")

Investment Thesis

In spite of my pen name, a non-dividend-paying growth business can still catch my interest if the investment thesis is compelling enough. First Solar (NASDAQ:FSLR) is an example of such a business, and I currently rate the stock a Buy because I believe that the current stock price offers a reasonable valuation for a high-quality, high-growth business with some margin of safety.

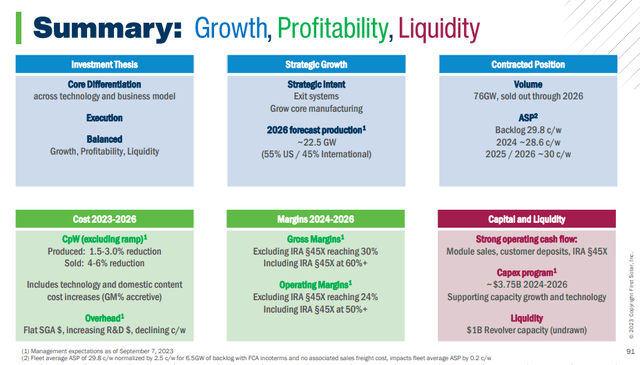

There are many reasons why I like First Solar and why I recently added to my position. First, the company is expected to deliver significant revenue and earnings growth over the next several years as it invests heavily in ramping up its manufacturing capacity as well as its research & development (R&D) capacity to meet strong demand for its products and technology. These investments are being funded primarily via the company’s cash on hand, prepayments from customers, and operating profits which is keeping the company’s debt relatively low. First Solar’s manufacturing cost structure is also largely fixed, allowing it to take advantage of operating leverage as it ramps up its capacity and sales. Furthermore, the company’s backlog is sold out through 2026 and now extends into 2030, securing the majority of its growth in the next several years as long as it executes.

Additionally, First Solar is taking advantage of many tailwinds including benefits from the Inflation Reduction Act (IRA), which is boosting its gross margins and increasing customer demand for the company’s products. The company has been divesting its legacy O&M business to focus on its core competency of designing, manufacturing and selling Cadmium telluride (CdTe) solar modules while it continues to invest heavily in innovating and developing new technology as well. In addition to the USA, First Solar is also pursuing attractive opportunities in countries/regions such as India, Malaysia and Europe as some of these regions have and are continuing to enact regulatory, environmental and tax policies that are providing First Solar with favorable growth opportunities.

Overview (First Solar Analyst Day 2023 Presentation)

That said, the investment thesis does face some significant risks, namely political risk, intense competition, supply risk (tellurium) and risk of the business executing its aggressive growth plans successfully. However, I believe that the business is well-positioned to manage these risks and that the current stock price (around ~$149 per share as of the time of this writing) makes FSLR is a buy at current levels.

High Growth Outlook

The solar energy industry is expected to grow at an attractive 12.3% CAGR through 2032 and is likely to continue to grow well after that as nations work to decarbonize their economies. First Solar’s growth path looks like it will be even higher:

Expected growth through 2026 (FSLR Guidance, Author’s Forecast Model, and Consensus Estimates)

As shown above, First Solar’s revenue is expected to take off over the next few years as new manufacturing capacity comes online and allows the company to produce and sell its solar module backlog which is already stretching into 2030. In fact, First Solar has already sold out its capacity through 2026, bringing a reasonable level of confidence to the above growth forecast as long as the company executes its ramp up plan.

To support this demand, First Solar has been aggressively investing in its manufacturing capacity, with several new plants recently launched or in the works:

- 3.3 GW Facility in India was inaugurated in January 2024

- Expanded capacity at existing Ohio manufacturing facility expected in first half of 2024

- Fourth US manufacturing facility expected in second half of 2024

- Fifth US manufacturing facility expected in late 2025

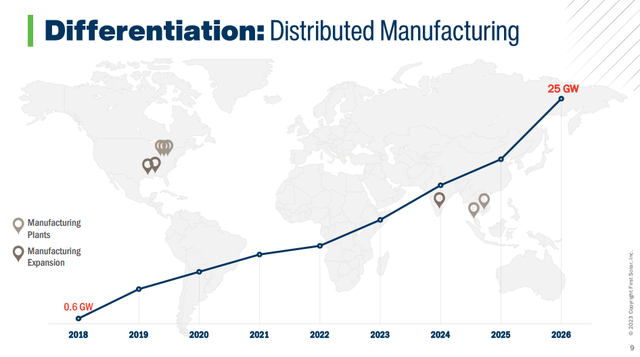

As these new facilities come online while capacity at existing facilities is increased, First Solar’s overall capacity is expected to grow to 25 GW by 2026 as shown below:

FSLR Manufacturing Capacity By Year (First Solar Analyst Day 2023 Presentation)

First Solar chooses the locations of its manufacturing facilities strategically to take advantage of local subsidies and tariffs in countries such as the USA and India. For example, the IRA provides credits for domestic US solar manufacturers such as First Solar, and India is also providing attractive incentives to solar manufacturers who produce modules locally for use in India. The company is also receiving tax holidays and incentives in its Malaysian and Vietnamese subsidiaries that make production attractive in those countries. The company continues to watch for opportunities to continue to expand its operations where it makes sense to, with regions such as the European Union providing the potential for future opportunity.

Why is demand for First Solar’s products so high that developers are booking orders as far out as 2030? The company’s CdTe technology differentiates it from the majority of its competitors who produce crystalline silicon panels. First Solar is the world’s largest manufacturer of CdTe panels, which can be produced quickly and at relatively low cost. According to the company’s 2022 10-K:

In addressing the overall global demand for electricity, our modules provide energy at a lower levelized cost of electricity (“LCOE”), meaning the net present value of a system’s total life cycle costs divided by the quantity of energy that is expected to be produced over the system’s life, when compared to traditional forms of energy generation.

Furthermore, First Solar focuses primarily on utility-scale markets as opposed to residential, and utility developers find First Solar’s LCOE and its warranties very attractive:

FSLR Value Proposition (Company website)

The company is also the largest manufacturer of solar panels (not only CdTe) in the Western Hemisphere, which gives it a competitive advantage in scale and also positions it very well to benefit from programs like the IRA.

First Solar’s R&D Is Growing Too

While First Solar is already a leader in CdTe module technology and manufacturing, it is not sitting still on the research and development front: high investment in R&D continues, expected to increase approximately 10% per year for the next several years. In addition to investing in several new manufacturing facilities, the company is also building a new $270M R&D facility in Ohio expected to open in 2024. This new facility will feature a pilot manufacturing line for the development and production of thin-film prototypes.

Furthermore, FSLR’s $38 million acquisition of Evolar, a Swedish research and manufacturing startup specializing in perovskite technology, in May 2023 offers high potential for synergies with First Solar’s own R&D as the sheet-to-sheet method of producing thin-film CdTe seems to be one of the methods of scaling high-efficiency perovskite solar cells with the highest potential. This is an example of an exciting opportunity for First Solar to gain a further lead against its competitors and shows that the company is focused on the long-term picture and is not complacent with its competitive position.

The company’s R&D expense is approximately 5% of expected 2023 revenues and expected to decrease as a percentage of revenue as sales growth outpaces R&D requirements.

Low Reliance on Debt Reduces Risk

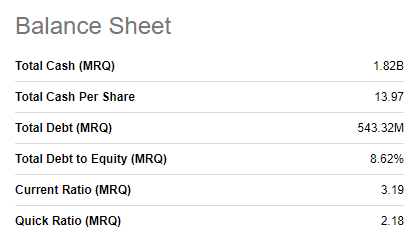

While the company is investing heavily in PP&E, some very good news is that is not taking on very much debt to do so. The company currently has a strong balance sheet with $1.82B in cash and cash equivalents and only $543M debt, most of which is against its India Credit Facility in support of its new India plant:

FSLR Balance Sheet (Seeking Alpha)

There are two primary reasons why the company has been able to keep its debt relatively low. First, one of the advantages of selling out its capacity through 2026 and partially into 2030 is that many customers have prepaid cash to book that capacity, which is why FSLR shows a liability of deferred revenue totaling $1.72B on its balance sheet. This is important to be aware of because a portion of the company’s recognized revenue over the next several years will not result in additional operating cash flow. However, with revenue expected to reach $6.75B by the year 2026 with significant margin expansion, there should be plenty more operating cash coming into the business. These cash prepayments have helped to fund the company’s growth and, in the current interest rate environment, have allowed the company to earn some interest on its cash balance instead of paying interest on a high debt balance. In other words, the cash advances from customers have created a type of float for First Solar that allows the company to invest heavily in its growth without incurring significant leverage risk.

