")

")

")

")

")

")

Last year, I covered The GEO Group (NYSE:GEO) on three different occasions.

In January, I wrote that while management seemed to be taking the company in the right direction, it might be wise for investors to lock in some profits, as shares had rallied notably at the time. Following that article, shares lost nearly 40% of their value.

Then, in June, I turned bullish on the stock and made the case that GEO might have hit bottom. As shares started their upward trajectory, I provided an update in October, suggesting that the rally was potentially just getting started.

Reflecting on my analyses, I am pleased to note that GEO has experienced significant gains, rising by approximately 60% and 39% since the publication of each respective article. Interestingly enough, I accurately pinpointed the bottom for GEO Group, though I must admit that a certain element of luck has most certainly played a role, as shares could have easily treaded lower for any reason.

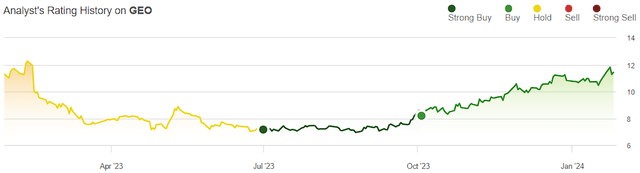

Past Analyst’s Ratings (Seeking Alpha)

In this article, I am revisiting the stock to reassess its investment case and evaluate whether GEO could potentially be resuming its dividend sooner than most investors may expect.

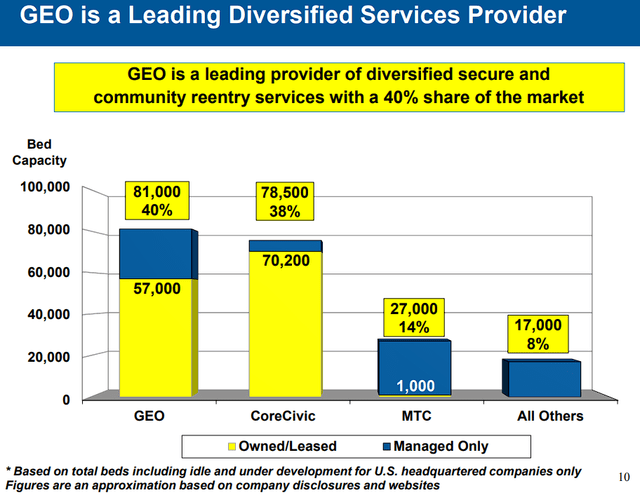

For those unfamiliar with GEO, the company is one of two prominent providers of secure facilities, immigration processing centers, and community reentry centers. It has a 40% market share in the secure and community reentry services “industry”, with over 80,000 beds. CoreCivic (CXW) trails closely behind, with a 38% market share of the space.

GEO Market Share Overview (Q3 Investor Presentation)

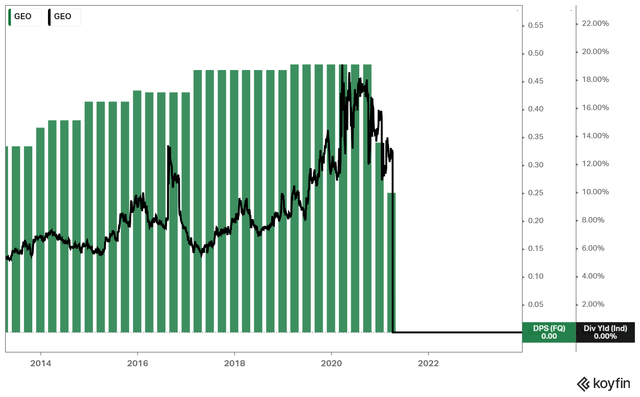

For context, the company’s investment case took a turning point in 2019. At the time, GEO stock had garnered considerable interest from income-focused investors pursuing above-average dividend yields. As displayed in the graph below, GEO used to pay out a growing dividend throughout the preceding decade, while after 2019, its yield hovered in the high-single to low-double digits.

The GEO Group’s Dividend History & Yield (Koyfin)

When you revisit the articles published on Seeking Alpha in that timeframe, a mere glance at the comments will reveal that GEO had a hardcore fan base. Many analysts praised the company for its massive yield and recession-proof qualities, making GEO an increasingly popular stock.

