")

")

")

Celestica Posts Strong Earnings

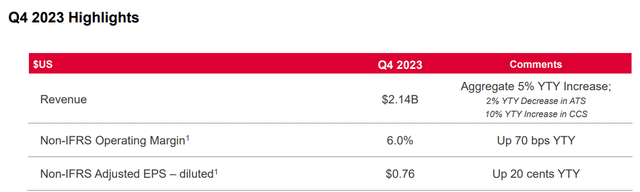

Celestica (NYSE:CLS) reported its fourth quarter 2023 financial results on January 29, 2024. The company delivered another solid performance, beating the consensus estimates on both revenue and earnings. Celestica’s revenue increased 5% year-over-year to $2.14 billion, while its adjusted EPS rose 36% to $0.76. The company also achieved a record operating margin of 6.0%, up from 5.3% in the same quarter last year. Celestica’s strong execution and growth momentum is impressive, especially in the face of the ongoing macroeconomic uncertainties.

Q4 2023 Earnings (Celestica)

For a detailed analysis of the Celestica business, please see our previous article here. In this article we will review the Q4 earnings results and update our valuation with the Q4 numbers and FY 2024 outlook.

CCS Segment Continues to Deliver

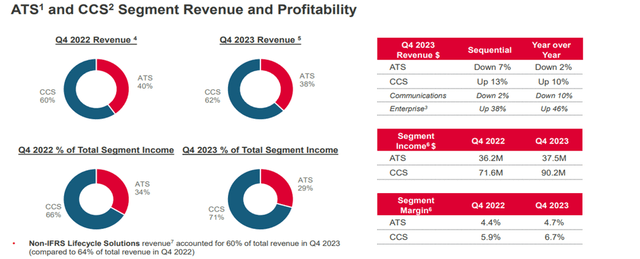

Celestica operates in two segments: Advanced Technology Solutions (ATS) and Connectivity & Cloud Solutions (CCS). Both segments offer attractive growth potential, but CCS is the main driver of Celestica’s revenue growth and margin improvement. The CCS segment delivered another strong performance in Q4 2023, growing 10% year-over-year to $1.34 billion, accounting for 62% of the total revenue. The segment benefited from the strong hyperscaler demand for its custom hardware solutions. The ATS segment, which comprises Aerospace & Defense, Industrial, HealthTech and Capital Equipment businesses, declined 2% year-over-year due to the softness in the industrial business.

Q4 2023 Earnings (Celestica)

Margin Expansion Continues

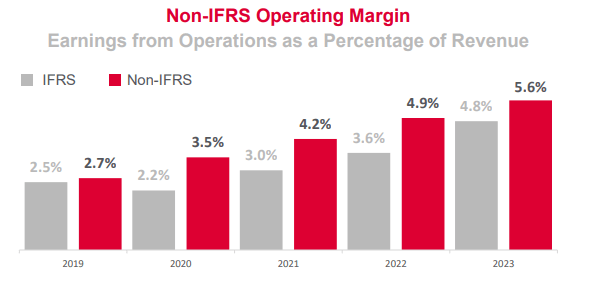

Another positive aspect of Celestica’s Q4 2023 results was the continued margin expansion, driven by the company’s operational efficiency, and portfolio mix improvement. Celestica achieved a record non- operating margin of 6.0%, up from 5.3% in Q4 2022. Th operating margin expansion was driven by the CCS segment which increased from 5.9% to 6.7%, due to improved product mix and higher volumes by hyperscaler customers.

The company also improved its gross margin to 10.4%, up from 9.1% in Q4 2022. Celestica has been executing on its multi-year margin improvement plan, which includes reducing its fixed costs, increasing its automation, and shifting its portfolio mix towards higher-margin and higher-growth segments. We believe Celestica has more room to improve its margins, as the company is expanding its margins at a 16% CAGR (see below).

