")

Introduction

I have been following DiamondRock Hospitality Company (NYSE:DRH) for quite a while now, as I like how this REIT is managed. DiamondRock owns a portfolio of 36 hotels and resorts in the US, and its assets are definitely in the premium segment.

The FFO and AFFO remain pretty strong

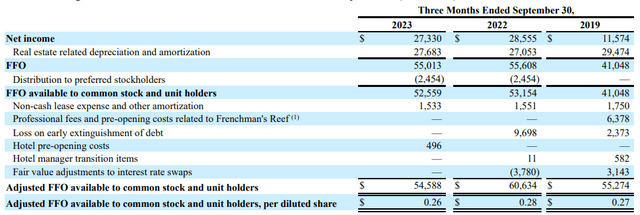

As you likely know, it’s quite useless to judge REITs by looking at its reported net earnings. Not only do the earnings include non-cash elements like the revaluation of properties (which inflates earnings as the value of the assets increases), but it also includes depreciation and amortization expenses, which definitely weigh on the result.

DRH Investor Relations

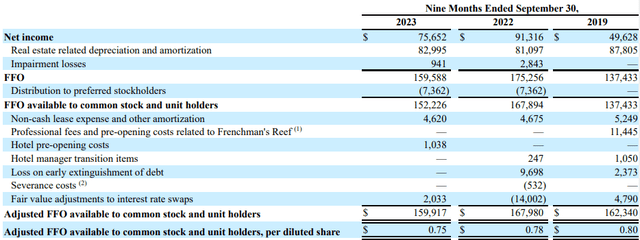

That’s why the FFO and AFFO calculations are more important to determine the underlying performance of a REIT. The image below shows the FFO calculation and as you can see, the starting point of said calculation is the $27.3M net income where after the $27.7M in depreciation and amortization gets added back to end up with $55M as the FFO result. After deducting the preferred dividends, the reported FFO available to the stock and unit holders was $52.6M.

DRH Investor Relations

In order to move from the FFO to the AFFO calculation, we have to add back a few non-recurring items, including a $0.5M non-recurring expense related to the opening costs of a new hotel. This resulted in an AFFO of $54.6M, or $0.26 per share, during the third quarter of 2023. That’s lower than the Q3 2022 result, and the entire difference could be attributed to the increased interest expenses, which almost doubled compared to the third quarter a year before. Whereas the REIT paid $9.1M in interest expenses in Q3 2022, this amount jumped to $16M in Q3 2023.

DRH Investor Relations

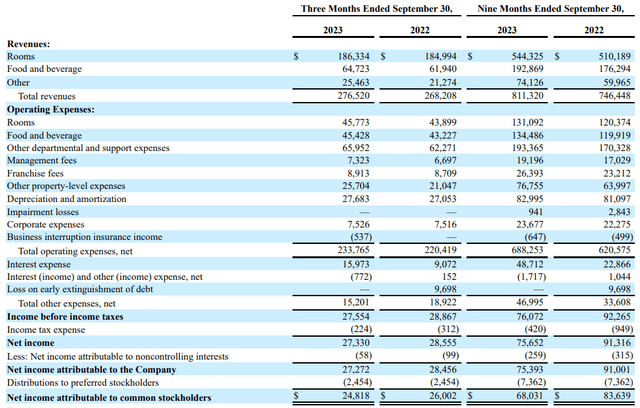

Looking at the performance in the first nine months of the year, we see the AFFO came in at $160M in the first three quarters of 2023. That’s approximately $8M lower than the 9M 2022 results, but as the income statement above shows, the total amount of interest expenses increased by in excess of $25M, which means the AFFO decrease was actually pretty manageable.

DRH Investor Relations

Keep in mind, the AFFO does not include the capital expenditures yet. During the first nine months of the year, DiamondRock spent $67M on capex and will spend a total of $100M this year. That being said, some of the hotels that were being refurbished earlier in 2023 have reopened and should start to contribute towards the FFO and AFFO results.

DRH Investor Relations

Also keep in mind, there’s no real seasonal impact on the financial results. In 2022, DiamondRock reported an AFFO of $48M in the final quarter of the year and despite higher interest expenses, this means DiamondRock’s full-year AFFO should come in around $200M. And even if you’d deduct the entire $100M in capex plans (2023 will have been a capex-heavy year compared to the normalized capex rate), the net AFFO will likely come in around $100M in 2023. And this means the preferred dividends to the tune of almost $10M per year are still very handsomely covered.

The preferred shares still offer good value for money

As mentioned in my previous article on DiamondRock’s preferred shares, the REIT has only one series of preferred shares outstanding. The series A preferred shares (NYSE:DRH.PR.A) are a cumulative issue, offering an annual preferred dividend of $2.0625 per preferred share, paid in four quarterly installments. The securities can be called from Aug. 31, 2025 on, and if the interest rates on the financial markets continue to decrease, I think this is a realistic scenario.

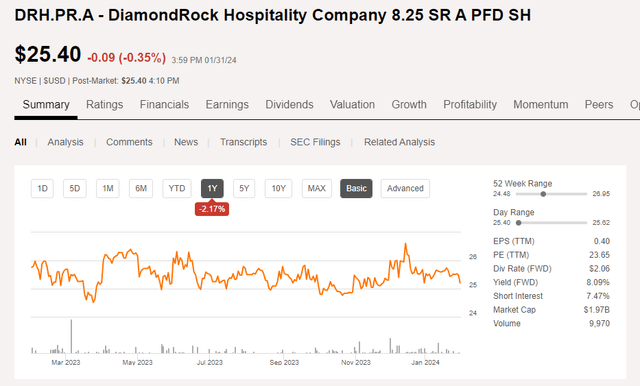

Seeking Alpha

As you can see in the image above, the preferred shares are trading at about 1.6% above their par (and call) value of $25/share, resulting in a yield to call of approximately 7.1%. While not the highest on the market, the yield to call represents an attractive way to park some cash one doesn’t need until the end of next year. And the total returns obviously increase if the preferred shares don’t get called. If the preferred shares would only be called in Q4 2026, the yield to call increases to 7.5%. And if the preferred shares wouldn’t get called at all, the yield on cost is a very respectable 8.1%.

Investment thesis

While the common shares are quite attractive as well, I’m mainly focusing on the REIT’s preferred shares as I’m looking for additional exposure to fixed-income securities. I used to own DiamondRock’s preferred shares, but I sold when the stock traded at a substantial premium above the principal value of $25/share. Now the share price has come down a bit to a level closer to the principal value of the preferred shares, I would be interested in reinitiating a long position with the mindset the preferred shares will be called next year.

Read the full article here

")

")

")