")

")

Introduction

The stock of the world’s largest IT infra services provider- Kyndryl Holdings, Inc. (NYSE:KD), has been on a tear over the last six months. At a time when the tech-heavy Nasdaq has only facilitated +9% returns, KD has delivered over 5x that figure.

YCharts

The two main catalysts behind KD’s exemplary alpha have been its quarterly results (KD follows a March-year end fiscal, so Q1 and Q2 are already done, and we now await Q3 results).

Back in August when the Q1 results came out, the stock witnessed a +14% spike the following day; in November when the Q2 results came out, the impact was less pronounced but still quite notable at +6% the following day.

Now investors have the opportunity to potentially profit (or loss) from another major event – the Q3 results, which will come out on February 6 after the market close (the earnings call related to this will take place the following day at 8:30 AM ET).

If you’re contemplating a position in KD ahead of the key event, here are a few important considerations.

Earnings-Related Considerations

As far as the headlines are concerned, KD has a pretty decent track record. Over the last eight quarters, it has missed bottom line estimates only 25% of the time, and on the top line, they’ve always delivered a beat.

For the upcoming Q3, the two key headline numbers to watch are a GAAP EPS of -$0.26, and a revenue figure of $3.92bn. Prima facie, that revenue figure may put off a few passive observers of KD, as it would represent both a sequential decline of -4%, and a YoY decline of -9%, but do note that this is a corollary of management’s broad strategy to get rid of or reduce exposure to low-margin revenue accounts. Please be aware that YoY revenue declines are expected to persist all the way until FY 2026 (March 2026), although KD management believes that they could start delivering positive YoY topline growth by the calendar year 2025.

In constant currency terms, one should also prepare for further worsening on the topline front, not just in Q3 but through this fiscal year. In Q1, the constant currency (CC) revenue decline was only -1%, but this worsened to -5% in Q2, and one shouldn’t be surprised to see double-digit CC declines, as the FY24 forecast is for a -9% decline; so clearly, Q3 and Q4 are expected to be a lot worse than the -3% run rate seen in H1.

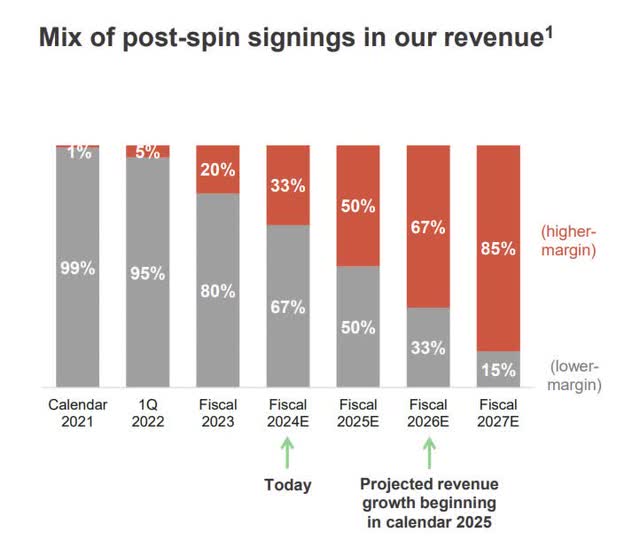

Whilst the revenue base may be slowing, what’s key is that the quality of revenue is expected to improve. Put another way, investors can be enthused about further gross margin progress, mainly driven by the quality of contracts that have been coming into the backlog in recent periods.

For context, during the pre-spin-off era, KD’s backlog largely consisted of contracts with an average gross margin profile of around mid-teens, but over the last couple of quarters, this has shifted to a threshold of 26%, and we could well expect a similar ballpark figure in Q3 as well.

What’s heartening is that a few years from now, KD will leave behind a lot of its legacy contracts with a heavier tilt towards high-margin work, so much so, that almost two-thirds of its overall mix could come from high-margin work.

Q3 presentation

One of the exciting offerings that management is doubling down on is Kyndryl Consult (basically advisory and implementation services), which only accounted for a single-digit share of the overall revenue mix a few years ago. But industry-wide skill shortages are prompting CIOs to tap Kyndryl Consult with greater fervor, so much so that this business has seen its topline grow at 17-20% YoY levels for the last couple of quarters.

Crucially, consult-related signings coming into the backlog have been growing at a pace of 32%, so one can be reasonably hopeful of this translating to sturdy double-digit growth here, yet again in Q3. Note that management’s goal is to get Kyndryl Consult to account for 20% of group sales by 2027.

Another key driver of KD’s improved sales mix could be hyperscale-related revenue, which we think could be a positive catalyst in Q3. In H1 alone, the company had generated $180m of hyperscale-related revenue, but yet management chose to be conservative and not lift the FY guidance of $300m; we think this could change in Q3.