Admittedly, this does still create execution risk because these customers are expecting the company to deliver their orders within a reasonably expected time frame and of course meeting quality and efficiency standards. It is also worth noting that First Solar’s current cash balance represents $13.97 per share, approximately 9.5% of the current stock price, which makes the current valuation more attractive.

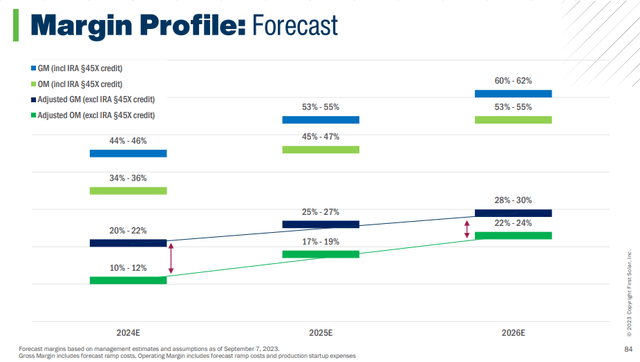

The second reason why the company has been able to keep debt low is that First Solar is already generating an attractive operating profit (which I expect to be ~22% in 2023) thanks to credits and grants from the IRA, and this profit is expected to increase considerably over the next few years:

Margin Profile Forecast (First Solar Analyst Day 2023 Presentation)

According to the company’s 2023 Analyst Day Presentation, it expects to spend $3.75B on CapEx 2024-2026.

With 20%+ annual revenue growth and operating margins approaching 50%, the company should be able to continue to fund its expansion and growth without needing to become highly leveraged.

Interestingly, the company announced in early January the sale of $700M of advanced manufacturing tax credits to fintech company FISERV, who agreed to pay 96 cents on the dollar for the rights to these credits. Such deals provide First Solar with faster and more certain liquidity as it doesn’t need to wait to receive the credits from the government.

Relatively High Fixed-Cost Structure Facilitates Operating Leverage As Company Grows

As explained in the company’s 2022 10-K, the company’s manufacturing lines use highly-automated continuous flow as opposed to batch processing. This type of production line is very desirable when you are able to scale your business rapidly because a significant portion of the production cost becomes fixed which fosters operating leverage. This is a significant contributor to the expected boost in First Solar’s gross margin and operating margin as was shown above.

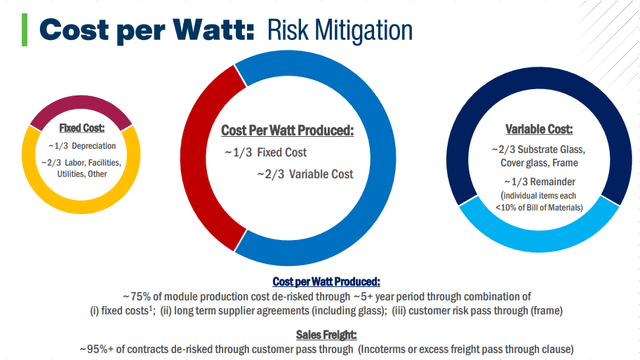

Of the variable production costs, over two-thirds is from input materials. In order to achieve its margin goals, the company must control the cost of these materials. Fortunately, it is doing just that via long-term supply agreements.

Long-Term Supply Agreements Further Mitigate Risk

Cost Risk Mitigation (First Solar Analyst Day 2023 Presentation)

First Solar has entered long-term supply agreements (5+ years) for the majority of its key production materials as well as favorable customer contracts that pass through many of the variable material and freight costs to customers helps to lessen First Solar’s margin risk.

Thus, not only is the company’s revenue growth essentially “locked in” through 2026, but many of its production costs are as well.

Risks

Political Risks

First Solar is a very strong beneficiary of the Inflation Reduction Act (IRA). The IRA offers the Advanced Manufacturing Production Credits under Section 45X of the Internal Revenue Code, and these credits are already significantly reducing the company’s Cost of Goods Sold and expected to reduce them through 2032. Additionally, the IRA offers Investment Tax Credits that are helping to boost demand for First Solar’s products. Partial or full repeal of the IRA, particularly after the 2024 US Election, would greatly reduce (although not eliminate) First Solar’s profitability.

