")

Q4 2024 Earnings Call Transcript")

")

Editor’s note: Seeking Alpha is proud to welcome Mencia Investment Research as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Summary

Jungfraubahn Holding AG (OTCPK:JFBHF) [JFN] is a Swiss-based ski conglomerate flying under the radar due to the lack of analysts’ coverage and the niche nature of its activities. The firm has a proven strong competitive advantage, cautious aligned management, financial strength, and a healthy rate of growth. I believe this firm presents a great opportunity for investors willing to diversify outside the mainstream markets. I currently expect high single-digit returns by investing in JFN’s equity. Investors should keep this name on their watchlist, waiting for future price pullbacks to start building a position in their portfolios.

Jungfraubahn Railway Service (Company Webpage)

Business Overview

Jungfraubahn Holding AG is located in Switzerland, a diversified company with the Jungfraujoch mountain region as a unique business model. The Jungfraujoch is located in the Bernese Alps, dividing the Cantons of Bern and Valais, with a peak elevation of 4158 meters. The complex includes the three prominent mountains overlooking the Interlaken region, the Jungfrau, the Mönch, and the Eiger. The company has a portfolio divided into divisions that offer visitors a full-year mountain experience.

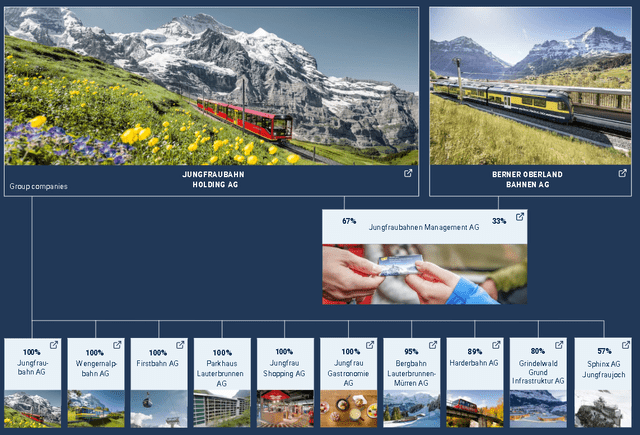

Company Structure

Jungfrau – Top of Europe is an alliance of the Jungfraubahn Holding and the Berner Oberland-Bahnen AG [BOB]. The objective of the alliance is to exploit synergies.

Jungfraubahn Holding AG and Berner Oberland-Bahnen AG jointly hold Jungfraubahnen Management AG (JFN 67% share, BOB 33% share).

The BOB operates the train from Interlaken Ost to Lauterbrunnen and Grindelwald, as well as the Schynige Platte Railway from Wilderswil to Schynige Platte.

Jungfraubahn Holding AG Group Structure (2023 Half Year Company Report )

JFN calls “Jungfraujoch Top of Europe” the division that includes the mountain infrastructure network. The company owns and manages several key railways on the mountain, providing access to the Jungfraujoch. This segment represented almost 60% of the company’s revenues in 2022. These assets include the original Jungfraujoch railway built in 1912, the highest railway station in Europe at 3,454 meters. Other remarkable assets are the Sphinx Observatory at an elevation of 3,572 meters and the Top of Europe building also located at a similar elevation; visitors can enjoy different panoramic restaurants, shops, and exhibitions among other features.

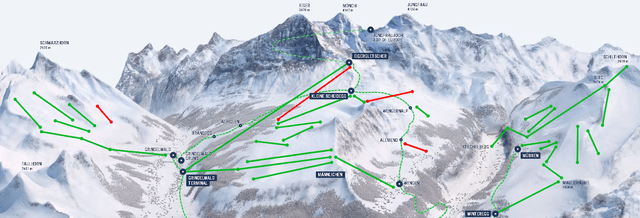

Jungfrau Ski region Overview Plan (Company Website)

The rest of the divisions, the so-called “Wintersports” and “Mountain Adventure” are segments that exploit the potential of the mountains. They represented 19.75% and 17.5% respectively of the 2022 revenue.

During winter, the company offers a portfolio of winter sports activities, including skiing and snowboarding, while in the summer months, the company offers experiences for more nature lovers.

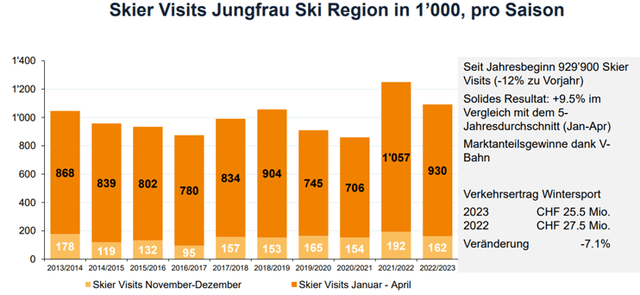

In 2023, more than 1million people visited Junfraujoch mountain region using JFN facilities and services.