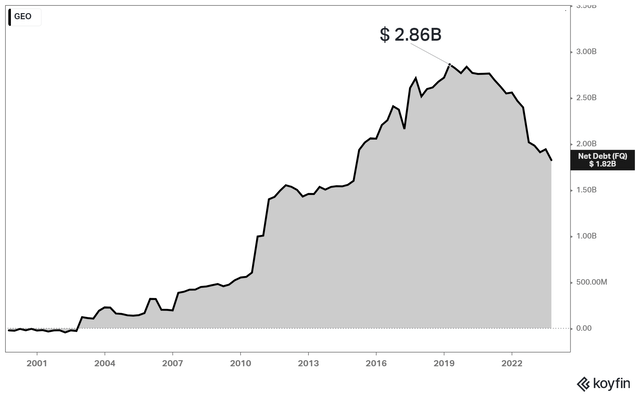

While investors relished the hefty dividends, it became evident that most overlooked the company’s substantial debt burden. On the surface, the dividend seemed well-supported, but beneath the surface, the balance sheet continued to deteriorate annually. Illustrated in the graph below, GEO’s net debt exhibited a consistent upward trajectory, reaching $2.86 billion in Q1-2019.

GEO’s Net Debt Development (Koyfin)

One could argue that growing debt levels would not necessarily present an issue, given that similar to all REITs (GEO was a REIT at the time), GEO could take on debt to fund its expansion. However, the issue here is that GEO’s debt was increasing much faster than its assets were growing.

Simultaneously, both GEO and CXW faced heightened scrutiny at that time as state governments and banks distanced themselves from private detention facilities. This shift raised significant questions about the future of the industry.

All major banks, previously providing credit and term loans to GEO, were now committed to severing ties with private prisons once existing obligations were fulfilled.

Given this decision came after GEO’s debt levels had already soared, investors suddenly woke up to the realization that the safety of GEO’s dividend might not align with their earlier perceptions.

Confronted with this formidable challenge, GEO’s management had no choice but to embrace a deleveraging strategy. The company strategically shifted its focus towards leveraging internal operational cash flows to fund future capital expenditures.

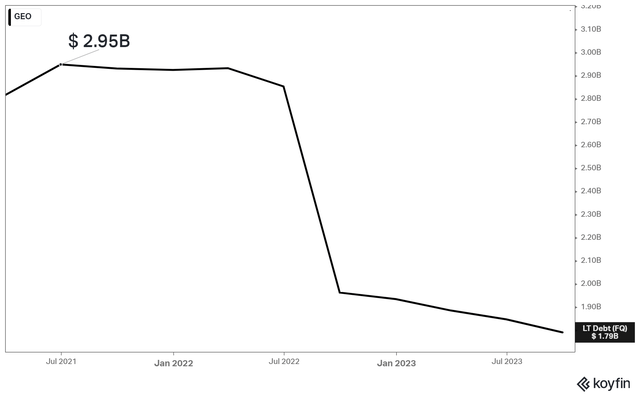

In order to achieve self-sufficiency, GEO slashed the dividend in 2021 and started using these funds to pay down its debt. As you can see, from Q2-2021 to Q3-2023, GEO’s long-term debt fell from $2.92 billion to $1.79 billion.

GEO’s Total Debt (Koyfin)

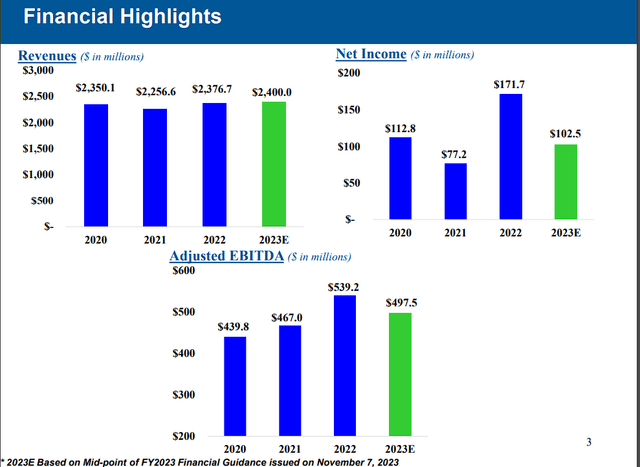

Note that the company’s underlying cash flows have remained robust in the post-dividend cur era. After all, this is a recession-proof business that is essential to its State and Federal clients.

Revenue generation has remained stable, while adjusted EBITDA has grown in recent years.

