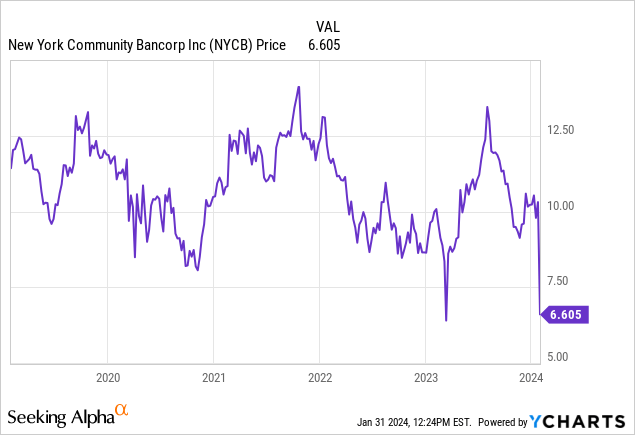

There is a great amount of commentary on today’s surprise Q4 earnings miss from New York Community Bancorp, Inc. (NYSE:NYCB) and the massive dividend cut down to $0.05 quarterly. Ouch. Shares tanked 40% premarket. We were asked about it in our investing group premarket, and we discussed with members that we felt while this was certainly a surprise, shares were a buy at $6.00. We reopened a trade there looking for an exit at $8.

All kinds of rumors are circulating now. Is this the collapse in commercial real estate so many have warned? Are more bank failures ahead? Does this dividend cut mean that NYCB is on the list of possible failures? The latter is rich, given they bought up many of Signature Bank’s old assets. When we last covered the stock we told you that we were closing out a trade but did recommend keeping a small allotment for a long-term investment with house money. Obviously, that position has dipped, almost by 50%. It would not have been so painful had the dividend not been cut. But we think this sets up new money for entry for a trade, in spite of the surprise miss and cut. Let us discuss.

New York Community Bancorp headline numbers strong in Q4

Shares have now retraced to levels we saw in the mini crash in 2023, where we last bought the stock for a rapid-return trade. We do see less upside now, but upside nonetheless. NYCB reported a weak Q4, whiffing on expectations. We cover a lot of banks and know the industry well. We do not believe this is the start of a collapse in regional banking. The losses were driven by a spike in provision for credit losses, which yes, raises some concern, but not enough to think the bank is going under. The company saw revenues of $886 million and a loss of $0.27 per share.

What were the weak points? Margins were poor, provisions were up, and significant actions to boost liquidity including the dividend cut, something management did not take lightly. For the year, overall, the bank is transforming:

We reported an increase in net income available to common stockholders, diversified our balance sheet with commercial loans now representing almost 50% of our total loans, and increased the percentage of non-interest-bearing deposits. In addition, we have made terrific progress integrating Flagstar Bank, meeting every milestone along the way and unveiled a fresh, new re-branding campaign, which will launch shortly after the planned systems conversion is completed in mid-February…we took decisive actions to build capital, reinforce our balance sheet, strengthen our risk management processes, and better align ourselves with the relevant bank peers. We significantly built our reserve levels by recording a $552 million provision for loan losses, bringing our ACL coverage more in line with these peer banks…we are also building capital by reducing our quarterly common dividend to $0.05 per common share. We recognize the importance and impact of the dividend reduction on all of our stockholders and it was not made lightly. We believe this is the prudent decision as it will allow us to accelerate the building of capital to support our balance sheet as a Category IV bank.

Because this is a bank preparing to be over $100 billion in assets, requirements for operations are different. This is part of the story. Commercial loans are an issue, as is exposure to commercial real estate. There is a lot of anxiety about this space. We think it may be overdone, but this is where the Street is. And NYCB has significant commercial exposure. Total commercial loans represent 46% of total loans held for investment, and multi-family loans represent 44% of total loans held for investment at December 31, 2023, which reflects significant diversification compared to a year ago. That is a major improvement. Commercial real estate loans were flat at $13.4 billion at December 31, 2023, unchanged compared to the start of the quarter.

Versus the past, in short, there was more risk exposure concentration a year ago. Residential loans and other loans represented 7% and 3%, respectively, of total loans held for investment.