Number of visitors per year during the Ski season (2023 Company investor presentation) Number of visitors per year during the summer season (2023 Company Investor Presentation)

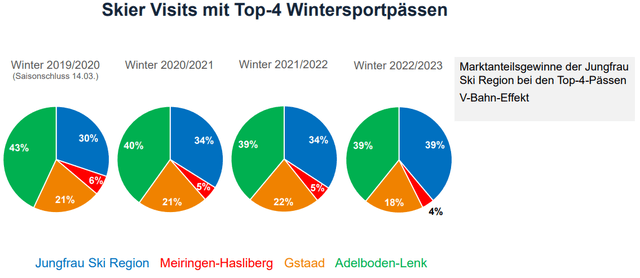

We can see how the winter sports and Mountain Adventures divisions have recovered and overcome the pre-pandemic number of visitors. Their investment in the V-cableway has played a crucial role. Their market position has gained a 9% share over the last 4 seasons against the other major four Swiss ski regions.

Top-4 Ski Swiss regions market share for the last 4 seasons (2023 Company Investor Presentation)

The company definition of the new V-cableway investment is the following:

“This new cableway increases the visitor capacity of JFN per day and gives clients the option to take a “fast lane” to arrive at the Top of the Europe area. Travel times will be significantly shortened and quality improved. The new winter sports facilities of international standard will get a direct public transport link with the new Berner Oberland-Bahn (BOB) railway station Grindelwald Terminal. At the Grindelwald terminal, including a car park, an extensive infrastructure with ski depots and shops will be available. The V-Cableway with its integrated components secures the medium- and long-term successful future of tourism throughout the Jungfrau Region as a top year-round destination in Swiss tourism. It strengthens the competitiveness of the Jungfraujoch as a beacon known worldwide, and it helps the winter sports destination reach the top position in international competition.”

Given the fact that the daily visit to the mountain region is a highly lucrative model for JFN, I am sure that the V-cableway investment will drive future earnings growth for JFN.

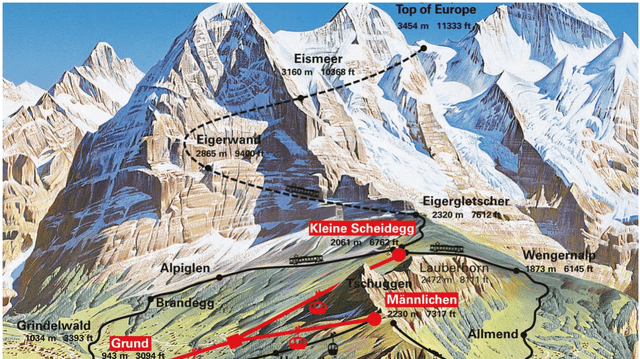

V-Cableway Path Overview over the mountain (Company Website)

The company also owns and operates a hydropower plant of 12MW of power. In 2023 the construction of an alpine solar power plant has been approved. This new plat will provide 12GWh for JFN railway assets and 3000 private households living in the area.

Alpine solar power plant (Company Website)

These two assets will provide the Jungfrau Railway with long-term independence from the energy grid and reduce its environmental footprint.

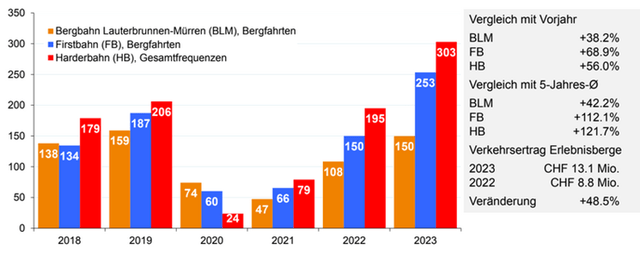

Additionally, they have two multi-store car parks. One is located in Lauterbrunnen with a capacity of 940 parking slots. Its location is strategic as it allows the visitor to transfer between the private transport and the car-free resorts of Mürren and Wengen. The other one is in Grindelwald Grund and it has over 1,000 parking spaces and charging stations. These assets provided around 22.75% of the 2022 revenue.

Car Park assets (2023 Company Investor Presentation)

Financial Position & Performance

Units expressed in millions of Swiss Francs:

P&L:

