")

")

")

")

")

")

Investment thesis

Skyworks Solutions (NASDAQ:SWKS) is going to report its Q1 ´24 results on January 30th after the market closes. I wanted to revisit the company to see how it has progressed since then and give some info on earnings expectations and some comments on the outlook. The company has navigated the downturn very well, and once market conditions improve, so will the company’s top-line growth efficiency and profitability. I reiterate my buy recommendation as the company has a very strong balance sheet that will help it navigate any further downturns in the economy.

Skyworks Solutions financials

As of FY23, the company had around $730m in cash and marketable securities against around $1B in long-term debt. That is a very strong position to be in, as many investors tend to avoid companies with excessive leverage on their books. To prove that the debt on the books is not an issue, I look for an interest coverage ratio of at least 5, which tells me that the company’s EBIT covers annual interest expenses at least 5 times over. SWKS’s coverage ratio is over 17x, which means it has no problem covering interest expenses and is at no risk of insolvency.

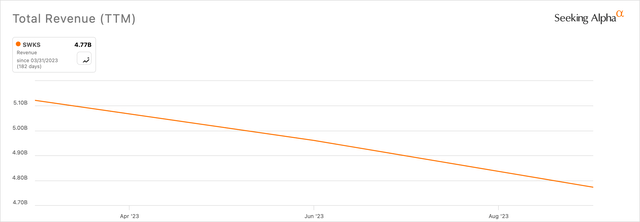

In terms of revenues, over the whole of FY23, the company has been struggling, as every quarter has seen low-double-digit y/y declines. The company has been underutilizing its factories and is trying to get rid of the excess inventory, which caused such a glut in revenues. Furthermore, the weakness in the Android market is lasting for much longer than anyone had anticipated just a couple of quarters ago.

Revenue over the year (SA)

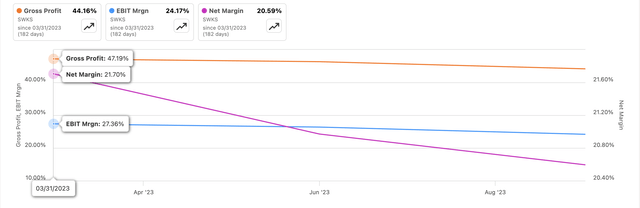

In terms of margins, we can see declines across the board in the last year, which was caused primarily by the underutilization of factories due to the slump in Android demand. In my first article on the company, I mentioned that the bottom is set or close to being set and in 2024 we should start hearing a turnaround in demand for mobile phones, but so far, the management has said that they “continue to under-ship to natural demand as the industry rebalances.”

Margins over the year (SA)

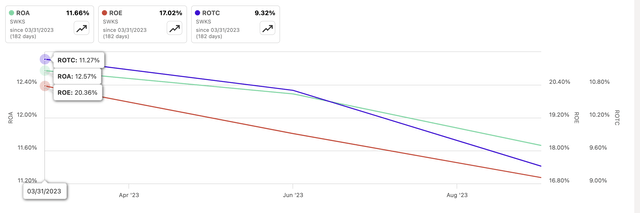

Naturally, with the decrease in margins, comes a decrease in efficiency and profitability. The company’s ROA and ROE have been on a downtrend all of 2023, and it is understandable given the fact that their biggest revenue segment has seen a slump. Furthermore, the company’s ROTC, which measures how efficiently the management is allocating capital to profitable projects, has been coming down quite a bit too. Seems like the company has lost some of its edge during 2023.

Efficiency and Profitability (SA)

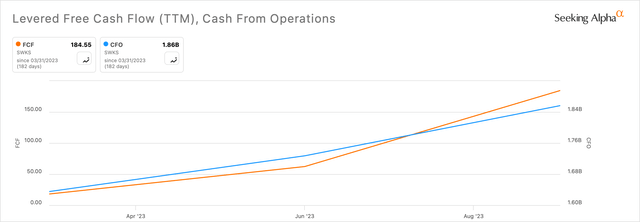

One positive I can see in the financials is the company’s ability to generate higher free cash flow over the last year, which is commendable. The management mentioned that the company can consistently sustain 30%-35% free cash flow, and once the market conditions improve, I could see this number to be even higher than what the company is achieving right now.

CFO and FCF (SA)

Overall, it does look like the company may be struggling on paper due to these macro conditions, however, with a strong balance sheet and growing free cash flow even during these times, in my opinion, the downside risks are very low going forward. Even with more downturns ahead, the company should weather the storm and come out on top.

