")

")

")

")

Dear readers/followers,

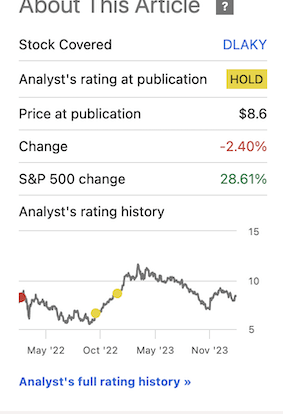

Since my last article, Lufthansa has done exactly what I expected it to – decline. The company has seen a negative 2.4% RoR while the market is up almost 29%, which makes it a 30% difference.

Seeking Alpha Lufthansa RoR (Seeking Alpha)

In this article, I mean to show you why despite the decline in the share price, I continue to have very little interest in this company – or most pure-play airlines. I do own shares in companies that own airplanes/airlines, such as Exchange Income Corp (OTCPK:EIFZF) or TUI (OTCPK:TUIFF), but I do not own any pure-play airline companies. There is a reason for this. I share Warren Buffett’s conviction that airlines do not make for very appealing investments, unless you know exactly what you’re getting into and what you expect from the company.

Even then, it’s my argument that a company in this field usually has lower-risk alternatives that offer a better and safer upside.

But, I have a rating on this company – and there is a price where I would say that one could invest in Deutsche Lufthansa.

So let’s see what we have here.

Deutsche Lufthansa – An update for 2024E

Lufthansa has absolutely been a problematic stock from some perspectives. The company has the dubious honor of being one of the very, very few companies I’ve ever assigned a “Sell” rating to, and one that paid off for quite some time. Going into the latest update, I do not change my rating here. I can understand why some analysts might see an upside for this company, but I do not share that positive view.

This company might seem like an interesting play – after all, we have control of some very attractive central-European airlines including geographies like Switzerland, Austria, BeNeLux, and others. It has the Star Alliance brand, and through it offers its travelers one of the most extensive networks of destinations on the planet. Even with Ukraine and the geopolitical and economic macro, none of the company’s overall geographical exposures are in themselves unattractive.

Only the sector of airlines itself and what to expect is unattractive, even with the addition of the logistics operator Eurowings. The Germany-heavy exposure also isn’t really the problem, as I see it. The problem is the likely future of this company in a forecast where earnings are not expected to improve.

The current company expectation is a flat EPS beyond 2023, which is perhaps growing 1-2%. We’ll see the impact of this in a normalized valuation going forward.

But I can say early on, that the core of the bearish thesis, of which I am a proponent at this valuation, would be mostly based on the lack of catalysts for an upward movement in this specific macro and company situation.

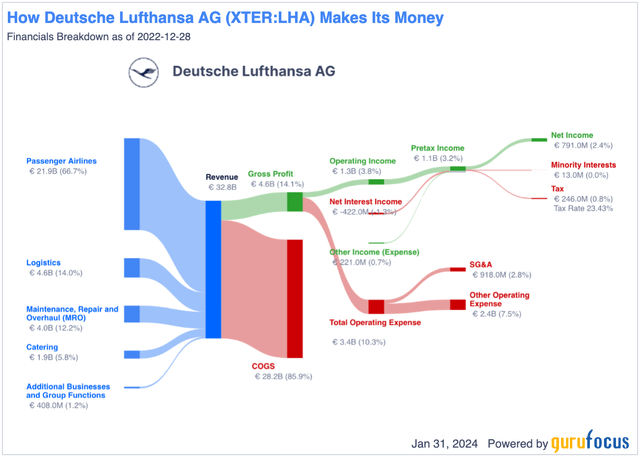

It’s wrong to say that this is an unprofitable company. Lufthansa does in fact generate profit – it’s just that I view the business model as entirely unattractive based purely on what happens with €100 of revenue that goes into this model.

Lufthansa Business Model (GuruFocus)

Any business model here that generates a sub-3% net income in a segment that is not consumer durable, or any sort of far more durable sector, is not something that I to begin with would express a whole lot of interest in. As I see it, cyclicality can only be accepted if during upcycled the company has massive amounts of profit and very good margins. Similarly, low net margins can only be accepted if it’s combined with very durable and stable earnings trends when you can count on those 1-5% net margins to be around for some time.

Otherwise, what’s the point? Combining the two unattractive traits of excessive cyclicality with low margins makes for a very tough sell for me. Because, where can a company like this “save” and drive efficiencies? It’s unlikely that COGS is something that the company can do much about – not with inflation across the board, wage increases, and other factors, and commodities and other things flying upward.

