")

")

")

")

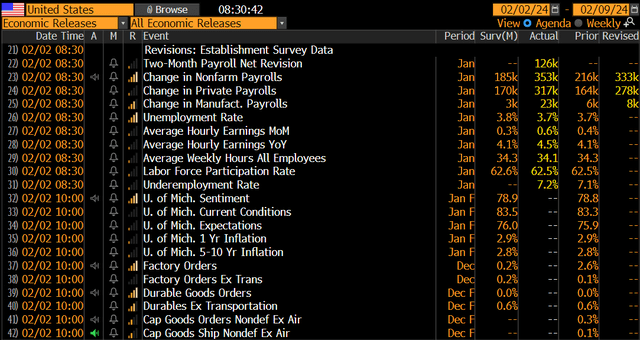

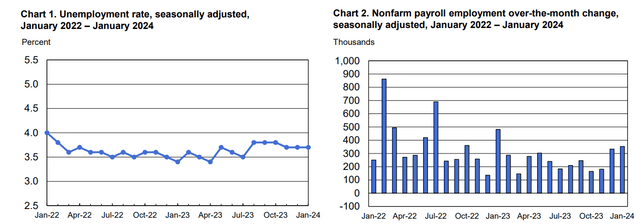

The January jobs report revealed a massive 353,000 nonfarm payrolls gain. Expectations were for just a 185,000 add. It was the biggest monthly employment advance since January 2023 while the unemployment rate remained at 3.7%, just 0.3ppt off the multi-decade low.

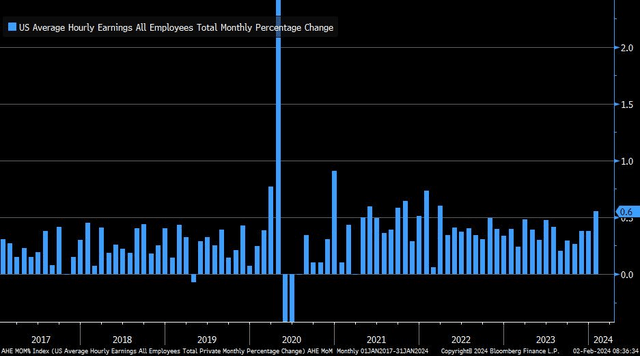

Average hourly earnings soared +0.6%, the biggest rise since January 2022. The year-on-year wage increase was also huge, up 4.5% compared to the +4.1% consensus. The pre-COVID high, for perspective, was just +3.6%. The average workweek was only 34.1 hours, a significant drop from 34.3 hours, so that was a dovish number. The Labor Force Participation Rate was 62.5%, unchanged from December, and the U6 under-employment rate was 7.2%, up 0.1ppt from December.

Big Jobs Gain to Start 2024

Christian Fromhertz

Unemployment Rate Steady, Monthly Jobs Climb Strong

BLS

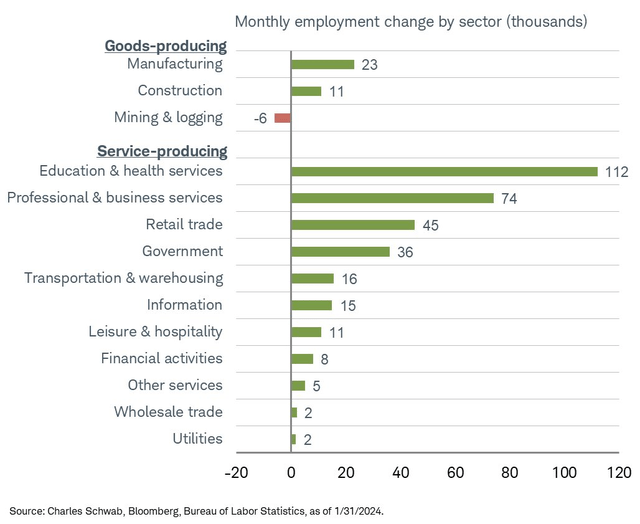

It’s hard to suss out what was the true employment gain and what changes were due to seasonal revisions. It is also key to point out that the previous two monthly NFP gains were revised significantly higher to the tune of +126,000, supporting the strong-labor market thesis. Private Payrolls were also very strong. Key to the cyclical side of the economy, Manufacturing jobs jumped by 23,000, significantly above the +3,000 consensus and a revised +8,000 in the prior month.