I am generally very cautious to invest in a business that is heavily dependent on government subsidies. However, in this case I am cautiously comfortable. First, I think that the IRA, or even just the Section 45X tax credits, is unlikely to get repealed, especially in full. It would appear that Republicans would need to control the House, the Senate, and the Presidency to have any chance at repeal. Even then, I doubt that they would repeal the credits in full. These credits are providing significant financial benefits to many American businesses and helping companies like First Solar to compete against Chinese counterparts, which is something that politicians on either side of the aisle would be very cautious to take action against. In my opinion, appearing to do something that hurts American businesses while helping China would not look good to many Republican voters.

Second, even in the worst case scenario where the Investment Tax Credits get repealed, this repeal would not happen until at least 2025. By then, the company’s gross margin should reach 25% even without the benefit of the tax credits while its operating margin reaches at least 17%. The company’s profits would take a hit, but the company would still be reasonably profitable, and these margins would continue to increase as the business’ worldwide operations continue to scale. The company will have already earned a nice profit in 2024 if it executes on its operations, and likely a portion of 2025 as well, with much of its three-year CapEx already funded.

Intense Competition

While demand for solar modules is growing quickly, so is the supply. First Solar has many competitors that produce different types of solar panels, and they compete on cost, efficiency, and overall environmental impact (such as recyclability). The IRA helps to make First Solar more competitive relative to Chinese competitors, and changes to the IRA or to current tariffs on Chinese-produced panels could pose significant challenges to First Solar’s ability to compete profitably. Additionally, the threat of new technologies could make First Solar less competitive if it does not continue to innovate with its own technology.

Scarcity of Tellurium Supply

As the world’s largest manufacturer of CdTe solar modules, First Solar is critically dependent on supply of the metal tellurium which is a by-product of refining copper and as rare in the earth’s crust as platinum. North of 60 Mining News wrote an interesting article about this topic last updated 9/13/2023. In summary, the Department of Energy (DoE) is certain that supply constraints are likely starting in the 2025-2035 timeframe, with First Solar’s capacity ramp up the single largest driver of this phenomenon. Other renewable energy technologies including battery storage are expected to increase overall demand for tellurium as well. Currently, two-thirds of supply is generated by China and Russia with limited domestic production.

However, as explained in the article linked above, First Solar is partnering with the DoE and with domestic suppliers to mitigate this risk by increasing the domestic supply while controlling demand through the development of more efficient technology that reduces the amount of tellurium required in each solar panel. Multiple US and Canada based companies are exploring and implementing opportunities to identify domestic sources of tellurium and ways to produce it cost-effectively. The current US Government administration is also highly supportive of First Solar’s efforts and is working with them to help reduce this risk of supply constraint. Furthermore, demand for copper is expected to increase as the result of increased investment in the US electric grid, and this in turn is expected to be favorable to the supply of tellurium.

Thus, First Solar’s management is confident enough to continue onward with its expansion plans. Nevertheless, this is still a key risk for investors to watch. It is also worth noting that even if supply of tellurium does not run out that the price could still skyrocket if demand outpaces supply over the next decade and beyond which could impact First Solar’s gross margins.

Execution Risk

I have enough experience in the world of manufacturing to know that things do not always go to plan, especially when commissioning new buildings, new equipment, and new manufacturing lines. As I’ve already discussed, First Solar has very ambitious growth plans, but these plans are dependent on the successful implementation and ramp up of several new facilities as well as upgrades at existing facilities which presents a significant risk that the company could run into a number of problems that threaten its timeline, its achieved capacity/throughput, or its quality of production.

So far, the company has kept on schedule and delivered results, so I am reasonably confident in management’s ability to execute its plan. That said, I believe it is important for investors to consider this risk which could impact revenue, margins and the company’s reputation. Delays in opening new plants or expanding existing plants could impact First Solar’s ability to deliver on its high revenue growth.

