")

")

")

Quick Overview

With banks making headlines this week again, I wanted to touch upon a subsector of the financials segment that is often under-covered but often presents an interesting investing opportunity as I’ve written about in the last year, and that is insurance. Though it may not be the mainstream media’s hip and cool startup from Silicon Valley, what it lacks in media hype it makes up in fundamentals, which we think is more important.

In fact, you may remember the opening scene of the 1980s movie Wall Street, where the experienced broker tells the younger folks to “stick to the fundamentals.. that’s how IBM and Hilton were built. Good things sometimes take time.”

Today’s insurance pick of the week trading now for under $70 is MetLife (NYSE:MET), a stock I covered in August and since calling it a hold its share price has gone up nearly 5% since then.

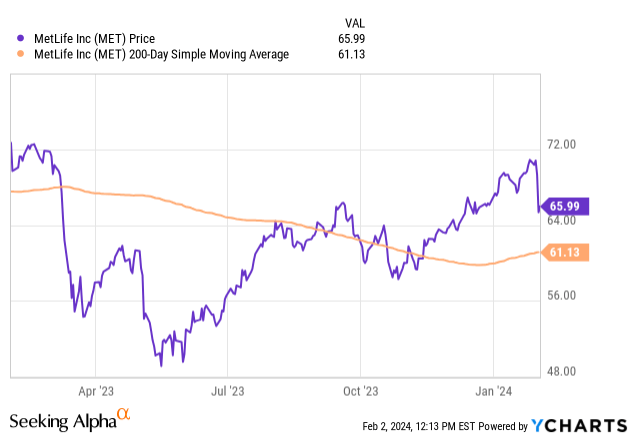

MetLife – price since last rating (Seeking Alpha)

This time around, our thesis on this stock is to reaffirm its hold rating, and this is driven by solid YoY growth in revenue, earnings, and equity, but also analyst estimates of future EPS growth, and an interest rate environment favoring this firm’s asset portfolio.

At the same time, its dividend yield compared to key peers is unremarkable, and despite decent valuations it also is trading at a significant premium to its moving average and has exposure to office loans, a known risk being talked about a lot lately.

Methodology

This article will make use of our Investing Flow below which is based on waterfall methodology from the world of project management.

Today’s article aims to answer questions like why this specific stock and sector, what are the risks and benefits we can plan for, whether the current share price and valuation makes sense, what metrics matter to this specific sector, and what could be a long-term exit strategy for this stock?

The answers to these questions, holistically, should lead to a business decision of whether we buy, sell, or hold this stock today.

MetLife – investing flow (author)

Initiating: Why this Stock & Sector?

First, let’s start with the overall sector of financials. We know from key market data on Seeking Alpha that this segment has grown nicely from 3 years ago, to the tune of +32% growth in 3 years, but also +6% growth in the last year.

It must be said that it is a large sector that encompasses banks, asset managers, and insurance. What I like about insurance is that it does not have certain issues that banks have. For example, it takes in a ton of cash from customer policy premiums, and after paying out expenses and policy claims it invests a lot of the extra cash into an asset portfolio, making money on that too, largely from interest. Hence, a high rate environment is like a gold rush for this firm.

At the same time, unlike banks, it does not have the liability of customer deposits, fear of bank runs, or paying interest on traditional bank depositor funds. Insurance policies, in our opinion, also tend to be “sticky” especially life insurance.

With that said, we like to analyze MetLife because it is a leading life insurer, but also has diversification among other lines of business. Some of its peers and competitors would be Prudential Financial (PRU), and Canada’s Sun Life Financial (SLF).

From its profile on SA, we know that it has been around for +100 years, trades on the NYSE, has a global reach, and besides insurance it also deals in fixed and variable annuities, pension products, and capital markets investment products.

Those of us who grew up in the New York City area also know how strong of a brand MetLife is, and not just from having its name on a huge building in Manhattan but also from multiple generations having watched MetLife ads on TV, print, and later online. It is a brand built over generations, and like we said sometimes good things take time.

Planning: What are Risks & Benefits?

Now that we know why we are interested in this sector and this stock, let’s talk about planning for the risks and benefits of owning this stock.

First, let’s touch on its most recent earnings results that are still fresh after their Jan. 31st release.

This appears to us a serious company, with YoY revenue growing to +$19B in the quarter ending December, vs $16.3B in December 2022.

We can see from the income statement what drove this revenue was growth in both its core business of insurance premiums but also growth in interest-income on its asset portfolio.

However, we also see from that same statement that there was YoY growth in policy benefit payouts, with +$14.7B paid out in benefits in Q4, and this clearly impacting earnings with net income falling to $607MM vs $1.3B in Dec. 2022.

The company was able to maintain positive cash flow, and from the balance sheet we see a significant YoY decline in long-term corporate debt, which helped towards YoY equity growth with total equity now at +$30.25B.

Another positive to note is that analysts are estimating further EPS growth for the next few years at MetLife, with nearly +23% YoY growth in EPS expected for the quarter ending Dec. 2024.

In terms of liquidity risk, the company in its full-year 2023 results indicated “holding company cash and liquid assets of $5.2B at December 31, 2023, which is above the target cash buffer of $3.0 – $4.0B.”

We also know that the high interest rate environment has benefitted this firm. According to their Q4 commentary, growth in net investment income was “driven by higher interest rates and increases in the estimated fair value of certain securities.”

With recent headlines in the financial press talking about risk exposure of banks to office loans, such as The Financial Times reporting on shares plunging at New York Community Bancorp (NYCB) after the bank reported loan losses ” which emanated from loans tied to office buildings,” we care about what kind of exposure MetLife has to office real estate and how it can affect this firm going forward.