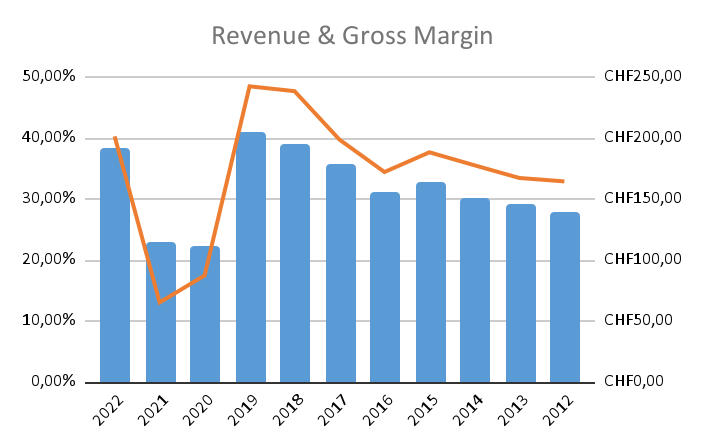

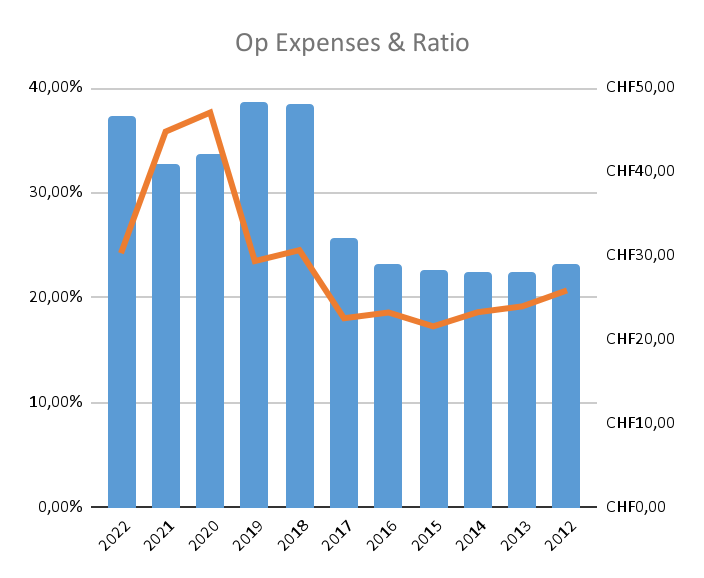

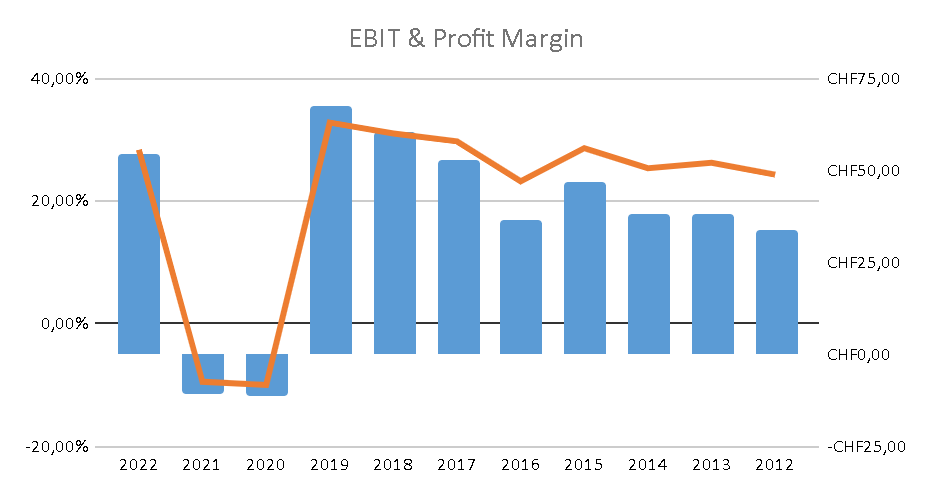

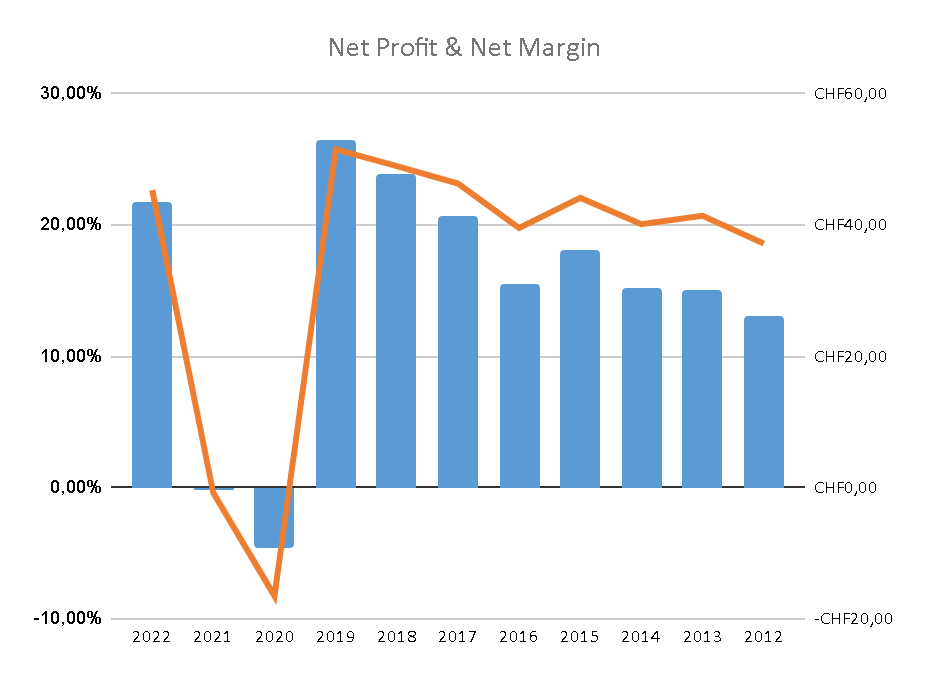

Revenue & Gross Margin (Data taken from Company Financial Reports) Operating Expenses & Expenses/Revenue ratio (Data taken from Company Financial Reports) Operating Margin & EBIT (Data taken from Company Financial Reports) Net Profit & Net Margin (Data taken from Company Financial Reports)

The company has managed to grow the top and bottom lines of the business each year for the last decade if we exclude the COVID lockdown period as it was an external event. Even during the 2022 period, the Asian lockdowns affected the company’s numbers as the visitors from that area of the world are a group that contributes substantially to the firm income.

The stable and increasing profit margins that this company shows reflect the competitive advantages or “moats” that this business model presents.

As for the latest results from H1 2023, Jungfraubahn Holding AG showed the following numbers:

Revenue: 132.5 million CHF a 35% increase from H1 2022.

EBIT: 44.3 million CHF with an operating margin of 33.5%

Net Profit: 35 million CHF with a net profit margin of 26.4%

Number of visitors: 419000 in H1 2023, -11% than in 2019 but in the path to recover the pre-pandemic numbers.

Balance Sheet

The balance sheet shows how the management is conservatively running the company. It has almost no goodwill or intangible assets and as per the latest H1 2023 report. It has less than 1 million CHF in debt and circa 39 million CHF in cash & equivalents. This leaves the firm in a net cash position.

The board has been able to grow the equity value at a 4% CAGR in the last 10 years. The liquidity ratios also indicate a healthy short-term horizon for the firm.

The company is practically isolated from the interest rate fluctuation which enables the firm to pursue new strategic investments to fuel the growth.