Valuation

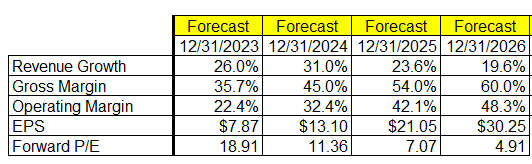

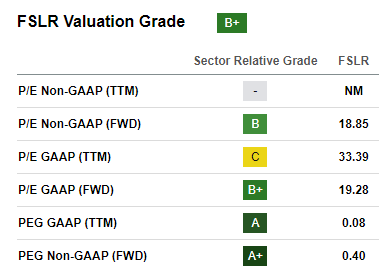

With EPS expected to nearly quadruple to more than $30 by FY 2026, the forward Non-GAAP PEG ratio for FSLR is only 0.40, which is very low and earns it an A+ in Seeking Alpha’s grading system:

FSLR PE and PEG (Seeking Alpha)

Yet as an investor, I only consider PE and PEG ratios to be a relatively small piece of the valuation puzzle because they don’t always tell the full story. I am a big fan of DCF models because they consider expected cash inflows and outflows to equity discounted to Net Present Value.

DCF models can sometimes be challenging for high growth businesses, but in the case of FSLR where so much of its sales capacity is already booked for the next several years and where I have reasonable confidence in its margins assuming no surprises from the IRA and related tax credits, I prefer to use this type of model to evaluate whether FSLR is a good buy at today’s prices. The other advantage of a DCF is that it allows you to test different assumptions for sales growth, margins, and other factors such as interest expenses and tax rates to see how they impact today’s estimated fair value.

When in doubt about an assumption, I like to err on the side of safety.

Without further ado, let’s get into it:

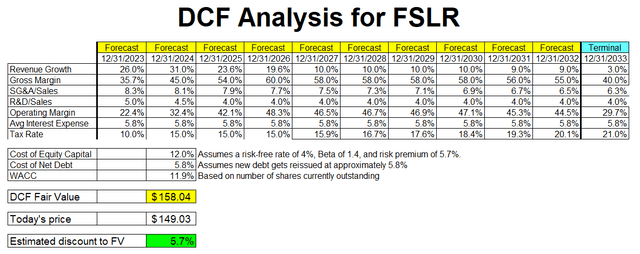

DCF for FSLR (Author’s DCF Model)

My DCF model shows FSLR as approximately 5.7% undervalued based on today’s price, offering a modest margin of safety.

Revenue growth and gross/operating margins through 2026 are forecasted using a combination of company guidance and consensus estimates (driven by the company’s capacity expansion plan and currently-booked capacity).

With the company’s revenue growth being less certain after 2026, I reduced my revenue growth forecast to 10% starting in 2027 which is modestly lower than the overall industry’s expected 12.3% CAGR through 2032. I used a terminal growth rate of 3%; I very rarely go higher than a 3% terminal growth rate in DCF models as doing so often overstates the current fair value in my experience.

I held gross margin at 58% after 2026, dropping modestly after 2030 and down to a terminal gross margin of 40%. This reflects the expected expiration of credits from the IRA and other subsidy sources partially offset by efficiencies gained via operating leverage and continued improvements in the company’s technology.

I forecast operating margin to follow suit – decreasing modestly after 2030 with a terminal rate of 29.7%, the decrease driven primarily by my forecasted drop in gross margin. I expect the company to continue to ramp its R&D expense, but I expect sales growth to continue to outpace it.

I left average interest rate expense at the current 5.8% but also don’t expect the company to incur a significant amount of debt unless it decides to alter its overall capital structure down the road as the company matures.

The effective tax rate is trickier to forecast. For Q1-Q3 2023 the effective tax rate was 6.4%, so I went with 10% for 2023 to be safe and increased to 15% starting in 2024 with gradual increase to 21%. I think the company’s actual tax rate will likely be lower, but I feel my numbers help to provide a little extra margin of safety.

I used a 12% discount rate which is higher than I use for most businesses but in my opinion fair given the company’s risks.

I think FSLR is a Buy at today’s price of ~$149 and would be a strong buy if it were to drop below $135 barring any bad news. On the flip side, I think it becomes a hold over $165-$170 barring any good news.

The price action of FSLR is relatively volatile, and I expect that to continue. This will likely provide opportunities in the near term to “buy the dip”. The company is expected to report earnings on February 27, and investors (myself included) will be watching closely to see how well the company is executing on its growth and its ramp up plan.

FSLR One Year Chart (Seeking Alpha)

Conclusion

First Solar is riding many tailwinds that are fueling high growth and operating leverage, and while the company faces some significant risks these risks are either being largely mitigated or are unlikely to happen. I think the risk/reward balance is attractive at today’s price and rate FSLR a buy.

Read the full article here

")

")