What to expect from Skyworks’ upcoming earnings

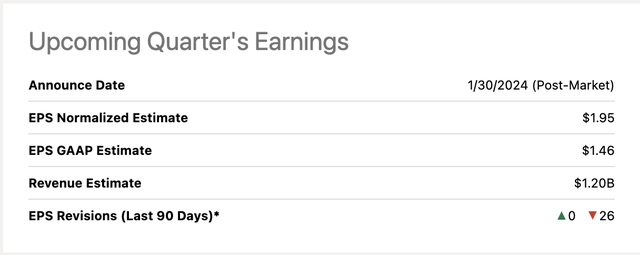

The management expects to book $1.17B to $1.225B in revenues, while expecting the mobile business to show a little momentum. In the broad markets, the company expects the inventory unwinding to continue to weigh on the company’s revenues slightly. Analysts are expecting non-GAAP EPS of $1.95 and GAAP EPS of $1.46 on $1.2B revenues. So, it looks like we are still going to see quite a big y/y decline in revenues of around 10% or so. Furthermore, over the last 90 days, there have been 26 down revisions, which is not a good sign. On the flip side, with such down revisions, the company may be able to beat the estimates.

Earnings estimates (SA)

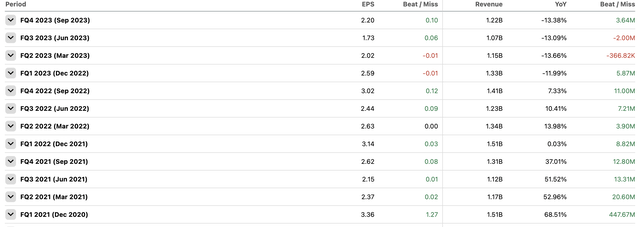

Speaking of beats, the company over the last 12 quarters missed EPS estimates twice by a penny and twice on revenues by also a very small amount. There’s a high chance that the company will beat in the upcoming report.

Earnings Beats and Misses (SA)

SWKS stock outlook

What I would like to see from the company in the upcoming report is what kind of guidance the management is going to provide. Everyone already knows the glut in the mobile sector has been rough for SWKS and many other companies, so a positive outlook may bring a lot of volatility to the company’s share price, and so would a negative guide.

I would like to see more improvements in the company’s overall margins. The management is guiding around 47% to 48% for the quarter, which as you saw in the image above is much better than what the company managed to achieve during the whole of ´23. This is still much lower than what the company would like to achieve in the long run, which is around 53%, and that will take some time, but I believe once the market conditions across the board start to improve, the company will easily achieve it.

In terms of its biggest customer, and the biggest risk for many investors who are looking to start a position in the company, we may hear something regarding Apple (AAPL) and the performance of its new headset that was released in September. I was a little disappointed that the dependency on Apple has increased to around 66% of net revenues for ’23. In my previous article, since we didn’t have all the info yet, it looked like the company was diversifying away from Apple. Still, since the slump in other business segments happened, the revenue from Apple seems to be larger in terms of percentages, however, once again, when market conditions improve, the revenue from Apple in % terms will come down. Apple is going to report its earnings a couple of days after SWKS, which is good because if Apple has bad earnings, SWKS should be relatively fine as the management may announce similar bad news on the 30th of January. From preliminary reports made by KeyBanc, the sales of the new headsets were strong in December, however, inventories were still above the level from a year ago.

In terms of the global smartphone market, researchers are already seeing a rebound in 2024 after seeing two consecutive years of declines previously. People upgraded all of their devices during the pandemic, so naturally, there was going to be very little demand to do it again, however, it is getting to that time when people need to start upgrading once again, as the devices’ batteries start to drain much quicker now and overall performance starts to wane. I haven’t upgraded my phone in a good few years now and I am in dire need of a new one, as this one barely charges anymore. I’m sure I’m not the only one in this boat. I would like to hear what the management thinks about the next couple of quarters in terms of the Android market and its subsequent recovery.

Speaking of the smartphone market, I believe there may be a lot of demand coming in over the next couple of years due to the buzz of AI. Qualcomm’s (QCOM) newest chip the Snapdragon 8 Gen 3 comes with AI capabilities, which could fuel demand for these sorts of devices because of the buzz of AI. Many people look for the best tech out there and will be willing to upgrade their devices just to have the latest tech. The management seems to agree with this sentiment, saying “Over time, we expect high-performance smartphones will be a critical platform for advanced AI capabilities, and in turn could spark a major upgrade cycle”, during the Q4 earnings call.

Closing comments

I believe that the company is still a buy at these levels. The company’s balance sheet is very strong, which played a huge role in weathering the downturn successfully so far.

Once we start to see proper rebounds in the key market segments, the company’s top-line growth will follow suit.

The dependency on Apple is a real risk still, and if it can start making its own chips in-house, that will be devastating to SWKS, however, just because it has the money to make something, it doesn’t mean it will be good at it, so I am not worried about the concentration of revenues right now. I think the worst is over and we should see efficiency and profitability improve over the next couple of quarters, with time, the company will achieve its long-term margin goals if everything goes well, and the management is competent at looking for inefficiencies and cutting them out swiftly.

Read the full article here

")

")

")

")

")

")