Loans and deposits

We always look for loan and deposit growth in regional banks. Essentially, more deposits means more capital available to lend, and more loans tends to mean more fee income as well as interest income. That said, deposits fell but loans grew. But there is a big asterisk here. Overall deposits totaled $81.4 billion, or $1.3 billion lower compared to $82.7 billion at the start of the quarter. The decrease was primarily driven by a $1.8 billion decrease in custodial deposits related to the Signature transaction, but if you back these out, total deposits increased $457 million.

There was also growth in loans. Total loans and leases held for investment were $84.6 billion, compared to $84.0 billion at the start of the quarter. The linked-quarter increase was driven by growth in C&I loans and residential mortgages. One of the weak points was net interest margin which fell jumped 45 basis points to 2.82% compared to the prior quarter. This was due to liquidity building actions.

New York Community Bancorp asset quality actually improved, but allowance for credit losses surge

Loans were up but with provision expense surging we had concerns over asset quality. We were surprised to see relative improvement in asset quality. Non-performing assets are another critical indicator to watch. In 2023, non-performing assets as a percentage of total assets have been relatively stable. In Q4, total non-performing loans actually decreased $7 million or 2% to $428 million compared to the start of the quarter. Although, repossessed assets of $14 million were slightly higher compared to the prior quarter. Overall non-performing assets also decreased 1% to $442 million from the sequential quarter.

This is positive, folks.

Now, the allowance for losses increased to be in line with other Category IV banks. At the end of Q4, allowance for credit losses was $992 million compared to $619 million to start the quarter, up $373 million “reflecting actions to build reserves during the quarter to address weakness in the office sector, potential repricing risk in the multi-family portfolio and an increase in classified asset.” So, there are some clues that not all is well in the office real estate space, but it is not portending collapse, folks. The allowance for credit losses to total loans held for investment increased to 1.17% compared to 0.74% in the sequential quarter on the back of more allowances.

The bank is also historically highly efficient. But Q4 was an anomaly, with efficiency worsening to 67.86% from 56.15% in Q3, and up markedly from 40.72% a year ago. This reflects moves to acquire more assets, and increased provisions for losses.

Still very attractive relative to book value

Despite the carnage, NYCB stock trades at a massive discount-to-book value. It is on sale here. If you believe the collapse is coming, avoid the stock. But we do not subscribe to that notion. We see shares as a buy at $6.

Look, the dividend cut hurts, but most of the decline is stemming from that cut. Interpretations vary, but we are taking management at face value that this was done for liquidity purposes, but not because the bank is in trouble. The Fed is very closely watching, and you can rest assured the Fed is in contact with NYCB regarding this report and cut, to ensure there is not contagion on the books that could be spreading.

The valuation overall here is attractive. We really like to compare the share price to that of book value. The bank is still trading way below book value. Book value was $14.28, so at $6.30 for the current share price, that’s a huge discount. The discount to tangible book value of 35% here! Hold your nose and buy. We love to buy bank stocks close to or below tangible book, so the value proposition is very strong here. More color came on the conference call:

NYCB remains well capitalized under all applicable regulatory requirements, resetting our capital allocation priorities was a necessary step to accelerate the building of our capital. We are confident that these actions we took in the fourth quarter and the continued execution of our strategy will position the company to deliver enhanced value over the long-term.

More on office exposure

We dug into the call further, and in the Q+A more came out on the office exposure. We are confident in the responses. When asked about future losses:

we look at the office perspective and the general office weaknesses throughout the country. And we really did a deep dive in the office portfolio as well as thinking through payment shock and interest rate shock given the rise of interest rates that we’ve experienced over the past few quarters, in particular, the impact to our customers in respect to repricing…we’re focusing on payment shock, interest rate shock and the developments in the commercial space…[also] we have not seen significant losses in multi-family.

We would encourage readers of this column to go through the Q+A. They were asked about the stock being at these lows. Management focused on the strategies being put into place. It was a tough Q+A. But nowhere were analysts concerned about collapses, or failures. It was more about expectations for future margins, rate cuts, and the health of assets of the newly $100 billion asset Category IV bank.

Final thoughts on NYCB stock

This was a shock to the market and New York Community Bancorp, Inc. shareholders. But we think you take advantage of the drop. Sure, the new yield reset is painful, $0.20 is now a 3% yield, cutting income from income investors. It is tough to swallow. But for traders, and long-term investors, the bank is growing and making strategic moves to secure its future. We think shares rebound in the coming weeks and months from the $6 level.

Read the full article here

FDA Approval")