")

")

Zimmer Biomet’s (NYSE:ZBH) stock has been under pressure over the past few years, which appears to be at least in part due to concerns over the impact of GLP-1 agonists. This fear appears to be misplaced though, as it will likely be decades before any negative impact will be felt. In addition, GLP-1 agonists should provide a near-term tailwind by making more patients eligible for surgery. Joint replacement procedures have been increasing 5% annually, and even if the worst-case scenario occurs, ageing populations and improved technology are likely to support continued robust growth going forward.

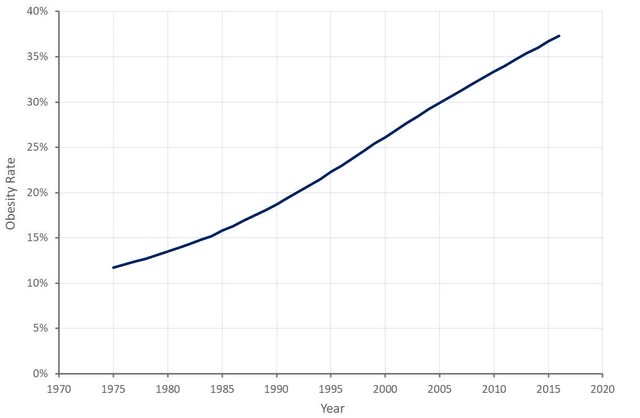

Obesity

Obesity is an important contributor to the demand for joint surgery as it increases the load placed on joints. As a result, rising obesity rates have been a tailwind for companies like Zimmer Biomet. The efficacy and sudden surge in popularity of weight loss drugs like GLP-1 agonists are now creating uncertainty about whether obesity rates, and in turn joint surgery demand, will drop. This seems unjustified when considering the facts though.

A BMI in excess of 40 increases the risk of post-op complications and as a result, many institutions will not perform surgeries on obese people. Close to 10% of the US population has a BMI over 40, meaning there is a large population who would benefit from surgery but are unable to receive it. As a result, weight loss drugs could actually increase the addressable population for joint surgery in the near term.

Longer-term, weight loss drugs could reduce joint surgery demand, as obesity is associated with joint damage. For example, overweight men have nearly 4x the risk of developing knee osteoarthritis. It should be noted that there is no cure for osteoarthritis though, meaning that once damage has been done, the condition will likely worsen over time, even with weight loss. This means that any impact on joint surgeries is unlikely to be felt for decades when the population of people who have avoided a lifetime of obesity through the continued use of weight loss drugs reaches their 60s. In any case, only an estimated 660,000 people in the US currently take FDA-approved weight loss medications, making any potential impact relatively modest at the moment.

Figure 1: Obesity Rate in the US (source: Created by author using data from Our World in Data)

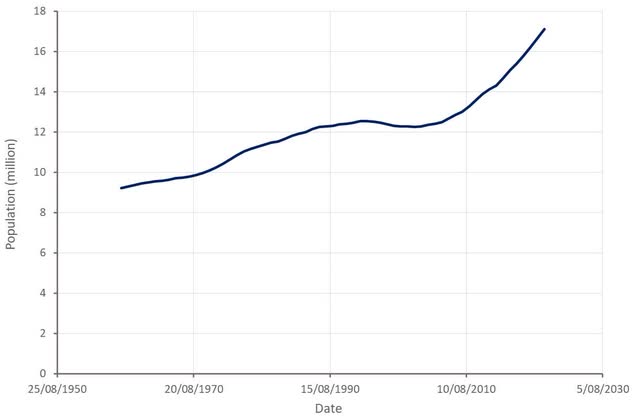

Demographics

Age is also a key driver of osteoarthritis and the need for joint replacements, and likely a far more important driver of demand for Zimmer Biomet than obesity. Osteoarthritis is a disease which impacts 528 million people globally. This figure will likely rise dramatically in the coming decades as the large baby boomer generation continues to age.