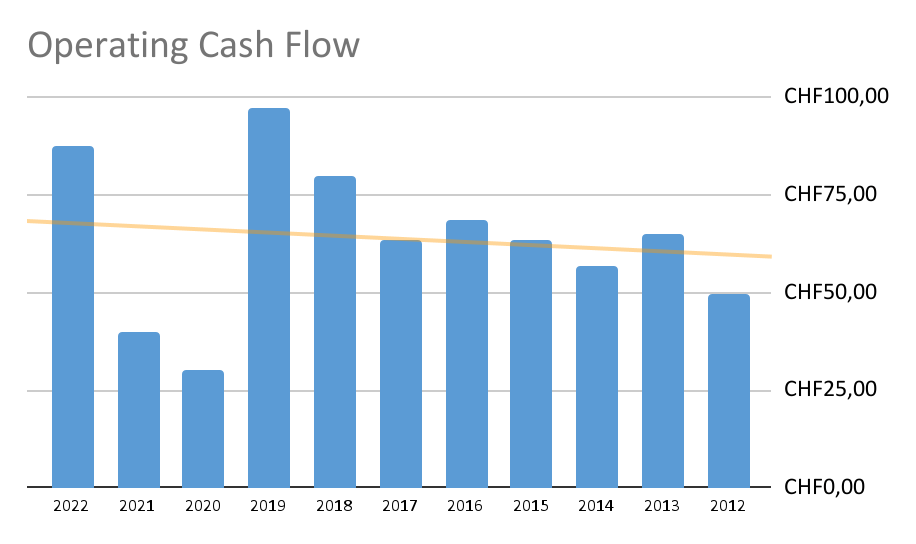

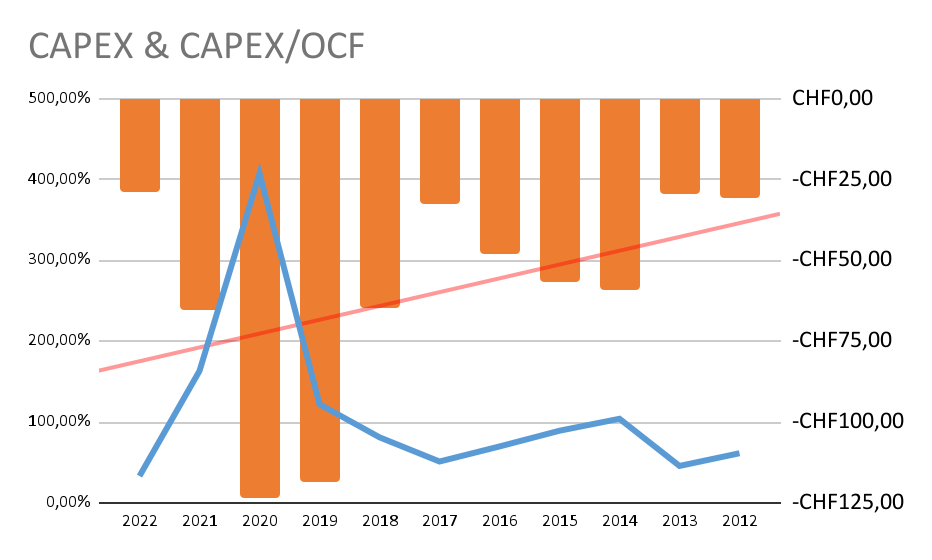

Cash Flow Statement

Operating Cash Flow (Data taken from Company Financial Reports) CAPEX & CAPEX/ Operating Cashflow Ratio (Data taken from Company Financial Reports)

The operating cash flow has grown at a CAGR rate of 5% for the last ten years. In 2022, the company managed to recover to catch up with the last OCF pre-Covid pandemic in 2019.

The Capex graph shows the V-cableway investment cycle starting with the works in 2012 and finishing in 2022 although the cableway was officially opened at the end of 2020. I expect that the 2023 Capex will be similar to the one in 2022.

The shareholders have been rewarded in the last ten years by JFN with dividends growing at a CAGR of 7%. The amount of shares in circulation is almost the same with a CAGR rate of 0.004% in the last 10 years.

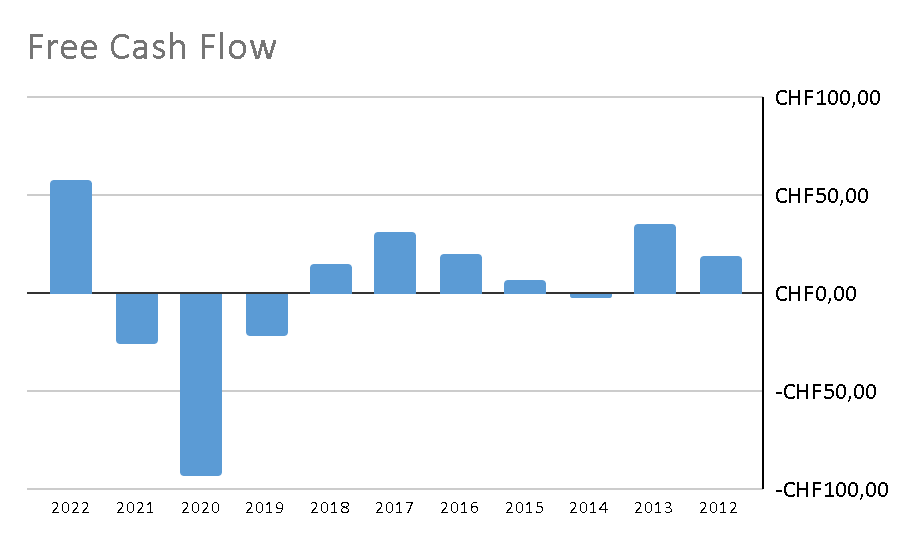

Free Cash Flow (Data derived from Company Financial Reports)