GEO’s Financials (Q3 Investor Presentation)

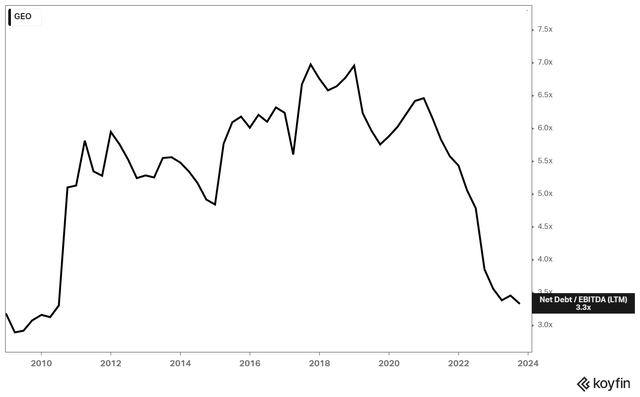

With debt levels declining and cash flows remaining stable, GEO’s net debt/EBITDA has now reached rather healthy levels, in my view. At a ratio of just about 3.3X, GEO appears to be the least leveraged it has been in about 14 years.

GEO’s net debt/EBITDA (Koyfin)

In my view, this development should allow the company to reassess its capital return policy and resume paying dividends sooner than most investors would expect.

While you don’t see analysts talk about a potential dividend resumption, GEO should gradually be able to support a healthy mix between deleveraging and rewarding shareholders.

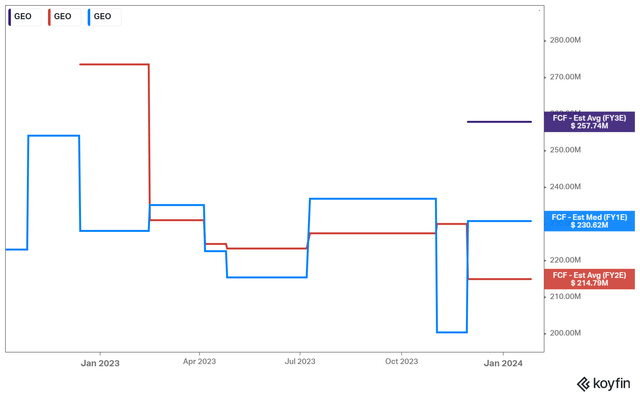

As you can see, consensus estimates point toward GEO generating a free cash flow of about $230 million this year. By 2025, free cash flow is expected to be closer to $258 million.

GEO Group Free Cash Flow Expectations (Koyfin)

If and when GEO decides to reinstate its dividend, the yield is likely to be quite attractive at the stock’s current levels. Even if we assume a conservative policy, such as allocating about half of its free cash flow, let’s say, $100 million annually, GEO would yield about 7% at the stock’s current price.

It’s important to emphasize that this $100 million (arbitrary estimate) remains well below the substantial $230 million+ that GEO paid out in dividends per annum before the dividend was suspended.

Hence, GEO is poised not only to rekindle the attention of income-focused investors but this time around, its dividend is anticipated to be even more appealing, thanks to a significantly strengthened balance sheet and expanded dividend coverage.

While it’s impossible to predict if and when GEO will reinstate its dividend in the coming years, insights from management during earnings calls hint that such an event may not be too far away.

Let’s look back at GEO’s Q4-2022 earnings call when management stated:

…doing this [referring to reducing debt] still would allow us to achieve net leverage below 3.5 times adjusted EBITDA by the end of 2023, …achieving that we hope to reduce debt by another $175 million to $200 million and reach net leverage below 3.0 times adjusted EBITDA by the end of 2024

…By 2024, we are also hopeful that interest rates will have declined to an environment that will allow for the refinancing of portions of our debt, further reducing our net interest expense. Once we achieve our stated debt and leverage reduction goals, we expect to explore options to return capital to our shareholders.

Almost a year later, the company appears to be positioned where management predicted last February. As shown in Q3’s investor presentation, management expects that GEO will end the year with a net leverage of 3.66X-3.58X.

GEO’s Guidance for 2023 (Q3 Investor Presentation)

At the same time, management kind of foresaw a potential decline in interest rates by the end of 2024, aligning with widespread predictions of multiple rate cuts by major banks.

Since management has stuck to its net leverage target of 3.0X in recent quarters, which I believe is achievable by the end of 2024, a dividend resumption in early 2025 doesn’t sound far-fetched.

Combined that such a resumption would lead to a notable dividend yield even with a prudent free cash flow payout ratio estimate, I remain bullish on the stock.

Read the full article here

")

")

")

")

")

")