividends). For investors who’ve been able to hold onto this winner, they’ve certainly been rewarded with a twenty-year compound annual return of 15.7%.

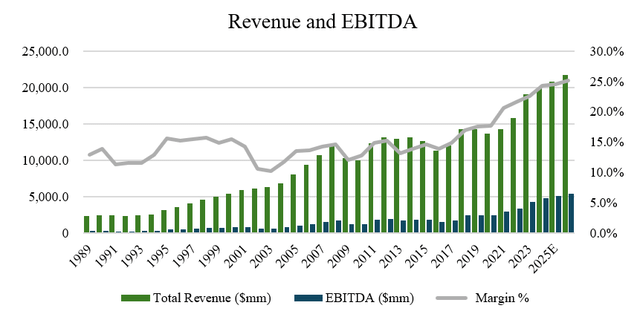

And it shows up in the numbers too. Parker-Hannifin has a twenty year track record of growing revenues at a 5.7% CAGR and EBITDA at a 9.9% CAGR. Even on a 10-year basis, the numbers are impressive, growing revenues and EBITDA at CAGRs of 3.9% and 9.6%, respectively (source: S&P Capital IQ). With 1230 basis points of margin expansion over the last twenty years and 937 basis points of margin expansion in the last ten years, Parker-Hannifin’s excellent returns to shareholders have been as a direct result of improving financials over long periods of time.

Author, based on data from S&P Capital IQ

Driving this strong growth has also been a very disciplined M&A strategy. Historically, the company has looked to maintain and growth its competitive position in the industry by pursuing M&A that brought Parker-Hannifin new technologies that it could help fill in the missing pieces of its previous business. In areas like filtration, engineered materials, and vibration technologies, the company expanded its portfolio of offerings in aftermarket products that tend to be higher margin.

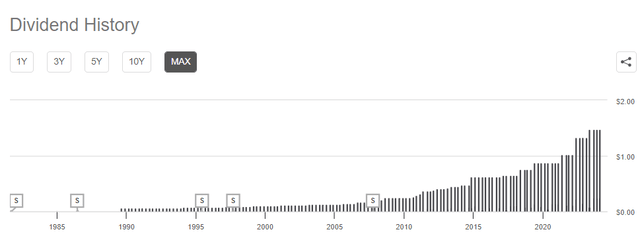

In addition to improving financials and a solid acquisition strategy, Parker-Hannifin has also delivered value to shareholders by paying dividends which have grown over time as well as by repurchasing stock. Over the last five years, the company has grown its dividend at a 14% CAGR and the quarterly dividend of $1.48 per share that was approved for the quarter will mark the company’s 295th consecutive quarterly dividend. On the share repurchase front, since 2003, the company has reduced its share count by 49.4 million shares, which is about a 28% reduction over the last 20 years (source: S&P Capital IQ). What this shows is that the company has been able to reinvest in the business both organically and through acquisition, but also return excess cash to shareholders via dividends and stock buybacks.

Seeking Alpha

Q2 2024 Results

When looking at the recent results for Parker-Hannifin, the company reported a beat on EPS by $0.89 with the quarterly EPS coming in at $6.15. On revenue, while sales were up 2.8% year over year, the $4.821 billion figure was a miss from analysts’ estimates by about $20 million.

With mixed results, the market reacted positively to the quarter and I think there’s reasons to be optimistic about the results from this quarter.

Investor Presentation

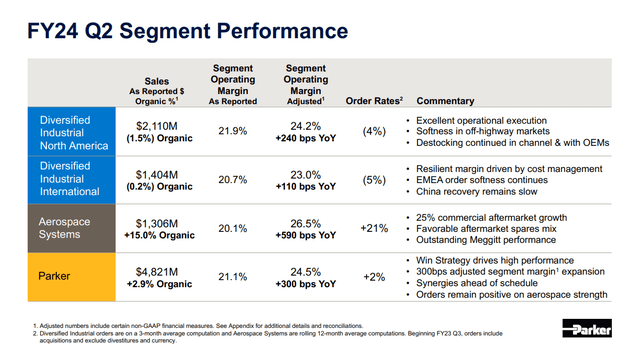

In the Diversified Industrial segments, the company experienced negative organic growth of 1.5% and 0.2% for the North America and International subsegments. Much of this was driven by ongoing destocking, a bit of channel rebalancing, and softness in off-highway markets. Specifically in the International part of the business, China’s recovery remains slow, so that put a hamper on sales here.

Despite fairly mediocre performance on the sales front, there were some positives that I think are worth mentioning. Firstly, margins improved as a result of expense management and cost efficiency improvements so segment margins increased 240 bps and 110 bps for the North American and International subsegments, respectively. Secondly, it should not have been a surprise to most investors who’ve been following the story as this quarter market its 4th consecutive quarter with negative orders now (for the North American segment).