The free cash flow (FCF) has grown at a CAGR rate of 8% for the last ten years. In 2022, the company managed to recover and hit a record FCF due to the end of the V-Cableway investment and the recovery of the business after the pandemic.

Company’s Key Financial Information

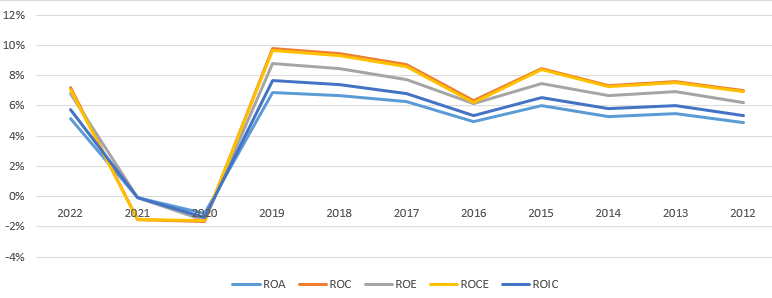

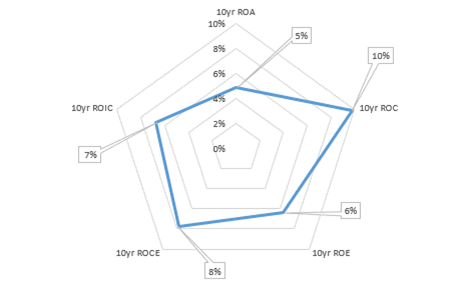

Historical Key Return Ratios Graph (Data derived from Company Financial Reports) Radar Chart of the 10-year average key return ratios (Data derived from Company Financial Reports)

We can see how during the last 10 years the company has delivered an average rate of return over the capital employed of 8% and a return on equity of 6%. This is an acceptable rate of return given the business model type and coming out from the pandemic period. If we look to 2019, we can see how back then the ROCE and ROE were 10% and 9% respectively. In my opinion, these rates of return could move higher in the coming years as the V-cableway investment will improve both the top and bottom line of the firm, helping to increase the return metrics.