Q4 2023 Earnings Margins (Celestica)

FY 2024 Outlook is Promising

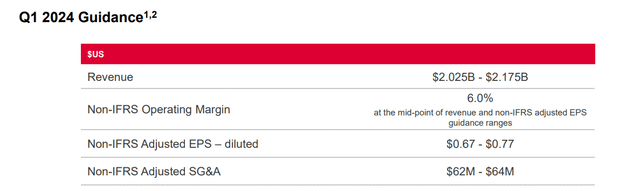

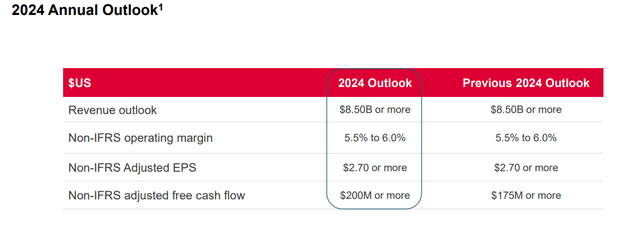

Celestica provided a promising outlook for Q1 2024, reflecting its confidence in its growth prospects and margin improvement potential. The company expects its revenue to range from $2.025 billion to $2.175 billion, which is 14% growth at the midpoint, again fueled by the persistent strength of the CCS segment. The company also projects its adjusted EPS to increase by 53%, driven by robust revenue growth and margin improvement. We believe Celestica’s forecast is very achievable and has considerable upside potential.

Q1 2024 Outlook (Celestica)

Updated Valuation

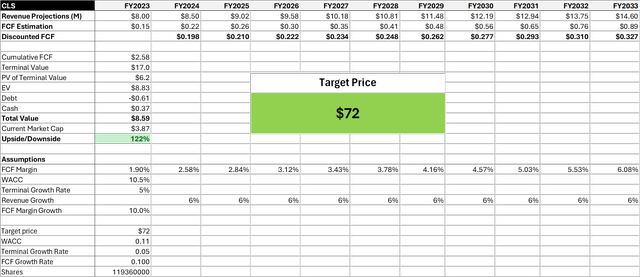

Based on Celestica’s Q4 2023 results and FY 2024 outlook, we have updated our DCF valuation for the company. The company now expects 2024 free cash flow to be $200 million (was $175 million) so we will update that one in our model. Also, we adjust the revenue growth rate to 6% as per the company’s 2024 guidance and keep it flat at 6% for 10 years. For the rest we keep the same numbers. Our model assumes 10% annual FCF increase, consistent with the company’s FCF growth guidance. We use a WACC of 10.5% and a terminal growth rate of 5.0%. We apply a 5% terminal growth rate after the 10-year period.

FY 2024 Outlook (Celestica)

Based on our DCF model, we derive a fair value of $72 per share for Celestica, implying significant upside from the current price levels. We maintain our buy rating and raise our price target from $63 to $72.

Celestica DCF Model (Author)

Risks

We see the following risks for Celestica’s valuation:

Macro Uncertainties: Celestica is a global company and is exposed to macroeconomic uncertainties, geopolitical conflicts and trade disputes that may affect its customer demand and operational efficiency.

Competition: The company faces strong competition in a cyclical industry. It has to compete with leading ECMs, ODMs and in some cases OEMs which that may impact its market share.

Conclusion

Celestica has delivered a strong performance in Q4 2023, beating the market expectations on both revenue and earnings. The company has demonstrated its ability to execute on its growth strategy and margin improvement plan, despite the challenging macroeconomic environment. The company’s CCS segment is the main growth engine, benefiting from the high demand from hyperscaler customers.

The company has also provided a promising outlook for Q1 2024 and FY 2024, reflecting its confidence in its future growth potential and profitability. Based on our updated DCF valuation, we believe Celestica is undervalued at the current price levels. We assign a fair value of $72 per share, implying more than 100% upside.

We reiterate our buy recommendation for Celestica, as we believe it is the best investment opportunity in the EMS industry.

Read the full article here

")

")

")