Figure 2: US Population Aged Over 65 (source: Created by author using data from The Federal Reserve)

In addition to an ageing population, technological advancements are lowering the age at which people begin to receive knee and hip replacements. This is because technologies like robotics and additive manufacturing create better outcomes and result in faster recoveries.

Robotics

Surgical robots use advanced 3D imaging, intraoperative data, and robotic assistance to help surgeons plan and execute joint replacement operations. They can reduce pain and hasten recovery times by minimizing trauma caused during surgery. Surgical robots also improve precision, creating better clinical outcomes.

In some cases, adoption of robotics has been restricted by high upfront costs and the learning curve associated with the technology. Costs are declining though, and Zimmer Biomet believes that surgeons reach time parity after a few cases. As a result, adoption of orthopedic surgical robotics is increasing, although the penetration rate in knee replacement surgery in the US is currently still only around 10%. The large joint replacement market is led by Stryker (SYK), as MAKO was the first mover in the space.

Additive Manufacturing

Additive manufacturing is widely used in a number of areas related to surgery, including:

- Planning

- Navigation

- Implant manufacturing

Additive manufacturing initially found adoption in dentistry and maxillofacial surgery, but its use has spread as the technology has improved.

Additive manufacturing enables customization and the production of complex parts. It can also enable the use of materials with desirable properties, like titanium. Titanium is widely used in medicine due to its biocompatibility and durability, but it is difficult to produce titanium parts using traditional subtractive manufacturing techniques. Additive manufacturing can also be used to create porous structures that mimic the mechanical and biological behavior of bone.

Zimmer Biomet

Zimmer Biomet is a medical device company targeting orthopedic implants and related products. This includes implants for joint replacement surgeries, including hips and knees, products for trauma and craniomaxillofacial surgeries, and surgical robots.

Zimmer Biomet’s sports medicine products are primarily for the repair of soft tissue injuries, including knees and shoulders. The company’s biologics products aid joint preservation and are used to support surgical procedures. Zimmer Biomet also offers products to stabilize bones in the chest after open heart surgery. Zimmer Biomet previously offered Dental and Spine products, but these were spun off into a separate business in March 2022.

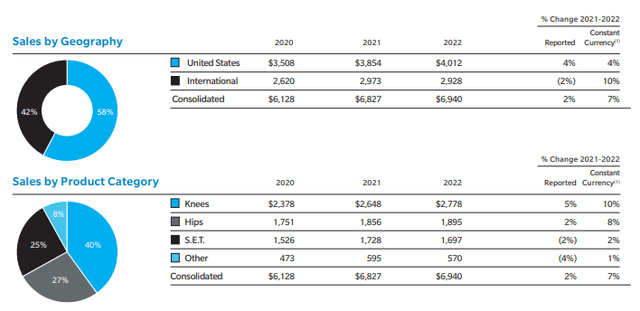

Figure 3: Zimmer Biomet Revenue by Geography and Segment (source: Zimmer Biomet)

ROSA is an integral part of Zimmer Biomet’s business given the rapid adoption of robotics in orthopedics. ROSA is currently offered for knees and hips, and Zimmer Biomet expects to expand ROSA to shoulders. ROSA continues to demonstrate clinical efficacy and time neutrality after a few cases. Zimmer Biomet is pleased with the adoption rate of ROSA, particularly within the ASC setting where speed is crucial. This is important as 10-15% of Zimmer’s sales comes from the ASC space and 40-50% of cases are expected to shift to ASCs in the next 5 years.

Zimmer Biomet has a focus on internal product development and plans to launch 40 new products over the next 36 months. As a result, the dollar value of the company’s pipeline is twice what it was in 2018. In addition, 80% of the products in Zimmer Biomet’s pipeline target markets with growth of at least 4% annually.

Management has also suggested that M&A will remain an important part of the company’s strategy going forward. Lower extremities (foot and ankle) are an area that has specifically been highlighted as a potential focus area for M&A.