Employment Change by Sector

LizAnn Sonders

Average Hourly Earnings MoM

LizAnn Sonders

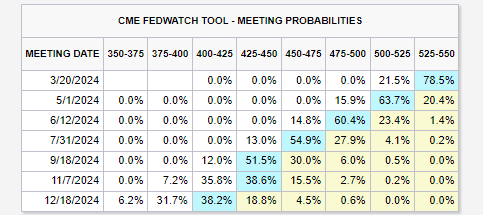

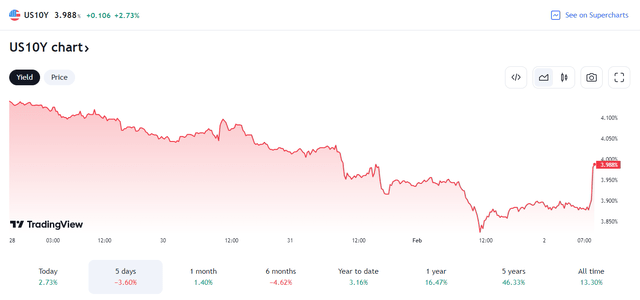

Since this was more than 100,000 over even the top-end of forecasters’ range, this was clearly a hot number. The U.S. 10-year Treasury note yield (US10Y) popped about 14 basis points, and the chance of a March Fed rate cut was slashed significantly.

Fed Funds Futures: Small Chance of A March Ease

CME FedWatch Tool

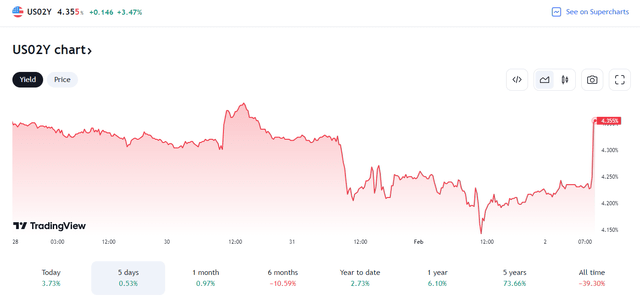

Equity futures tumbled following the hawkish January jobs report, but the S&P 500 (SP500) managed to hold some of its pre-market gains, powered higher by Meta Platforms (META) and Amazon (AMZN) following those firm’s strong earnings reports. Apple (AAPL) shares traded lower Friday morning post-earnings. The yield on the short-term 2-year Treasury note, a gauge on where future Fed policy may be, rose from 4.22% to 4.40%. The US Dollar Index (DXY) popped above the 103.50 mark but remains confined to its recent trading range.

US 2-Year Yield Soars

TradingView

US 10-Year Yield Jumps to 4%

TradingView

Regional Banking Fears Brew

What will be key to watch over the coming sessions is how the U.S. regional banks perform. The group was in turmoil just 10 months ago on fears of severe asset-liability mismatches and steep losses on the banks’ held-to-maturity portfolios. Those fears could be resurfacing following volatility in shares of New York Community Bancorp (NYCB), though many pundits are quick to point out that there are idiosyncratic risks to NYCB. The iShares Russell 2000 ETF (IWM) dropped to a 0.4% loss in the premarket as yield-sensitive regional banks continue to be a concern. The SPDR S&P Regional Banking ETF (KRE) was down nearly 2% before the bell on Friday.

Opposing Data

Bigger picture, today’s January jobs report flies in the face of some recent troubling employment data. Recall that the ADP Private Payrolls number was somewhat soft and there was a recent tick-up in Jobless Claims. What’s more, the ISM Manufacturing Employment subindex dipped last month, and had already been in contraction territory. Anecdotally, it’s hard to bypass the mounting list of corporate layoff announcements to start 2024. Despite those poor headlines, the Bureau of Labor Statistics’ establishment survey was stout. The Household survey, used to determine the unemployment rate, revealed a 31,000-employment decline. Those two surveys often oppose each other, though.

Strong Growth Persists

With a gangbuster January NFP report, U.S. economic growth continues to hum along. Recall that Q4’s US real GDP growth rate was a solid 3.3%, on the heels of a +4.9% print in Q3 2023. Early looks at first-quarter economic expansion are near 4%, at least according to the Atlanta Fed’s GDPnow tool, though the consensus forecaster’s growth estimate is significantly under that lofty rate. All eyes will now be on both the January CPI report and Retail Sales data to be released later this month.

Earnings Rolling In

We are also still in the throes of Q4 earnings season, which has turned better following healthy per-share profits reported by many mega cap tech companies this week and last. Smaller companies and foreign firms will grab the reporting torch next week. I will be eyeing the weekly FactSet earning season update due out later this afternoon.

The Bottom Line

It was a January jobs jolt. The blowout NFP report featured a monthly employment gain that was close to double what economists were expecting. Average hourly earnings were exceptionally hot, though the total hours worked number was light. With positive revisions to previous months, the chances of a March Fed rate cut were cut considerably. Stocks stumbled from their pre-market highs.

Read the full article here

")

")

")

")

")