But I can’t just be negative. Lufthansa has some very good things going for it as well.

Foremost in this list, is the fact that the company is now BBB-rated or above by all leading agencies once again, as of 22nd of January.

That’s a non-trivial set of news and part of why I can understand some of the positivity. The company has also concluded sale/leaseback transactions and ordered 80 new aircraft. Unlike what I expected or hoped, the company has split the straight purchases 50/50 between Airbus (OTCPK:EADSY) and Boeing (BA). 40 each from A220-300s and 737-8-MAX. As for the latest set of disasters, I make very certain that whenever I fly either continental or trans-continental, I do not step aboard a Boeing plane. This may be overly careful, but I’m happy to be labeled “careful” some feel this necessary. From a business perspective, I do not view these as equally attractive assets to own, depending on the pricing and purchase term.

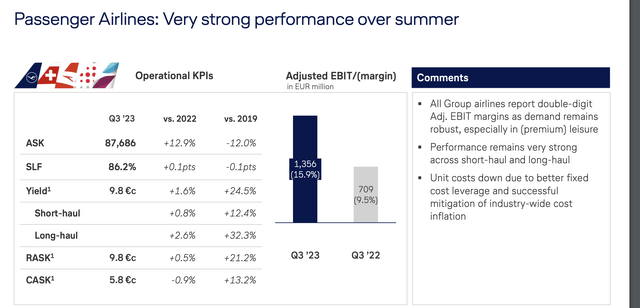

Also positive, 3Q23 which is the latest quarter, has brought results back to good levels and positive, confirming an overall annual trajectory to where a full-year adjusted EPS of over €1.5 is entirely possible, and something I forecast for the company here. (Source: Deutsche Lufthansa IR)

However, this does not make the company attractive in itself.

Lufthansa IR (Lufthansa IR)

Even the fundamental improvements such as reduction in net debt as well as pension liabilities only act as small positives for a picture I view as fairly negative or at least, flat for the near term. The company had good FCF, and this brought the next debt on an adjusted EBITDA down to below 1.5x, which also goes some way to explain the rating increases.

Lufthansa IR (Lufthansa IR)

I’m interested, as an analyst, to see how the company delivers on customer value – with many of the US-based carriers already having upgraded their interiors, to see how Lufthansa intends to deliver the value proposition for what is usually at least a somewhat more expensive ticket than the budget and the US-based carriers. I have to say though, what I see there does imply to me a decent value for the various price points.

Lufthansa IR (Lufthansa IR)

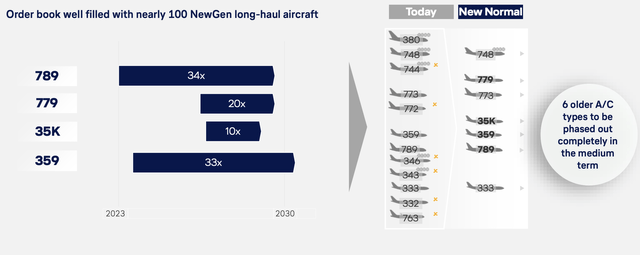

The company has a well-filled order book with over 100 aircraft incoming, towards a “new normal” with a new fleet of very attractive assets.

Lufthansa IR (Lufthansa IR)

The company has already achieved its emission reduction targets and the latest results mean that this is the first European airline, and second airline worldwide to receive validation by SBTi.

The future for Lufthansa is to use the multi-hub and multi-brand strategy, including Lufthansa, Swiss, Austrian, and Brussels, to drive growth through scale and efficiency, with joint operations, network, and sourcing.

I will say this – if I believe any company can become a good investment in this sector, I believe that is Lufthansa.

Will it?

I believe that’s too early to say.

The 2023E results are to me not an argument to invest in the business. This recovers what I believe to be good “baseline” earnings, but I do not see this automatically going upward.

Let me show you why.

Deutsche Lufthansa Valuation – not much upside, I retain “HOLD”.

What the upside is here is difficult to see. I choose to forecast Deutsche Lufthansa at a 7-10 P/E average, to avoid the GFC, but to include COVID-19, which puts the company at 4-6x P/E – justified given the volatility and mostly negative returns over time.