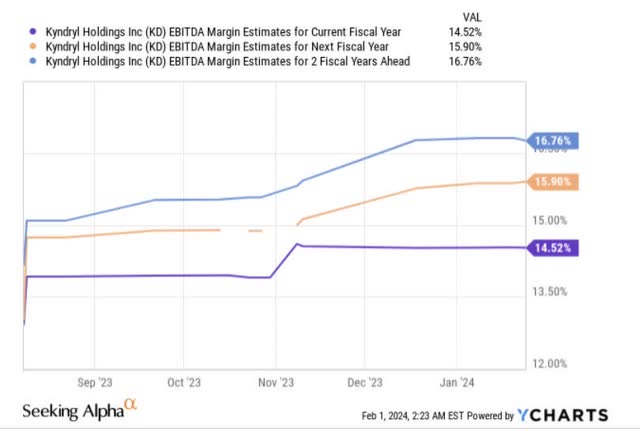

It isn’t just progress on the gross margin that’s worth anticipating, we think there could be surprises on the EBITDA front as well. Note that KD management has stepped up the pace in engendering greater automation in their service delivery, whilst also upskilling their workforce, which is likely to reflect more favorably on the OPEX base. At the end of Q1, they were only targeting $200m worth of benefits for FY24 on account of this, but this was lifted in Q2 to $250m.

The average EBITDA margin in H1 worked out to 14.35%, but management expects to hit 14.5% for the FY, so that implies incremental progress in H2. Looking ahead, note that consensus is budgeting for EBITDA margin improvements, not just for this year, but the next couple of years as well, with margins expected to improve even further by 220bps through FY26.

YCharts

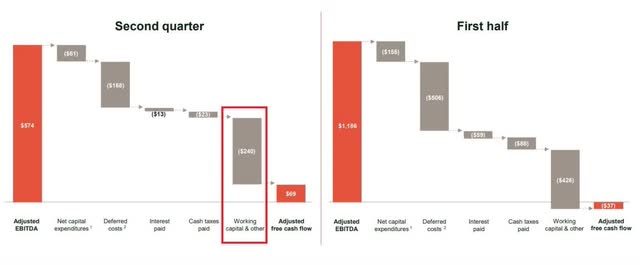

One variable that the market ostensibly hasn’t given too much of importance to is KD’s prospects of generating positive FCF for the FY, but this could well be a dark horse. They can be forgiven for not being too optimistic, as in Q1 alone, KD had witnessed a massive operating cash flow of -$173m.

Note that in Q2, the FCF got a useful leg up from an impressive EBITDA performance (EBITDA margins improved by almost 400bps YoY), but working capital spend was a massive drag, particularly on the payables front, which ate up around -$350m of cash.

Q3 presentation

In Q3 we would expect some normalization on the working capital front, and that coupled with the ongoing EBITDA progress could see a healthy uplift in the FCF. If KD can demonstrate a consistent track record of FCF generation through this year, we think conversations about a dividend or buyback could crop up by the end of this fiscal year, which would boost sentiment towards the shares.

Valuation and Technical Considerations

Even though KD’s Q3 results will likely have quite a few positives, we are hesitant to pursue a fresh long position given what the valuations and the technicals are suggesting.

The last time we covered Kyndryl, we had suggested that the stock deserved to witness some re-rating in its forward EV/EBITDA multiple, which was then priced at only 2.35x.

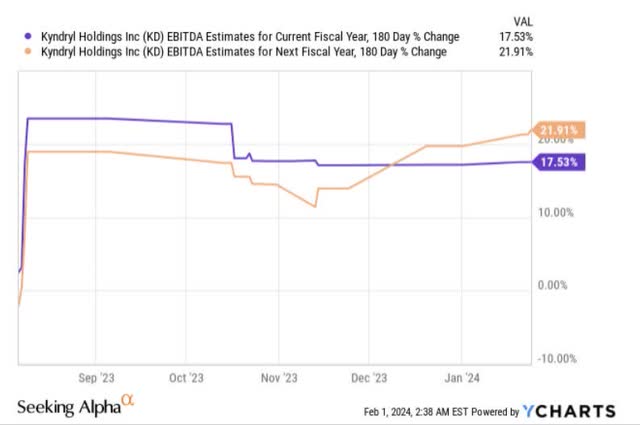

Egged on by favorable management commentary and an upgrading of EBITDA expectations for the year, we’ve also seen quite a significant upward shift in the forward EBITDA expectations, both for the current year (up by +18% over six months), and the following year (up by +22% over six months).

YCharts

Ordinarily, in light of such strong upward revisions in KD’s EBITDA profile, the stock should’ve looked even more appealing from a forward EV/EBITDA perspective. However, such has been the ferocity of the uptrend over the last six months that forward valuations no longer look attractive. KD is now priced at an EV/EBITDA of 2.91x, a +35% premium over its historical average!

YCharts

The other important point to consider is how KD’s stock is positioned relative to its peers from the broad software and services universe. This exercise can be useful in gauging a stock’s potential to garner additional rotational interest with a certain sector. As things stand, KD’s relative strength ratio versus a diversified portfolio of software and services stocks is now hardly a breath away from hitting the mid-point of its long-term range. Given this scenario, we don’t see KD benefitting from a great deal of rotational ammunition.

StockCharts

Finally, consider the recent developments on KD’s weekly chart. The price imprints of KD over the past two years or so can be captured within the two black lines. You ideally want to buy when the stock is somewhere close to the lower line, not where it is now, more so, when in recent weeks, we’ve seen quite a few candles with upper wicks near the upper boundary. This would suggest the presence of additional supply of the stock at higher levels. Note also that the relative weekly volumes appear to have tailed off (it has been at around the sub 7m levels for the last few weeks) and are a long way from the double-digit levels seen at the start of this channel.

Investing

Closing Thoughts

To conclude, KD may well deliver solid Q3 results, but given where the stock is currently perched, we wouldn’t be enthused about going long regardless. The stock is a HOLD.

Read the full article here

")

")

")