Zimmer Biomet acquired Incisive and Relign in 2020 for 80 million USD upfront and up to 98 million USD in deferred and milestone payments. Incisive provides operating room solutions that target the 1.2 billion USD integrated operating room market, with a particular focus on ASCs. Incisive’s products offer data analytic capabilities and aim to improve efficiency in the surgical setting. Relign offers products targeting the 1.6 billion USD arthroscopy market. The Relign acquisition aims to bridge gaps in Zimmer Biomet’s sports medicine portfolio.

Zimmer Biomet also acquired A&E in 2020 for a total of 250 million USD, specifically for its sternal closure products. Zimmer believes the sternal closure business is growing in the high single digits.

Zimmer acquired Embody in early 2023 for 155 million USD at closing with up to 120 million USD additional consideration. At the time the acquisition was expected to be accretive to overall revenue growth. Embody offers collagen-based biointegrative solutions that support healing after soft tissue injuries. This acquisition supports Zimmer’s sports medicine business.

Zimmer Biomet faces a number of well-resourced competitors, including:

- DePuy Synthes

- Stryker

- Smith & Nephew

While Stryker has a more diversified business than Zimmer, it has a strong position in Zimmer’s core markets and is a formidable competitor.

Financial Analysis

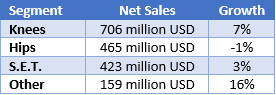

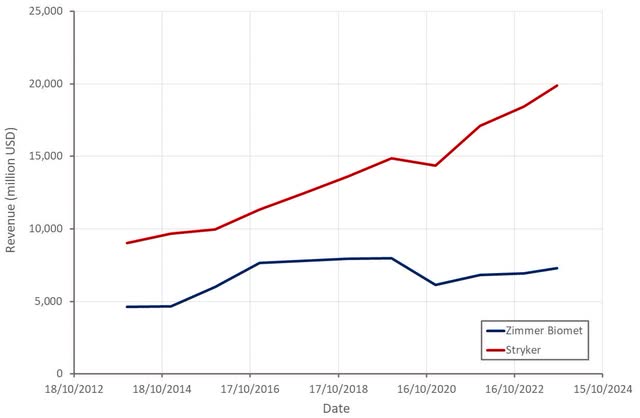

Zimmer Biomet’s revenue was 1.75 billion USD in the third quarter of 2023, up 5% YoY. This was driven by US growth of 6%, with international growth slightly lower at 3%, which was attributed to weakness in Europe and Asia on the back of tough comps and geopolitical tensions. Growth in the US is also currently being supported by a rapid rise in ASC surgeries, while volumes through traditional channels remain resilient. Zimmer Biomet’s ASC growth rate in the US is in the double digits.

Knee growth is being driven by both Zimmer’s cementless offering and the ROSA robotic platform. The Hips segment was down due to a combination of tough comps and geopolitical headwinds. The Other segment was driven by ROSA sales.

Table 1: Zimmer Biomet Q3 2023 Revenue by Segment (source: Created by author using data from Zimmer Biomet)

Zimmer Biomet is targeting revenue growth of 1-2% in excess of the market growth rate, which implies around mid-single digit growth. This should be supported by a moderation of pricing headwinds, product expansion, and M&A.

Figure 4: Zimmer Biomet Revenue Growth (source: Created by author using data from company reports)