Relative Valuation Metrics

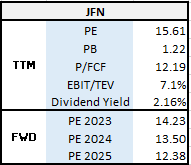

The stock is currently trading at a TTM price to earnings (P/E) of 15.61 and has a dividend yield of 2.16%. I expect the dividend to be increased this year fueled by the earning growth and ending of the CAPEX cycle. The current price-to-book value is 1.22. If we look at the Trailing Price to Free Cash Flow (P/FCF), it is currently 12.19.

The 10-year average PE is 15.63, the dividend yield of 2.35%, the price-to-book value is 1.2 and the P/FCF is 11.52 this means that currently, the stock is trading in line with the historical valuation.

Trailing and Forward JFN Multiples (TIKR website)

Currently, analysts forecast an annual growth CAGR rate of around 8%. The expected P/E ratio for the period from 2023 to 2025 is 14.23, 13.5, and 12.38 respectively for the current share price. Analysts expect JFN to have strong growth due to the end of the COVID-19 pandemic period and the entry into service of the V-cable.

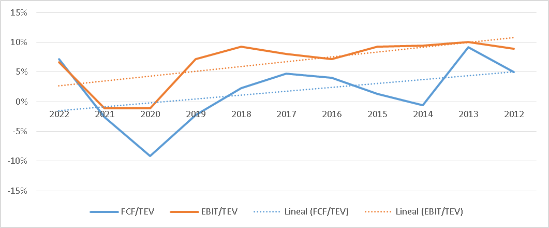

Historical Graph of Valuation Metrics (Own Analysis)

The graph above shows how the valuation ratios of EBIT/Total Enterprise Value (TEV) and FCF/TEV have evolved over time and currently are sitting at a value of EBIT/TEV: 7.1% and FCF/TEV: 7.61%. I prefer to value companies with these ratios, as they offer a more well-rounded idea of the price that we are paying for the business.

Growth Metrics

JFN has shown high-quality stable growth over the last 10 years. The average CAGR growth rate is 4.2% combining top and bottom line growth, and also including the equity growth, which is a good sign of the value created for shareholders.

Talking about growth quality, the company has been able to have stable growth in the 10 years, they have managed to grow 70% of the time on average.

Valuation

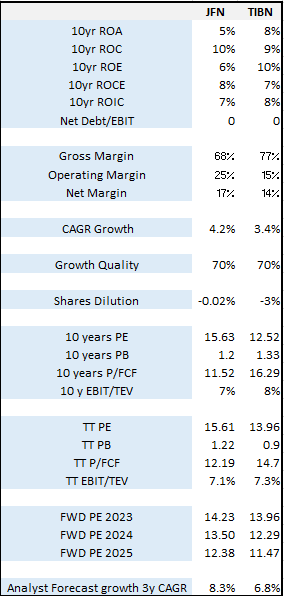

Relative Valuation Against Peers

This chapter performs a relative valuation against a similar company operating in the same sector and type of business and geographical area. The selected company is Bergbahnen Engelberg Truebsee Titlis AG (BRGBF) [TIBN]. It is a Swiss ski conglomerate operating on the Titlis mountain, at an elevation of 3,238 meters. I have selected this company because is another publicly traded Swiss ski conglomerate trading at the SIX. TIBN is located on the border between the Obwalden and Bern cantons. Titlis and Junfraujoch mountains are at a distance of around 150 kilometers by car.

TIBN is a much smaller company with a market cap of 144 million CHF, an annual revenue of 72 million CHF, and around 1 million visitors per year. Their revenue mix is 51% representing the mountain services as the railways, and daily/ski visit tickets, among others. 32% comes from the gastronomic segment and 17% comes from the Hotel segment.

The image below shows how the profitability ratios and valuation metrics stand one in front of the other. Although in some aspects TIBN has better numbers, for example, a higher ROIC, ROA, or ROE. The comparison between margins shows how JFN has a superior capacity to translate revenue into bottom-line profits.

Relative Valuation Comparison (Own Analysis)

They also show a similar dilution share rate and growth quality. Both companies trade at a similar TTM EBIT/TEV ratio which is my preferred valuation ratio.

JFN has a more diversified well-positioned portfolio and a scale competitive advantage. For example, the higher elevation of the Jungfraujoch mountains allows an all-year ski season. Instead, Titlis Mountain only allows visitors to ski from October to May. These factors, together with the entry into service of the V-cable enable JFN to have a higher rate of growth in the near future and to trade with a higher multiple.