What I believe to be the standout for the quarter is the performance of the Aerospace segment which experienced organic growth of 15% with 590 bps of margin expansion which brought the segment’s margin to a record 26.5%. Most of the cost synergies were as a result of the Meggitt acquisition announced a few years ago and this amounted to total synergies of $200 million. Another positive indication was that order rates are also increasing, up 21%, so this appears to be very strong growth for the aerospace segment.

Regarding my outlook going forward, I would say that the aerospace segment should continue to outperform in the quarters to follow, especially given the fact that order rates are trending higher and because backlog is strong at $10.8 billion. With guidance increased during the quarter for this segment, management expects to achieve $300 million in synergies by FY2026 .

As for the Diversified Industrial segment, with continued destocking, I don’t believe that the weakness in organic growth doesn’t seem all that bad considering that a few quarters ago it was much worse. In my view, we’re likely close to a bottom and my expectation would be that we see a recovery in the back half of the year, especially with stronger indications we’re seeing from the overall economy. Moreover, it’s likely that the gains from the aerospace segment should more than compensate for flat to slightly lower growth near-term for the Diversified Industrial segment.

Moving over to the balance sheet, at quarter-end, the company had a decent balance sheet with a leverage ratio of 2.3x and the company believes they are on track to bring that down to 2.0x by June 2024. With over $400 million of debt reduction this quarter, the company seems to be de-levering well. A good portion of this debt came from the acquisition of Meggitt and since that transaction in late 2022, the company has reduced the leverage ratio by 1.4x, reducing its debt load by about $2.2 billion. So in my view, with Parker-Hannifin’s ability to pay down debt quickly using cash flows generated by the business, it seems that the company will soon be ready for another major acquisition.

Valuation

Based on the 13 analysts who follow Parker-Hannifin’s stock, there are 10 ‘buy’ ratings, 2 ‘hold’ ratings, and 1 sell ratings. The average target price is $529.08, with a high estimate of $622.00 and a low estimate of $300.00 (source: TD estimates). From the current price to the average target price one year out, this implies about 3.7% upside, not including the current dividend yield of 1.2%.

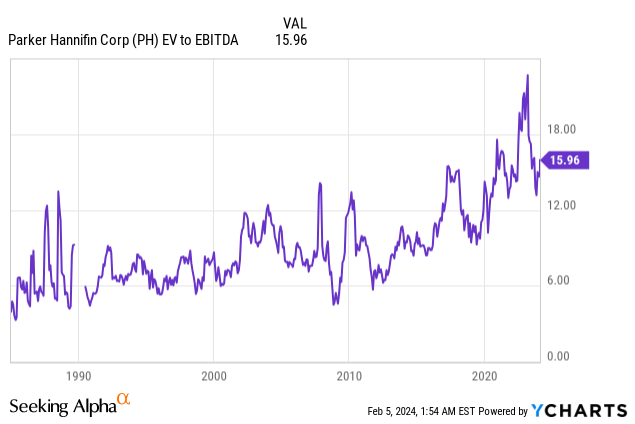

As with the rest of the market, the multiple of Parker-Hannifin has begun to creep up in recent time. At 16.0x EV/EBITDA or 25.2x P/E, the company’s shares don’t seem egregiously expensive. In fact, I’d argue that with margin expansion over time, the company has grown into its current multiple. While long-term revenue growth may be in the 4-5% range (based on what we’ve seen from the company historically), Parker-Hannifin should be able to grow its free cash flow and earnings per share faster as the company proves out margin expansion and repurchases shares.

As for the risks to my investment thesis, the main risk would be the cyclicality of Parker-Hannifin’s business, which is exposed to the booms and busts of the commercial aerospace industry in particular (38% of the Aerospace segment’s revenues). Selling to end-markets like construction and mining also has its risks as during recessionary periods, spending tends to drop and purchases for the company’s products would drop. In the last recession in 2009-2010, the company’s revenues fell 15.1% in 2009 and 3.1% in 2010, with margins contracting 260 basis points (source: S&P Capital IQ).

Another risk would be with the company’s acquisition strategy. While the market is focused on synergies and margin expansion generated from the recent acquisition, investors should also monitor the company’s restructuring expenses as these are real cash expenses that often go unnoticed in the calculation of adjusted EPS or adjusted EBITDA.

Conclusion

In summary, Parker-Hannifin has had a long track record of delivering exceptional returns to shareholders through a combination of steady revenue growth, incremental margin expansion, a disciplined M&A strategy, share repurchases, and a growing dividend. This quarter showcased mixed performance, with challenges in the Diversified Industrial segment offset by outstanding achievements in Aerospace. In my view, despite headwinds in certain markets, the successful integration of Meggitt has contributed to overall resilience along with remarkable 15% organic growth in the Aerospace segment. Margin expansion and a strong backlog should insulate the company’s profitability well with near-term weakness in the Diversified Industrial segment. With a reasonable valuation and a strong long-term outlook despite some temporary headwinds, I view shares as a ‘buy’ today.

Read the full article here

")

")

")