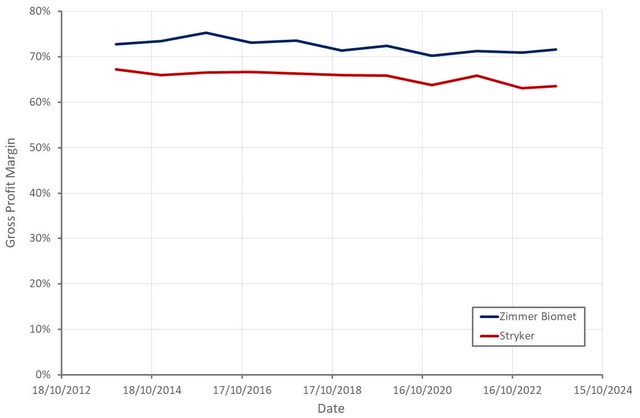

Zimmer Biomet’s gross profit margins have rebounded slightly in recent quarters on the back of easing supply chain headwinds and a more favorable pricing environment. Zimmer’s gross profit margins are high and relatively stable though, meaning bottom-line improvements are more likely to be driven by operating expense control.

Figure 5: Zimmer Biomet Gross Profit Margin (source: Created by author using data from company reports)

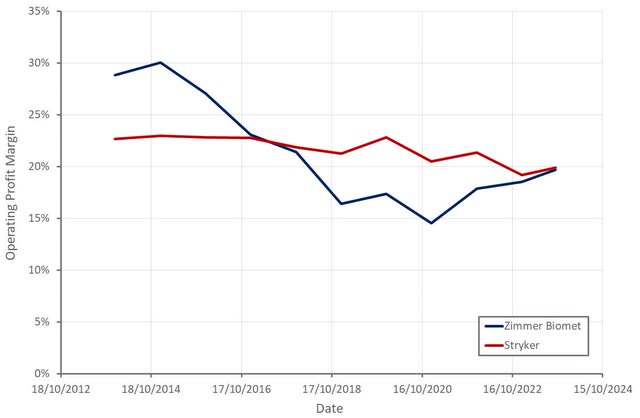

Zimmer Biomet’s profitability deteriorated significantly between 2014 and 2020. Much of this was related to goodwill impairment charges in the wake of the merger between Zimmer and Biomet. During this period Zimmer also faced issues related to supply and quality.

Margins have recovered somewhat over the past few years, and management expects to drive margins higher through a combination of operating leverage and efficiency.

Figure 6: Zimmer Biomet Operating Profit Margin (source: Created by author using data from Zimmer Biomet)

Conclusion

While there has been consternation about the demand for Zimmer Biomet’s products recently, the long-term market outlook remains favorable. Demographics and a large population of overweight people who already have damaged joints but are too young to receive replacements will continue to drive demand. In addition, the rise of robotics in joint surgery is a tailwind and Zimmer Biomet’s expansion of ROSA to hips and shoulders should see solid growth going forward.

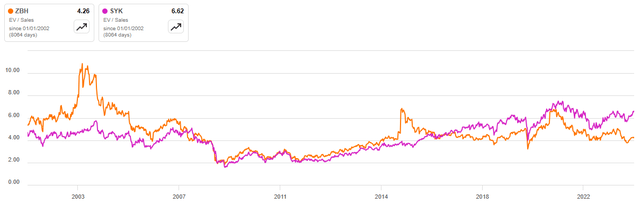

It is questionable whether Zimmer Biomet is the right way to gain exposure to these tailwinds though. While the expansion of ROSA to hips and shoulders should support growth, Stryker is the clear leader in the space and the valuation gap between the two companies appears insufficient given the quality difference.

Stryker invests more in R&D, both in absolute terms and as a percentage of revenue, which may help to explain the company’s ability to continue gaining market share. MAKO was also a first mover in orthopedic surgery robotics and has built up a strong competitive position. Stryker initially focused on building a large installed base and is now trying to drive utilization, in part through direct-to-consumer advertising. To the extent that AI becomes an important part of visualization and navigation during surgery, this could also help to create a sustainable data advantage. Stryker is also ahead in extending MAKO to new areas like shoulders and spines. Stryker also appears to be more vertically integrated in some areas, like additive manufacturing, having invested several hundred million euros into 3D printing R&D and manufacturing capabilities.

Figure 7: Zimmer Biomet EV/S Multiple (source: Seeking Alpha)

Read the full article here

")

")

")