I believe that the market understands that the size advantage and asset quality of JFN create a more compelling investment than TIBN.

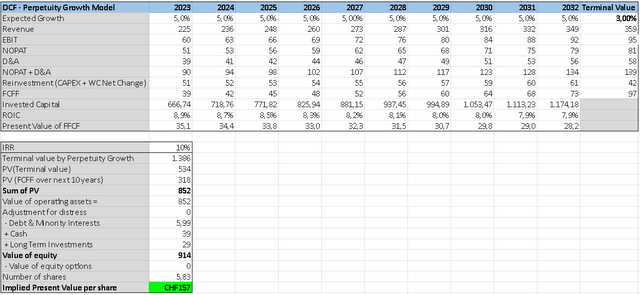

Discounted Cash Flow Valuation

In the valuation chapter, a discounted cash flow (DCF) analysis using the perpetuity growth model is performed to assess the intrinsic value of the business and, therefore, the stock. The analysis looks at the free cash flow of the firm, as wants to extract the business valuation.

Inputs

Revenue growth: 10-year average of 4.2%. We expect a higher growth given the V-cable investment. We take the 5% rate as the most probable rate of growth. The perpetual rate of growth selected is 3%.

EBIT Margin: 10-year average of 26.5%

Tax Rate: 15%

Reinvestment Rate: 10-year average of 0.3.

Investment Rate of Return (IRR): 10%, for me this is the standard rate of return for an international investor.

DCF Valuation (Own Analysis)

The DCF calculation gives a target share price of 157 CHF for investors looking to get a 10% return on their investment. This number validates my view that currently the shares are trading at a fair price.

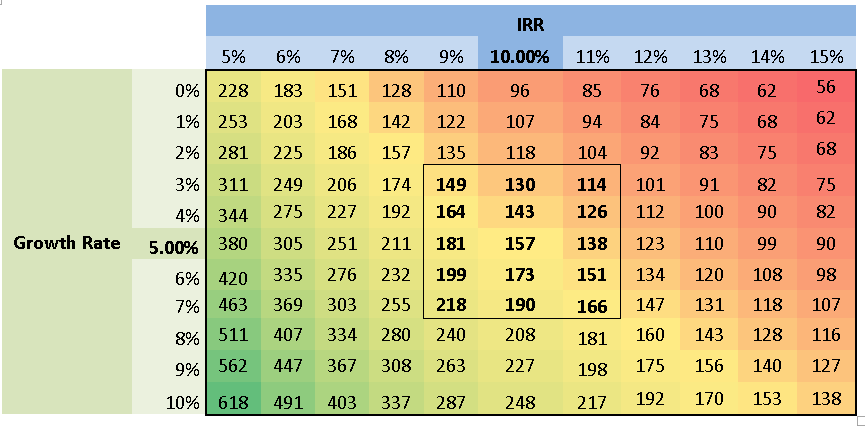

Sensitivity Analysis

To add an extra layer of precaution, I run a sensitivity analysis to understand the impact of changing some assumptions on the valuation. The IRR and the rate of growth are the variables. In this way, the simulation can take into account the variation of the interest rates and how these changes affect the result in combination with the growth rate.

The conclusion is that the market is currently pricing a rate of return of around 9% with a growth rate between 4% and 5%. If investors think that these assumptions are appropriate, the stock would be a buy for them. In my case, I prefer to add some margin of safety to the buy calls, requiring at least a 10% IRR and the projected growth of around 4-5%, leaving the entry point around 5-10% below current stock price levels. It is very plausible that the stock will touch those levels in the short-medium term if general market volatility increases given the scarce liquidity of the shares.

Sensibility Analysis Graph (Own Analysis)

Looking Forward

SWOT Analysis

Strengths

Diversified Business Model: The company’s portfolio includes high-quality infrastructures, real state, and other tangible and intangible assets, a complete activity portfolio for both winter and summer seasons. The firm has the capacity to produce its own electricity, reducing the environmental impact of its activities and being independent of energy price fluctuations. The firm is vertically integrated, reducing costs and maximizing growth opportunities.

Management & Financial Strength: Proven aligned management and financial robustness provide stability and resources for ongoing operations and future investments.

Weaknesses

Dependency on Seasonal Tourism: Reliance on seasonal activities, winter sports, and mountain adventures, exposes the company’s revenue during off-season periods.

Weather Dependency: Weather conditions affect the visitor numbers and the feasibility of certain activities.

Opportunities

Tourism Growth: Continued growth in the tourism industry especially from emerging areas of the world like China and India presents an opportunity for JFN to attract more visitors and expand its customer base. This firm is well positioned to capture the increase in the income per capita from emerging countries in the coming years offering an appealing unique vacation destination.

Technological Innovations: Investing in technological advancements in transportation and visitor experiences can keep JFN’s market position and competitive advantages.

