")

")

Investment Thesis

Extreme Networks (NASDAQ:EXTR) delivered a lackluster outlook for fiscal H2 2024 that left investors bewildered. Crucially, Extreme Networks’ guidance for fiscal Q3 2024 was meaningfully worse than investors were expecting to see.

That being said, it appears to be the case that once Extreme Networks gets over fiscal Q3 2024, it should be a low base from where it can once more start growing its revenues into fiscal Q4 2024 and beyond.

According to my estimates, the stock is priced at approximately 10x forward non-GAAP operating income, which is not expensive. This implies that a lot of bad news has started to be priced in. But until Extreme Networks gets more visibility into fiscal 2025, investors will remain on tenterhooks and unwilling to give this company the benefit of the doubt.

Extreme Networks’ Near-Term Prospects

Extreme Networks provides solutions and services for computer networks. They help organizations set up and manage their computer networks. Extreme Networks offers various products, including hardware like Wi-Fi access points and switches, as well as software services such as cloud management and security solutions. Their goal is to make networks more efficient and secure, helping businesses connect their devices and share information seamlessly.

As discussed on the earnings call, it’s not all bad news as Extreme Networks’ fiscal Q2 2024 results showcased positive trends, such as a 37% growth in SaaS ARR.

Moreover, Extreme Networks anticipates normalization in the third quarter as distributors and partners accelerate inventory purchases. The company’s bookings trends and funnel of new opportunities signal strong customer demand, with particular stability and growth in the EMEA and APAC regions. The addition of managed service provider partners and the launch of innovative products like Extreme Cloud Universal demonstrate a commitment to staying at the forefront of technology.

However, Extreme Networks faces challenges too. The networking industry is grappling with the aftermath of COVID-induced supply chain disruptions, impacting the company’s business and the need to address channel digestion in fiscal Q3 2024.

Larger deals are experiencing elongated sales cycles, particularly in North America, posing a challenge to revenue growth.

Also, the competitive landscape, with major competitors introducing disjointed solutions and uncertainty in their long-term product rationalization, adds market share pressure.

Given this backdrop, let’s now discuss its financials.

Guidance For H2 2024 Surprises

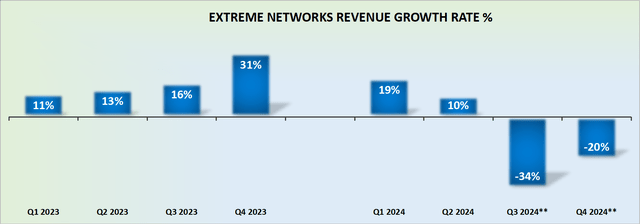

EXTR revenue growth rates

At the start of January, Extreme Networks offered a preliminary announcement that fiscal Q2 2024 results weren’t going to be overly exciting. This in and of itself put investors on alert and concerned that perhaps in the near term, the best that Extreme Networks could offer was in the rearview mirror.

But then, the company guided for fiscal Q3 2024 and fiscal Q4 2024 with an outlook of approximately negative 34% and approximately negative 20%, respectively, which took investors by surprise.

Investing is never easy at the best of times. And anyone that thinks that investing is easy is deluding themselves. This is always a game of probabilities and there are no risk-free investments.

That being said, I believe that there are certain things an investor can do to put the odds slightly more in their favor. Again, no investment strategy is perfect, and even this suggestion doesn’t always work out favorably.

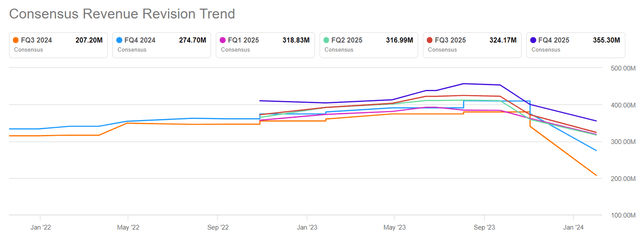

SA Premium

But when one considers the graphic above, it becomes apparent that the analyst community following this stock doesn’t hold the company’s near-term prospects in high esteem.

I reiterate my view to my followers. Don’t position yourself in a stock where it’s your ego on the line against the market. As you can see above, the analysts following the company are clearly disenchanted with the company’s prospects and they are out there reducing the company’s sales estimates. As an investor, it’s much easier to invest in companies where The Street is out there pumping your stock than it is when they are reducing the revenue estimates on your company.

It’s not that the analyst community is always right. Absolutely not. But battleground stocks make for tough investments that wear down the investors’ psyche.

EXTR Stock Valuation — 10x Forward Non-GAAP Operating Income

If we presume that fiscal Q3 2024 is the near-term low part of the cycle for Extreme Networks and that starting fiscal Q4 2024 its prospects stabilize, it’s possible that as a forward run-rate, Extreme Networks could be on a path towards $160 million of non-GAAP operating income.

There can be little doubt that this looks like a cheap stock. But the only problem with it is that Extreme Networks is now in the penalty box as a “show-me” story.

Until investors become very comfortable that there are no more negative surprises to emerge, the stock will remain priced at a low multiple. Even though, there’s clearly a lot to like about the company.

Indeed, Extreme Networks is a solid free cash flow producing company that has dramatically improved its balance sheet from a net debt position of approximately $60 million to a net cash position of approximately $25 million in twelve short months.

The Bottom Line

In conclusion, Extreme Networks faces a challenging near-term outlook following a disappointing fiscal H2 2024 guidance, causing investor concern.

The company’s fiscal Q3 2024 projections were worse than expected, contributing to a cautious sentiment. However, there is optimism that once Extreme Networks surpasses fiscal Q3 2024, it can rebuild from a low base, potentially fostering revenue growth into fiscal Q4 2024.

Despite the current uncertainties, the stock is relatively inexpensive at around 10x forward non-GAAP operating income, meaning that much of the bad news may already be priced in.

Still, investor confidence remains contingent on Extreme Networks gaining more visibility into fiscal 2025.

While there are positive aspects, such as a 37% growth in SaaS ARR and strategic initiatives to address issues, Extreme Networks remains in a “show-me” story, and until concerns diminish, hence the stock may continue to be undervalued despite its strong financial fundamentals and meaningfully improved balance sheet.

Read the full article here

")

")