From MetLife’s financial supplement, we see that their $19.65B of office loan exposure is nearly +38% of their total commercial mortgage loans which make about $52.1B of the net mortgage loan book of $84.1B. So, offices are around 23% of the net mortgage loans MetLife is exposed to.

MetLife – exposure to office (company financial supplement)

Our outlook, therefore, is one of positive caution on this firm because on the one hand it has grown revenue, equity and earnings as well as having future EPS growth estimates however at the same time almost 1/4th of its mortgage loan exposure is tied to offices. Even if those are top quality loans, our concern is the market becoming increasingly jittery about owning companies with more than a few percentage points of exposure to offices, especially if more banks start reporting significant loan losses.

Holistically, the risk/benefit scenario for us here so far is one of a hold rather than a buy or sell, but we will need some more data before making a decision.

Executing: Is the Price & Valuation Justified?

A factor we consider is share price in relation to its 200-day moving average, as well as valuations on this stock.

First, let’s pull the yChart:

We see from the chart that the stock has recovered quite nicely from its lows last spring when many financials were taking a dip in the wake of regional bank failures, and right now MetLife is trading at nearly +8% vs its 200-day SMA.

From valuation metrics we know that the forward P/E is 7.98, while the sector average is 10.88. Further, it is a better valuation than the 16.6x earnings multiple at insurance peer Prudential Financial.

Compared to my summer coverage of MetLife when it had a forward P/E of 13.7, now it presents a better valuation at nearly 8x forward earnings, considering that analysts are estimating +23% YoY EPS growth by December, as I mentioned earlier. So, it appears the market is holding back a bit even though analysts are bullish. We see this as a value opportunity.

Personally, we think the continued high interest rate environment will continue to benefit this firm’s earnings, especially after the late-January Fed meeting did not result in a rate cut and according to a CNBC article it seems less likely that a March rate cut will happen either.

As far as forward P/B ratio, it is now 1.62, just above the sector average of 1.04. This tells us the market is bullish on future equity growth, likely due to expected earnings growth and the YoY equity growth and lower debt the company reported in Q4 results. We like this valuation as it is backed by proven equity growth and high likelihood of future equity growth, so it justifies bullishness on the share price.

At this point in our “waterfall” approach to this stock, it could still be either a hold or a buy, and we see today’s consensus (SA analysts, Wall Street, quant system) all are calling for a buy.

The deciding factor will be dividend yield and dividend growth, and we will cover that in the next section.

Monitor & Control: What Metrics Matter to this Sector?

We are caught between whether to buy shares in MetLife at the current elevated price or hold on (assuming we had already bought at the earlier lower prices in spring).

Two metrics we monitor on an ongoing basis (as they are subject to change) are dividend yield and dividend growth, but also the stability of quarterly dividend payouts.

We know that MetLife up until now has been a dividend grower over 10 years, with the annual dividend going from $1.18 in 2014 to $2.06 in 2023, a +74% growth in a decade. This tells us it is a serious firm able to return capital back to shareholders. Consider that the recent loan loss from New York Community Bancorp led to that firm reducing its quarterly dividend, and affecting yield as well.

We think the continued expected profitability growth at MetLife, and positive cash flow situation, increases likelihood of dividend hikes in 2024. It is now already at $0.52/share, which we think is not bad for a stock trading at under $70, as it offers a +3% yield. Although history does not guarantee future payouts, it does increase our confidence as this firm has had uninterrupted quarterly payouts for years.

Finally, we want to compare the trailing yield vs peers, to grab the best yield for our capital invested.

The comparables we will use are Prudential, Sun Life, and Aflac (AFL). We can see that Prudential leads the way with 4.87% yield, so in an interest-rate environment where investors are often leaving stocks for high-rate CDs and money market funds paying +5% yield and higher, we have to say that MetLife comes short in its yield.

Prudential, despite its $125 share price today, offers a quarterly dividend of $1.25/share, and also has a history of steady payouts and 10 year dividend growth, so that would be our choice in terms of the best yield offer.

MetLife – dividend yield vs peers (Seeking Alpha)

So, we argue for a firm hold on MetLife rather than a buy or sell at this point, and believe the evidence supports this case.

Closing: When do I Exit This Investment?

Now that we determined to hold on to MetLife and not buy shares or sell them, what is our portfolio strategy and how do we exit from this position?

Our strategy is that MetLife would be an anchor stock in our portfolio, giving us exposure to large, well-established and highly liquid insurance companies like this one, so we would be looking to hold it for 30+ years as part of a dividend-income portfolio, rather than looking to achieve short-term capital gains.

By holding on, we know it exposes our portfolio to downside but also upside risk. The downside risk we think could come from jittery investors fleeing financials overall in the event of further office loan headaches in the system, but we also think there is upside potential as opportunistic investors will recognize the “future value” of this stock and will also hold on to it like we are, particularly dividend-oriented investors who want the steady dividend income from a secure company. The downside risk of office loan defaults ought to subside, we think, after interest rates come down again as it will make borrowing cheaper. Right now the high cost of borrowing to invest in offices is simply not a great investment, but eventually that should change since rates always come down again as we’ve watched this cycle over and over again.

In other words, we consider MetLife a “safety” stock to keep our hands on, and we also recognize the “value” of the insurance industry as a necessity as an industry that helps people and businesses transfer risk to a third -party.

In this case, MetLife is heavy into life insurance, and that is a life event that can become quite costly and financially impeding to any family, so we think MetLife provides a critical necessity economically to transfer that financial risk to an insurer, and as investors we also see the value of the continuous faucet of policy premiums coming into the company each year, and through efficient actuarial /risk management this firm has made a 100+ year business out of insuring what we could call someone’s most important asset.. their life and that of family members.

Read the full article here

")

")

")