Business expansion: Expanding the business through inorganic growth, acquiring other Swiss sky complexes. To increase and improve the efficiency of the railways to gain a higher number of visitors and therefore revenue.

Threats

Economic Downturns & FX movements: Global economic downturns would affect discretionary spending on travel and tourism, translating into a decrease in revenue and profitability of the company. FX movements could also affect the suitability of international investors. Although the Swiss franc tends to be stable and behave well against other currencies during macro instability, the historical appreciation of the currency could be inconvenient to certain investors.

CEO Stepping Down: In 2023, it was announced that the current CEO, Urs Kessler will step down from his office as Chief Executive Officer after the General Meeting of Jungfraubahn Holding AG in June 2025. Kessler has been with Jungfrau Railways for 36 years and served as Chief Executive Officer for the last 15 years. This decision was already shared by Mr. Kessler some time ago when he confirmed that he would leave the company when the V-Cable project would be finished. Unfortunately, COVID-19 came and his departure had to be postponed to 2025.

Climate Change: The consequences of climate change could pose a threat to JFN’s core business model in the very long term.

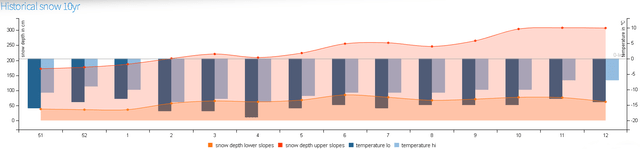

Related to this point, I would like to indicate that in the last ten years, the average amount of snow that the Jungfraujoch mountain region has registered is the following:

Historical Snow in Jungfraujoch Region (Skiweather.eu)

In the last 4 seasons and the current one, the data is the following:

Snow level in the last 4 seasons, Jungfraujoch Region (Skiweather.eu)

In the last 10 years, this mountain region has had at least 50 cm of snow in the lower mountain levels and almost 200 cm in the higher parts. Given all the recent scientific studies claiming that the last recent years have been to hottest in Europe in recent history, I believe that the Jungfraujoch mountain region will avoid for the foreseeable future the risk of not having enough snow to perform their business activities.

During seasons 2022 and 2023, the snow levels were the lowest of the last 5 years. Despite this fact, JFN managed to generate 169 CHF million in 2022 and 132 CHF million in the H1 of 2023. This means that the firm can generate and increase its revenues despite lower levels of snow and adverse weather, thanks to its high-quality diversified asset portfolio.

Future Growth

Regarding future growth potential, I would like to look at the historical data and see how the company has been able to grow its business from 2010 to 2022. This period includes the GFC, the European debt crisis, and the pandemic crisis and shows how resilient the business model of JFN is.

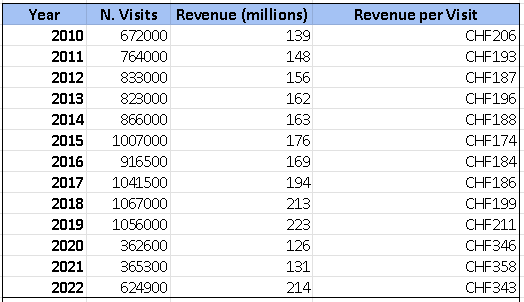

For that, I use the ratio of Revenue per Visitor as I want to see how the company has been able to include the inflation and increase the turnover per visitor in a 10 year period.

Historical Revenue per Visitor Table (Own Analysis)

The company managed to increase the revenue per visitor with a CAGR of 4.3% per year for this period. The firm has been consistently able to place the inflation in their prices. This chart proves that JFN’s business model is inflation-proofed and their competitive advantages allow the firm to increase prices without hurting the number of visitors.

For all the points shown above, I believe that JFN will manage to exceed the historical growth rate and grow at a stable rate of 5% for the next years, thanks to the new V-cableway investment, which will drive an increase in the yearly number of visitors of the Jungfraijoch mountain region.

Conclusion

In conclusion, Jungfraubahn Holding AG is a unique well-rounded business. This company is the perfect example of a hidden quality firm flying under the radar. JFN has the main characteristics that investors love to see when analyzing a company. Some of them are the following:

- The financial strength of the firm.

- A business with proven competitive advantages and inflation protection during extended periods of time.

- The company has a proven, prudent, and aligned management.

- The business is growing at a steady and healthy rate with tailwinds to support the future and a similar progression path.

- The historical stock price appreciation shows how this firm delivers value year after year to its shareholders.

Jungfraubahn Holding AG offers a strong, stable inflation-protected quality business, giving investors a good way of diversification away from the main markets and sectors. I consider this stock a buy & hold until the business conditions change given its characteristics and the sector where it operates.

I believe that shares are fairly priced currently. New investors should keep this name on their watchlist, waiting for future 5-10% pullbacks due to market volatility or macro concerns to offer them an appropriate margin of safety to add this name to their portfolios.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")

")