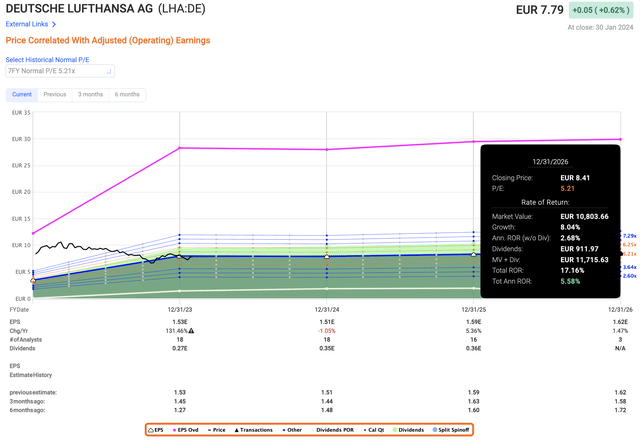

If we forecast the company at the average or midpoint of around 5x, the company does not manage an upside of more than 5.6% per year – and that includes the company’s dividend.

Deutsche Lufthansa Upside (F.A.S.T graphs)

Airlines are a very tricky sort of investment, and in my experience, people take what they invest in far too lightly. They don’t give risk considerations the same attention they should, and they also don’t ask the fundamental question if a company is really that much more attractive than a far safer alternative. I know that because I work with this professionally, and I used to be similar when I started investing.

I have invested more in such turnarounds over the past few years, successfully. Rolls-Royce (OTCPK:RYCEF) was a very good example of such an investment, and I am prepared as of this article to give a price target for Lufthansa. But it might be a target that very few agree with.

S&P Global goes from €6.6 to €15, with a current share price of €7.7 native. I would say a fair price target that I would buy the company at is €5.5 – to find a good conservative upside for this company – no higher than that.

Currently, 5 of 17 analysts are at a “BUY” here – so you can see, that there are not many that are convinced this company has a clear enough upside here. The analysts are expecting the company to actually consider a dividend for this year – one that would result in a yield of 3.5%, and would increase the return profile of the investment considerably.

However, until this is declared, I point clearly to the fact that Lufthansa misses analyst estimates 50% of the time with either a 10% or 20% margin of error, and those misses are on the negative side, with differences of upwards of 100%.

So to state that you believe with high conviction that Lufthansa can achieve this or that, you’re in a minority, and statistics and historical trends are not on your side, given how much money shareholders have lost over time by investing in this business at the “wrong” price.

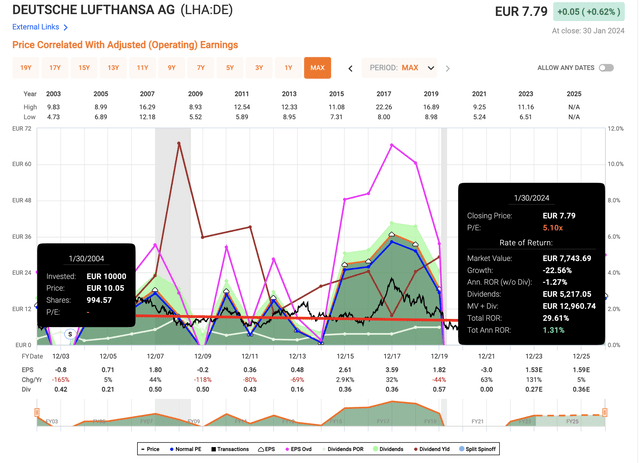

All this is a way of saying for me to “be careful” with a company that has this sort of EPS and RoR profile on a 20-year basis.

Lufthansa RoR (F.A.S.T graphs)

Because if you want 1% returns annualized, you can put your money in any savings account that pays interest and does better at lower risk.

My thesis for the company is as follows, and I would consider buying Lufthansa, at the highest, for €5.5/share to expect a solid double-digit upside. But even then I would be careful.

Thesis

My thesis on Lufthansa is as follows:

- This incumbent airline has been on a rollercoaster ride since early 2002. 20-year returns for Lufthansa are negative without the dividend, making it a terrible investment.

- There is real potential for a turnaround somewhere between 2024-2025, but this does not yet warrant a change in my Lufthansa thesis, because normalized multiples do not necessarily imply any sort of upside here.

- Because of this, I am continuing my coverage on SA on Lufthansa with a “Hold” rating. I still believe that Lufthansa should not be part of any conservative portfolio, even at the risk of some sort of upside here.

- I say a €5.5 PT is what I want before I would invest.

Remember, I’m all about :

- Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company still fulfills none of my investment criteria, dictating the “Hold”.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")